October 2, 2019

USDCAD open 1.3245-49 (6:00 am EDT) Overnight Range 1.3208-1.3248

Today’s ADP employment report showed private sector employment rising 135,000 jobs. The forecast was for an increase of 140,000 and the US dollar inched higher on the news. Yesterday, the weaker than weaker than expected US ISM Manufacturing PMI report (actual 47.1 vs forecast 50.4) reverberated throughout Asia markets. The major equity indices closed in the red, US Treasury yields consolidated losses, and the antipodean currencies edged higher. Traders were also distracted by more Brexit drama, and missiles from North Korea.

The US dollar opened on a mixed note compared to yesterday. The British pound and Australian dollar are the only currencies to have lost ground since yesterday’s open.

FX Market Snapshot

Change in currency value against the US dollar from Tues. New York open to Wed. New York open

North Korea may have launched a missile according to South Korean officials, but FX markets ignored the news. Instead, the focus was on Boris Johnson’s Brexit plans which he will make public today. GBPUSD soared and sank on conflicting rumours yesterday and had a similar, but less volatile pattern overnight. GBPUSD bounced in a 1.2228-1.2308 and opened at the lower end of that range.

EURUSD tracked Sterling moves in a 1.0909-40 range. Weak economic data, bearish technicals and a dovish ECB are weighing on the single currency. Switzerland inflation was weaker than expected

USDJPY failed to break resistance above 108.50 yesterday and plunged on the back of the ISM report and drop in Treasury yields. The currency pair traded with a negative bias in a 107.56-88 band and is sitting at the overnight low in early New York trading.

AUDUSD underperformed against NZDUSD in part due to a report by Goldman Sachs. It said, the Reserve Bank of Australia internal model predicted the need for a $200 billion quantitative easing program to achieve the RBA’s employment and inflation targets. AUDUSD dropped from 0.6717 to 0.6675 on the news.

The American Petroleum Institute (API) weekly crude stock data showed a 5.92 million barrel drop in crude oil stocks for the week ended September 27. WTI prices rallied but only briefly as US recession fears, slowing global growth, and the China/US trade war weigh on prices. WTI fell from $54.78/barrel to $53.08/b yesterday and consolidated those losses in a %53.71-$54.38/b overnight.

USDCAD traders ignored oil price action, preferring to track EURUSD moves. Prices found a floor at 1.3206 when EURUSD gains peaked at 1.0940. Canada GDP was flat in July. The result was expected but supported the Bank of Canada’s view of a slowing domestic economy in the second half.

The Canadian data calendar is empty, and the US calendar is light. The only data on tap is ADP employment, which some traders use as a gauge for the nonfarm payrolls report which is due Friday. US stock futures suggest a negative open on Wall Street today.

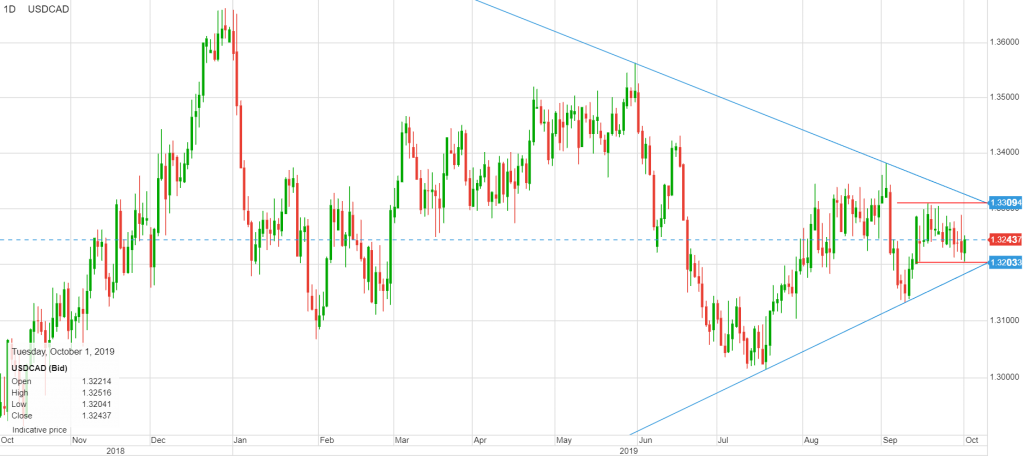

USDCAD Technical View

The intraday USDCAD technicals are unchanged. The currency pair continues to bounce inside the well-defined 1.3200-1.3300 range. Attempts to break support and resistance levels have been rejected. The Bank of Canada’s steady interest rate policy contrasts with the Fed and other major central banks which is capping USDCAD gains. However, broad US dollar strength, and slowing global growth concerns is limiting USDCAD downside. For today, USDCAD support is at 1.3220 and 1.3190. Resistance is at 1.3260 and 1.3290. Today’s Range 1.3210-1.3280

Chart: USDCAD daily

Source: Saxo Bank