May 29, 2024

- Fed Kashkari’s rate hike comment spooks markets.

- Oil prices rise ahead of Sunday Opec meeting.

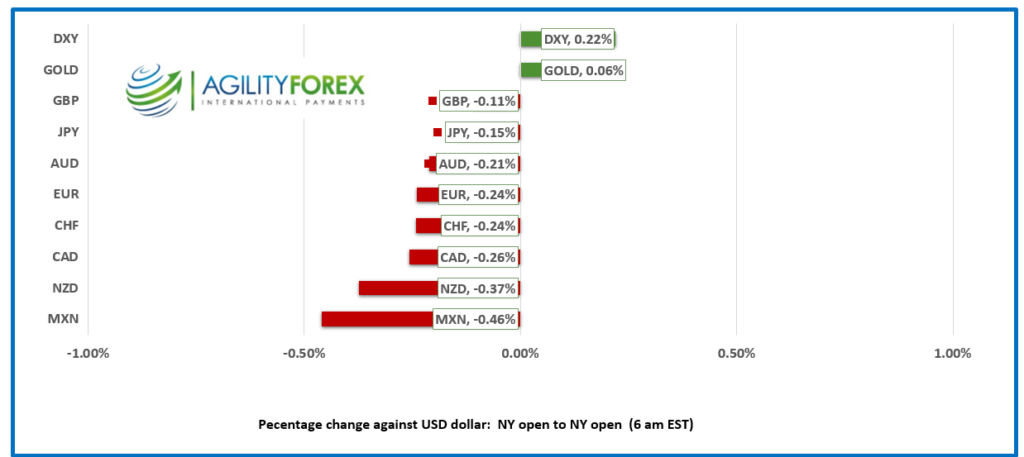

- US dollar opens with small gains. MXN underperforms.

FX at a Glance

Source: IFXA/RP

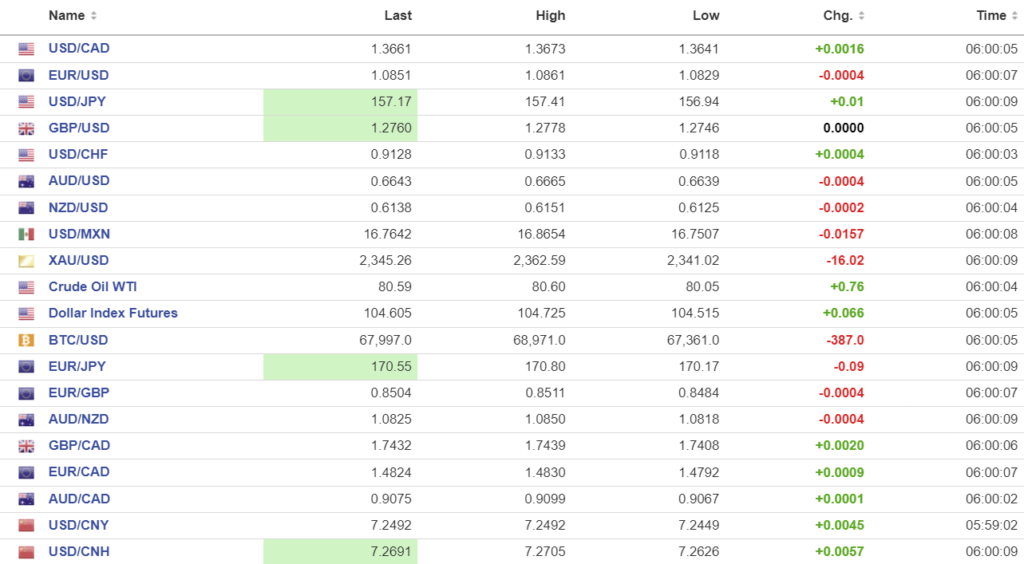

USDCAD open 1.3661, overnight range 1.3641-1.3673, close 1.3645

USDCAD was heading toward support in the 1.3580 area until it slammed into a brick wall made by Minneapolis Fed President Neel Kashkari. His comments about rate hikes still being on the table sent USDCAD bears scurrying for the exits. The USDCAD rally intensified after the poor Treasury auction exacerbated rate hike risks and drove the US 10 year Treasury yield to 4.548% at the close.

USDCAD is trading with a bit of a bid this morning with traders wary about the direction for US Treasury yields and upcoming remarks from Fed policymakers.

WTI oil prices traded narrowly in a 80.05-80.62 ahead of the June 2 Opec meeting. Opec is expected to leave existing production cuts intact and combined with hopes that the US summer driving season will increase demand, are supporting prices.

There is no Canadian economic data today.

USDCAD Technicals

The intraday USDCAD technicals turned bullish with the failure to break support at 1.3610. The subsequent rally above 1.3740 will continue while prices are above this level and is targeting resistance in the 1.3710-30 zone.

The longer term uptrend from January 2024 is intact while prices are above 1.3560. That trendline is supported by the 100 and 200 day moving averages at 1.3571.

For today, USDCAD support is at 1.3650 and 1.3620. Resistance is at 1.3690 and 1.3720. Today’s range is 1.3640-1.3720

Chart: USDCAD daily

Source: DailyFX

Fed Kashkari Terrifies Traders

It is not Friday the 13th, and Neel Kashkari is not Jason. Nevertheless, when the Minneapolis Fed President reminded markets that US interest rate hikes were still on the table, traders screamed in horror. Well, that may be a bit of an exaggeration, but traders sold stocks and bonds and bought US dollars. Kashkari’s comments and a weak 2- and 5-year Treasury auction drove the US 10-year Treasury yield from 4.555% at the NY open to 4.577% overnight. In addition, the odds of a September rate cut fell to 42% from 48%. Gold (XAU/USD) dropped from $3361.52 yesterday to $2346.08 in early NY trading.

The US economic data calendar is light, but NY Fed President John Williams and Atlanta Fed President Raphael Bostic will enlighten markets on the state of US monetary policy.

Donnie Trump is a Nickelback fan.

A New York jury is deliberating on the fate of former President Donald Trump, who is charged with 34 felonies, each carrying a maximum penalty of 4 years. Mr. Trump says he is not worried, but it is rumored that in private he is listening to Nickelback’s “San Quentin” tune and lustily singing, “I’m gonna testify that I was right outta my mind. So can somebody please keep me the hell out of San Quentin?”

EUR/USD

EUR/USD is in the middle of its 1.0829-1.0861 overnight range ahead of today’s German May CPI data. The forecast is for a modest uptick to 2.4% y/y from 2.2%. However, the results should not have any bearing on next week’s ECB decision when a rate cut has been virtually pre-announced.

GBP/USD

GBP/USD is trading in a 1.2746-1.2778 range. Prices are underpinned by EUR/GBP selling due to expectations that the ECB will cut rates faster and deeper than the Bank of England. Even so, it is the outlook for US rates that is driving GBP/USD direction, and the risk of a US rate hike (albeit low) will limit gains.

USD/JPY

USD/JPY rallied yesterday and then drifted in a 156.94-157.41 range overnight. The spike in the US 10-year Treasury yield from 4.455% to 4.54% at the close fueled the gains. Weaker Japanese May Consumer Sentiment (actual 36.2 vs. April 38.3) also supported USD/JPY.

AUD/USD and NZD/USD

AUD/USD churned in a 0.6639-0.6665 range due to the jump in US Treasury yields and higher-than-expected Australian inflation. April CPI was 3.6% y/y, which topped the 3.4% forecast and 3.5% in March and lifted AUD/USD to 0.6665 in the process. ING Bank analysts wrote, “Across the board, inflation components exceeded the 0.25% MoM increase that would be needed to bring inflation to target over the medium term.” The results suggest that the RBA will not be cutting rates in 2024, and even worse, could hike.

NZD/USD traded in a 0.6125-0.6151 range with prices weighed down by the rise in US interest rates. The ANZ Business Outlook Survey showed confidence falling 4 points to 11.2. However, the inflation indicators eased, with inflation expectations falling to 3.6% from 3.8%.

USD/MXN

USD/MXN is consolidating Tuesday’s gains in a 16.7507-16.8654 range. The injection of a Fed rate hike into the conversation fueled the gains. Traders are nervously awaiting Friday’s US PCE-Prices data.

BTC/USD

BTC/USD (Bitcoin) is trading with a slight negative tone in a 67,361-69,971 range. The negative sentiment stems from the hawkish Fed comments yesterday, which led to a spike in Treasury yields.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

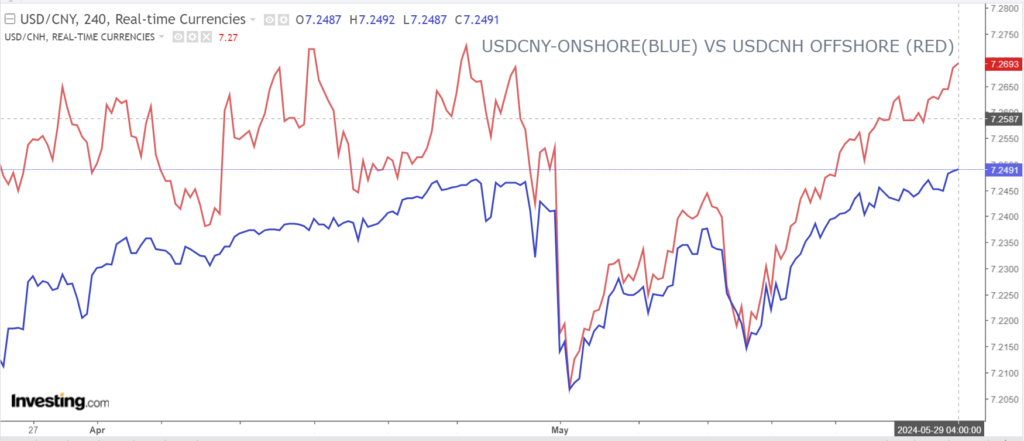

China Snapshot

PBoC fix: 7.1106 vs exp. 7.2528 (prev. 7.1101).

Shanghai Shenzhen CSI 300 rose 0.12% to 3613.52.

The IMF helped give Chinese stocks a lift when it upgraded China’s 2024 growth to 5.0% from 4.6% previously. The IMF said the upgraded is due to the strong expansion at the start of the year and the latest batch of stimulus measures from the government.

Chart: USDCNY and USDCNH

Source: Investing.com