March 26, 2024

- Markets enjoying calm before the data storm.

- US Durable Goods rebound-rise 1.4%.

- US dollar opens with losses on improved risk sentiment.

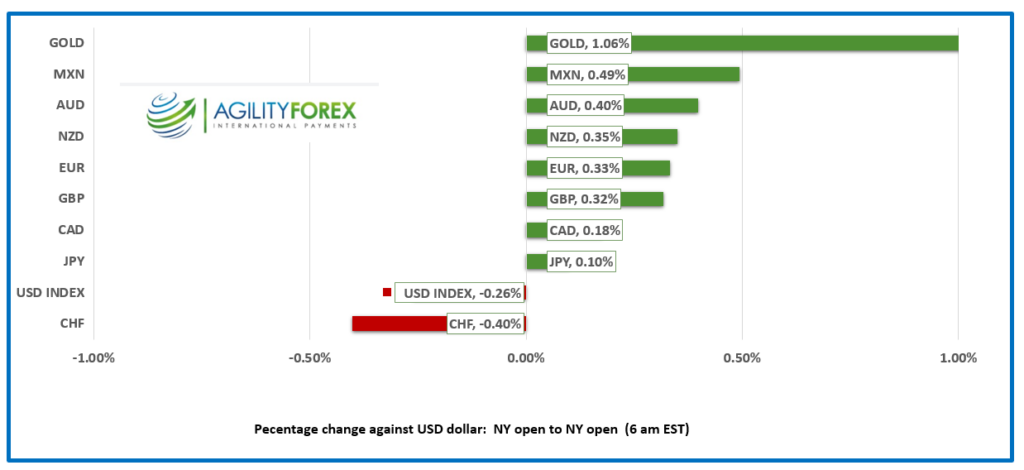

FX at a Glance

Source: IFXA/RP

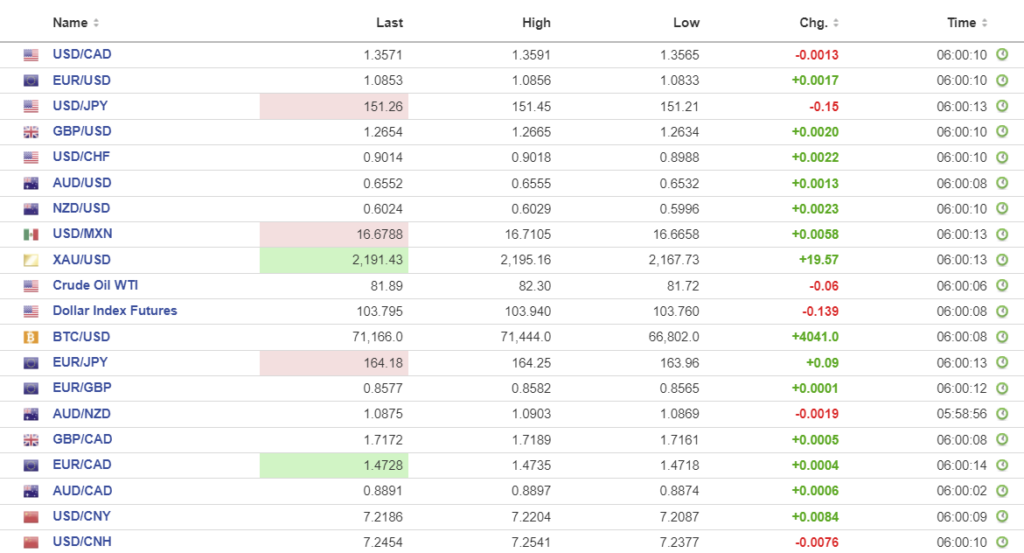

USDCAD Snapshot: open 1.3569-73, overnight range 1.3555-1.3591, close 1.3586

USDCAD trickled lower overnight on the back of a generally soft US dollar with firmer oil prices giving it a bit of a lift but is otherwise rangebound. Prices have been contained within a 1.3360-1.3815 range since the middle of January and that range is pretty safe, at least until the May 1 FOMC meeting.

Bank of Canada Deputy Governor Carolyn Rogers spoke about Canadian productivity, yesterday. She pointed out that domestic productivity has not significantly improve over the years compared to the US and other G-7 countries. She suggested that low productivity adds to the difficulty in managing inflation risks.

Oil prices inched higher due to supply concerns on rising geopolitical tensions and attacks on Russian crude infrastructure. Russia launched 57 missiles at civilians in Kyiv yesterday, but Putin is outraged because ISIS attacked Russians.

Canada January GDP is due Thursday and expected to show that the economy grew at 0.4%.

USDCAD Technicals

The intraday USDCAD technicals are bearish in a downtrend channel with resistance at 1.3590 and support at 1.3540. Even so, the price action is merely noise in the context of the dominant 1.3360-1.3820 range since mid-January.

The 2024 uptrend line is intact above 1.3460. A break above the 1.3630-1.3660 zone would shift the focus to 1.3900.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3590 and 1.3620. Today’s range is 1.3540-1.3610.

Chart: USDCAD 4 hour

Source: DailyFX

The thrill is gone.

B.B King lost his thrill in 1970, while for FX traders are finding that the spark has faded. FX markets are posting small gains against the US dollar, but all the major G-10 currencies are within recent ranges. That’s because of the Fed refuses to commit to any interest rate action while policymakers flash conflicting signals. Atlanta Fed President Raphael Bostic is a champion flip-flopper. He has gone from predicting three rate cuts with the first as soon as the summer on February 29, to saying only two cuts were likely a week later. Now he is calling for just one cut. Spot traders hold positions longer than Bostic holds a rate view.

US Durable Goods Orders rose 1.4% in February )previous -6.9). It is good news as it suggests that the economy is slowly improving. Markets barely budged on the results.

Case-Shiller Home Price index is expected to rise 6.7% (6.1% in December). Consumer Confidence is expected to show a small improvement.

Asian equity indexes followed Wall Street’s lead and closed with small losses. European traders are more optimistic, and the German Dax is leading the other major bourses higher, rising 0.40%. S&P 500 futures have gained 0.42% and gold (XAUUSD) has jumped $26.00.

EURUSD

EURUSD has a bit of a bid and is at the top of its 1.0835-1.0865 range in NY despite recent comments by ECB officials suggesting that the time is right to cut interest rates. Bank of Italy Governor Fabio Panetta said that “The consensus emerging – especially in recent weeks – within the ECB governing council points in this direction.” Monday, ECB Chief Economist Philip Lane spoke optimistically about declining inflation heading down to its 2.0% target.

GBPUSD

GBPUSD rallied “right smartly” rising from 1.2634 to 1.2668 overnight. Traders raised the odds for a June rate cut to 80% after last week’ s unanimous BoE monetary policy decision. Policymaker Catherine Mann pushed back against that notion, saying, “I think they’re pricing in too many cuts which is giving GBPUSD a bit of support.

USDJPY

USDJPY is steady in a 151.21-151.45 range. Prices are supported by wide US/Japan interest rate differentials (in favour of the US), but gains are capped following official warnings that suggest FX intervention is likely. Many traders are looking forward to intervention to buy USDJPY at the proverbial “better level.”

AUDUSD and NZDUSD

AUDUSD is slightly higher, rising in a 0.6532-0.6555 range due to improved risk sentiment weighing on the US dollar against the major G-10 currencies. AUDUSD is underpinned by the PBoC actions to support CNY. Traders ignored the Westpac Consumer Sentiment Index data which dropped to 1.8% compared to last months 6.2% increase. Consumers are cautious and inflation and interest rate sentiment fears are only easing gradually.

NZDUSD rose from 0.5996 to 0.6029 in NY on the back of improved risk sentiment.

USDMXN

USDMXN retreated in a 16.6658-16.7105 range supported by the move below key support at 16.7000. The move was due to renewed US dollar selling pressure vs the majors and the lingering benefit of the slightly higher than expected inflation data for the first half of March (actual 4.48%, forecast 4.45%, previous 4.35%)

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

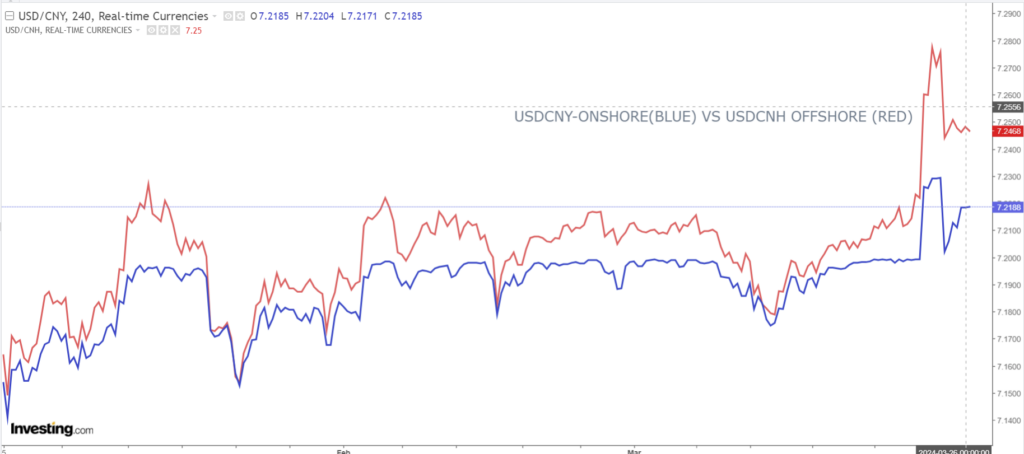

China Snapshot

PBoC fix: 7.0943 vs exp. 7.2037 (prev. 7.0996.

Shanghai Shenzhen CSI 300 rose 0.51% to 3543.75.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com