January 17, 2024

- US Retail Sales-Ex autos rise 0.4% m/m (November 0.2%)

- Traders are re-thinking early rate cuts in Europe and US.

- US dollar surges again; Trump factor perhaps?

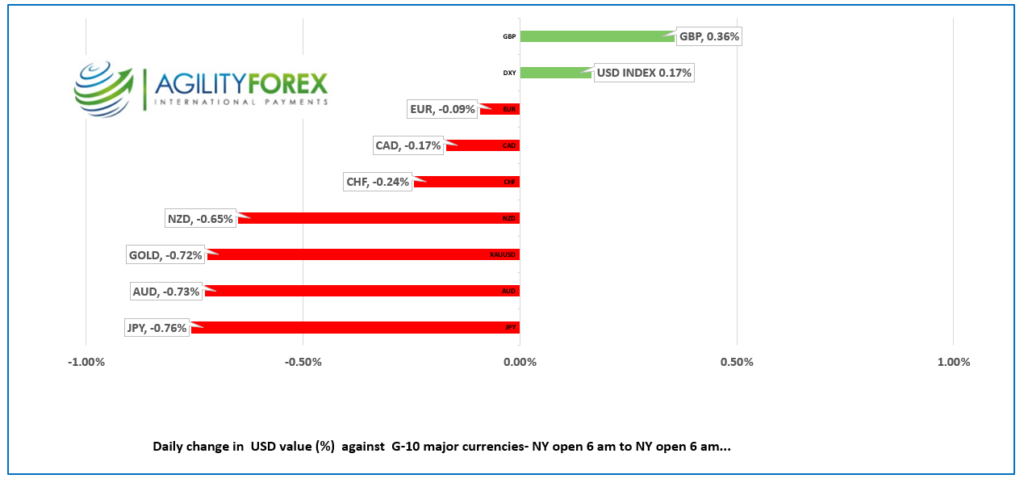

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3516-19, overnight range 1.3480-1.3531, close 1.3490.

Yesterday, USDCAD dropped to 1.3448 from 1.3481 on the heels of the Canadian inflation report for December (actual Canada CPI r3.4% y/y, November 3.1%). The move didn’t last and USDCAD rebounded to 1.3504. That’s because of comments from Fed Governor Christopher Waller who suggested there was no need for the FOMC to cut interest rates as soon or as sharply as markets were pricing.

The Bank of Canada has a similar dilemma. They want to lower rates, but inflation is proving to be somewhat reluctant to cooperate so rate cuts may be delayed.

USDCAD got an extra lift after WTI oil prices dropped from yesterday’s peak of $73.09/b to $70.75/b overnight. Weaker than expected Chinese economic growth fueled the losses.

Canada Industrial Product Price index fell 1.5% m/m (forecast -0.7% m/m) while the Raw Material Price index dropped 4.9% m/m (forecast -1.6%). Both results suggest inflation will continue to ease.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3480, looking for a break above 1.3550 to extend gains to 1.3620. However momentum studies suggest the rally is running out of steam and that prices may need to move lower, before the uptrend resumes.

The USDCAD uptrend channel band that began at the beginning of the year is 1.3400-1.3550 and a break below 1.3480 suggests the bottom of the channel will be revisited.

For today, USDCAD support is at 1.3480 and 1.3450. Resistance is at 1.3550 and 1.3590. Todays range 1.3450-1.3540.

Chart: USDCAD 4 hour

Source: DailyFX

G-10 FX recap

“On second thought…” Traders are rethinking their outlooks for aggressive ECB and Fed rate cuts and concluding that perhaps thinking the Fed would lower rates by 150 bps in 2024, was a tad aggressive. Fed Chair Jerome Powell previously warned that policymakers would take a data-dependent approach to monetary policy, but his words of caution were ignored. Other policymakers followed suit, but it wasn’t until Fed Governor Christopher Waller spoke yesterday, that traders took notice.

Mr. Waller sent a message that said, “When the time comes to begin lowering rates, I believe it can and should be lowered methodically and carefully.” He pointed out that because economic activity and the labor market were in good shape, he didn’t see a need to move quickly or cut as rapidly as in the past.

His comments weighed on equity markets and Wall Street closed in negative territory. Things deteriorated further in Asia following weaker than expected Chinese Q4 GDP growth and December Retail Sales.

Asian equity markets closed with losses, but the Chinese indices were hammered. Hong Kong’s Hang Seng fell 3.71%, its biggest loss since October 2022, and the Shanghai Shenzhen CSI 300 index fell 2.17%. ECB pushback against early rate cuts fueled a sell-off in European equity indexes. The UK FTSE 100 index is down 1.64%, while the French CAC 40 index is down 1.24%. S&P 500 futures have lost 0.50%.

The US dollar rallied at the same time Trump decisively won the Iowa Republican caucus vote. Coincidence, maybe, but traders were caught flat-footed in November 2016 when the US dollar index rallied from 95.87 to 103.65 by mid-December. This week, the DXY rallied from 101.92 on Friday to 103.34 overnight,

Chart: US dollar index

Source: Daily FX

US Retail Sales rose 0.4%, ex autos in December, easily beating the 0.2% forecast and reinforcing Christopher Wallers view that rates should be lowered methodically.

EURUSD is directionless in a 1.0855-1.0885 band. Eurozone HICP inflation was 0.5% m/m which was a tad firmer than expected (forecast 0.4%) and supported calls by numerous ECB officials that it was too early to think about cutting rates. ECB President Christine Lagarde’s seems to agree. She said interest rates would go lower but not until the summer.

GBPUSD whipsawed in a 1.2597-1.2696 range. Broad US dollar strength drove GBPUSD to its session low in Asia then slightly hotter than predicted UK inflation took GBPUSD to its peak before it returned to the middle of the band in NY trading. UK CPI rose 0.4% m/m in December while Core CPI remained unchanged at 5.1% y/y. compared to -0.2% in November(forecast 0.2%) while Core-CPI was 5.1% y/y.

USDJPY traded with a bid in a 147.08-147.99 range, and it is at the top of that band in NY. The gains are underpinned by the rising US 10-year Treasury yield which climbed to 4.106% from 4.06% at yesterday’s close.

AUDUSD has a bearish bias and traded in a 0.6535-0.6595 range. The currency is suffering from a mix of weak Chinese economic growth data and a surging US dollar.

Today’s Fed speak includes remarks from John Williams, Michelle Bowman, and Michael Barr.

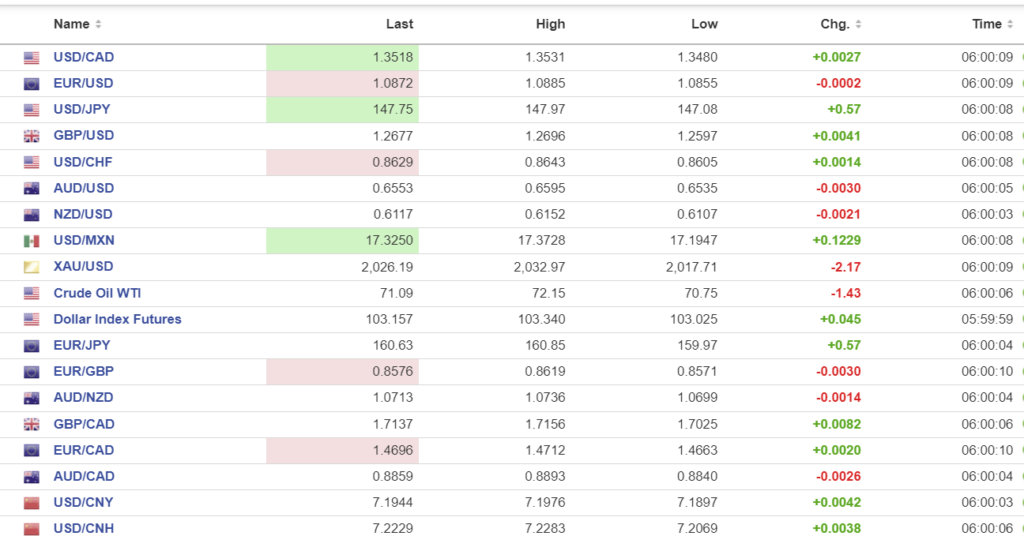

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

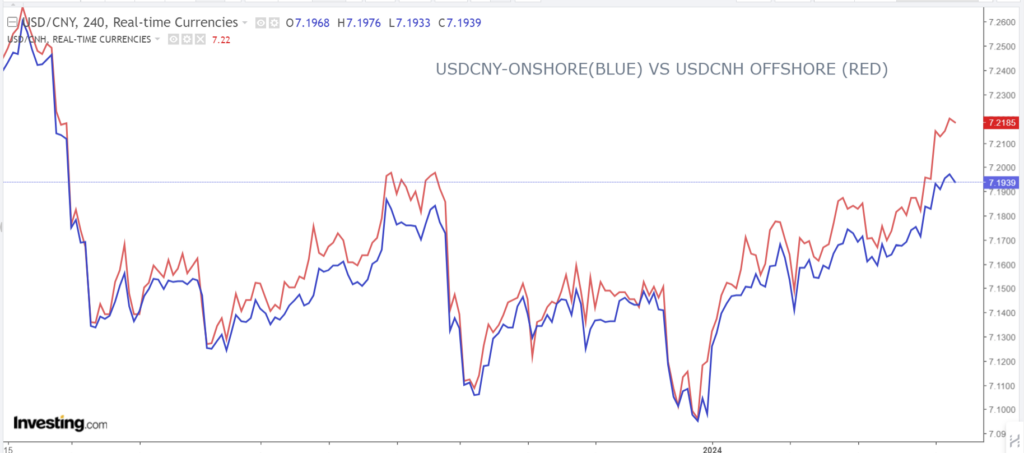

China Snapshot

PBoC fix: today 7.1138, expected 7.1986, previous 7.1134.

Shanghai Shenzhen CSI 300 fell 2.18% to 3229.08.

Chinese data disappoints. Q4 2023 GDP 5.2% y/y (forecast 5.3%) and 1.0% q/q vs 1.3% in Q3. December Retail Sales rose 7.4% y/y (forecast 8.0%).

Chart: USDCNY and USDCNH 4hour

Source: Investing.com