April 11, 2024

- ECB basically pre-announced a June rate cut.

- US PPI data helps soothe CPI angst.

- US dollar opens with large gains compared to yesterday but trades sideways overnight.

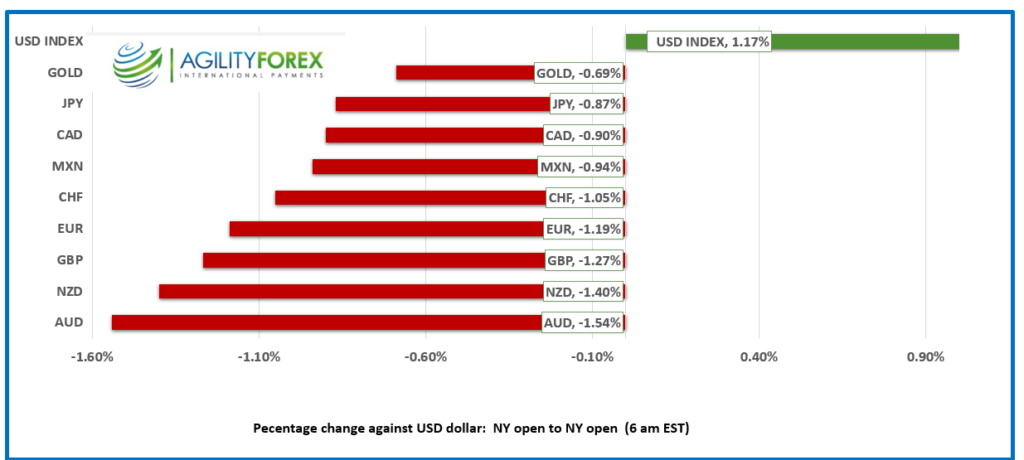

FX at a Glance-Open

Source: IFXA/RP

USDCAD Snapshot: open 1.3689, overnight range 1.3661-1.3695, close 1.3683.

USDCAD soared yesterday thanks to a dovish Bank of Canada monetary policy outlook and higher-than-expected US inflation data. USDCAD rallied from a low of 1.3558 to a peak of 1.3705 due to a tsunami of US dollar demand after traders reassessed their views for Fed rate cuts when US March CPI was a tad higher than expected.

But it was Governor Tiff Macklem who plucked the Loonie’s feathers. Perhaps he thought he was being clever, or perhaps it was a bit of central banker humor, but Mr. Macklem decided that telling Canadians that he would probably cut rates in June was a good idea. It wasn’t. Mr. Macklem has spent his entire career at the Bank of Canada and he has a PhD in economics. He is a smart man, but this smart man makes a lot of dumb mistakes.

For starters, he recently admitted that the bank’s forecasting models needed to be overhauled because they didn’t work. He is also on record for saying that the policy is determined by data and that one or two data points do not make a trend. He is fully aware of the tight Canadian and US economic relationships. So why would he feel the need to prime the rate cut pump in the wake of a surprisingly hot US inflation number, while knowing that his own economic models are suspect? If this was a Hollywood movie remake of “Dumb and Dumber” Tiff would play both roles.

WTI oil prices are modestly bid and trading in an 85.58-86.62 range. News that the EIA reported that US crude inventories rose more than expected was offset by fears of escalating Middle East tensions disrupting oil supplies.

USDCAD Technicals

The intraday USDCAD technicals are bullish with the break above the 1.3580-1.3610 resistance area and the subsequent break above 1.3660. Those moves suggest a revisit to the 1.3995 October peak, with the previous resistance levels reverting to support.

Fibonacci retracement analysis on a daily chart suggests that the break above the 61.8% level at 1.3630 targets 1.3750, the 78.6% retracement level of the November-December range.

For today, USDCAD support is at 1.3660 and 1.3610. Resistance is at 1.3710 and 1.3740. Today’s range is 1.3650-1.3740.

Chart: USDCAD daily

Source: DailyFX

Life is Just a Fantasy

Optimistic traders fantasizing about 75 bps of Fed rate cuts came face-to-face with a snarling CPI print. The slightly hotter-than-expected headline and core inflation figures caught markets wrong-footed, despite analysts speculating that the Fed would only cut twice. The fallout was fast and furious, which is indicative of a market that was positioned for a below-consensus CPI reading. The proof is in the overnight market action, which saw the FX majors little changed from where they closed in NY, and by the 10-year Treasury yield, which opened unchanged from where it closed.

PPI Soothes CPI Angst

Today’s US Producer Prices Index is like Aloe Verde for a sunburns-soothing. PPI rose 0.2% m/m (forecast 0.3% m/m ) while core-PPI rose 0.2% m/m as expected but below the 0.3% result in February. However, the year over year Core-CPI result was worse than expected, rising 2.4%, compared to 2.0% in February. The greenback retreated slightly on the news while the 10-year Treasury yield eased down to 54.538% from 4.56%.

Missiles Underpin Greenback

Geopolitics are also doing its part to underpin the US dollar. The CIA has warned of imminent missile strikes on Israel by Iran or Iran proxies. Russia is launching attacks on Ukraine’s energy infrastructure and cities, and if that’s not all, the US and Japan announced a “new era” of strategic cooperation to counter growing threats from China.

Equities

Asian equity indexes closed with losses led by a 0.44% drop in Australia’s ASX 200. European bourses are in the red ahead of today’s ECB monetary policy meeting, and S&P 500 futures are down 0.29%.

EURUSD

EURUSD dropped yesterday and consolidated its losses in a 1.0726-1.0750 range overnight. The ECB appeared to confirm the speculation about a June rate cut. The statement noted “if the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.” EURUSD barely budged on the news

GBPUSD

GBPUSD is consolidating yesterday’s losses at the bottom of its 1.2531-1.2570 overnight range. The RICS Housing Price Balance dropped 4.0% compared to the consensus forecast for a 6.0% decline. The survey noted that “buyer demand continues to edge higher, while near-term expectations point to activity gaining further traction over the coming months.” Bank of England policymaker, Megan Greene, pushed back against market pricing for UK rate cuts. She said that inflation persistence in the UK “remains higher than in other advanced economies, particularly the US. In my view, rate cuts in the UK should still be a way off as well.”

USDJPY

USDJPY extended yesterday’s gains and rose from 152.75 to 153.29 on the back of the 10-Year Treasury yields surging to 4.566% overnight. The gains were also because traders feel that unless the BoJ hikes interest rates, FX intervention alone will be ineffective

AUDUSD and NZDUSD

AUDUSD traded in a 0.6502-0.6531 range due to post US-CPI demand for dollars and also because of the sharp fall in the Chinese yuan.

NZDUSD tanked yesterday and traded defensively in a 0.5971-0.5993 range overnight. The soft Chinese inflation data which risks deflation is also a NZDUSD negative due to its implication for China and New Zealand trade.

USDMXN

USDMXN traded firmer, rising from 16.4249 to 16.4855 due to broad US dollar demand after markets reassessed the outlook for Fed rate cuts in 2024. A correction was overdue after USDMXN fell over 5% since the beginning of February. Nevertheless, while prices are below 16.6000, the downtrend is intact..

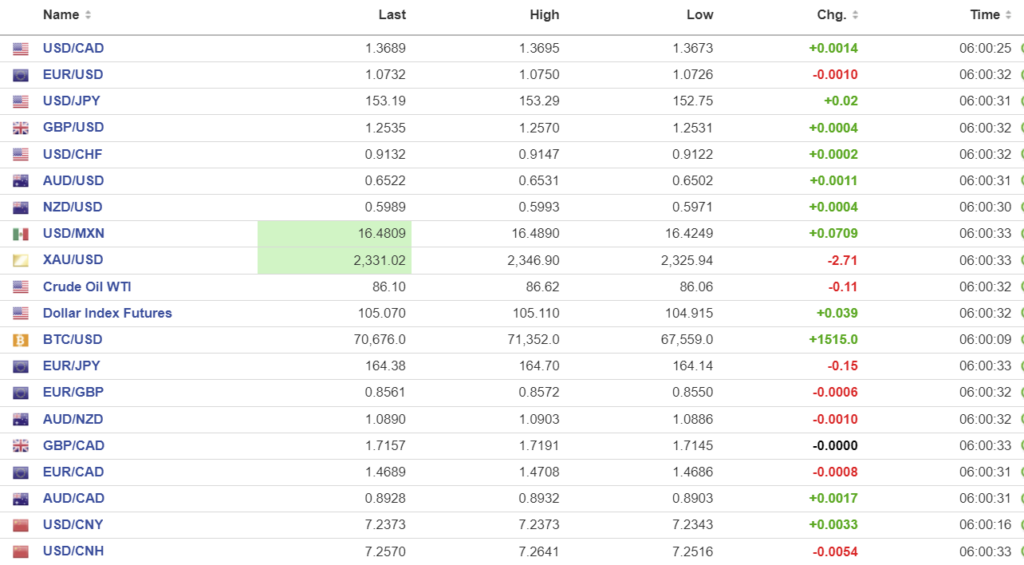

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0968 vs exp. 7.2622 (prev. 7.0959).

Shanghai Shenzhen CSI 300 fell 0.01% to 3504.24.

China March CPI fell 1.0% m/m (forecast -0.5%, previous 1.0%, m/m, CPI rises 0.1% y/y (forecast 0.4%)

Producer Prices fall 2.8% y/y (forecast -2.8%, February -2.7% y/y)

China fixes yuan far below expectations as authorities push backed against offshore yuan weakness following broad US dollar demand, post CPI.

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com