August 8, 2024

- US weekly jobless claims lower than expected

- Equity market rally fades

- US dollar opens mixed after quiet overnight session-JPY is the exception.

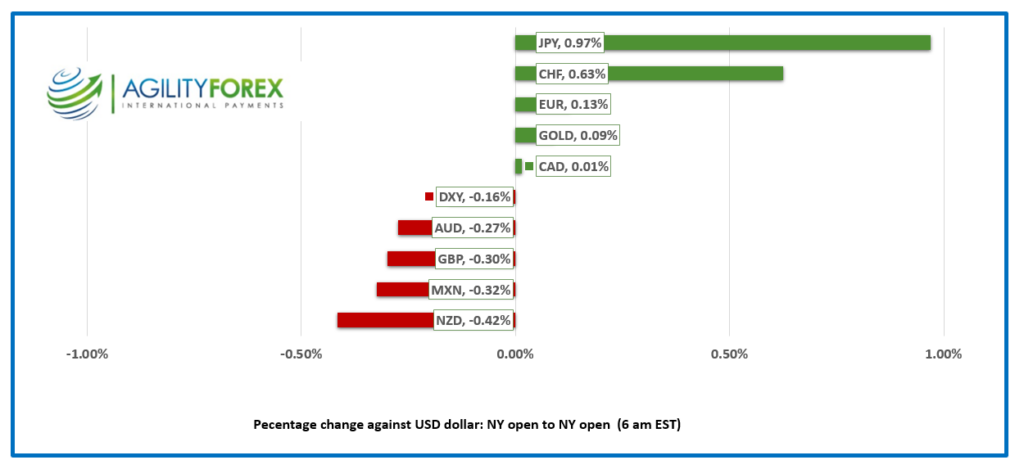

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3746, overnight range 1.3727-1.3762, previous close 1.3760

USDCAD traded inside yesterday’s 1.3721-1.3794 range overnight due to a lack of interest ahead of the US weekly jobless claims data today. Prices popped to1.3762 after the claims numbers were lower than expected.

The Bank of Canada Summary of Deliberations blamed population growth for subdued GDP and why , on a per-person basis, GDP is contracting. They noted that survey results pointed to lower consumer spending and the high cost of building new houses. The weak Labour market is expected to persist. All of the above suggests Canada would fare poorly in the event of a US recession.

The Canadian economic calendar is empty.

.USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3770 on an hourly chart and looking for a break below the 1.3690-1.3710 area to extend loss to 1.3640. A move above 1.370 targets 1.3810.

Longer term, the attached chart shows USDCAD levels every 6 months until 1997. It is rather useless from a charting perspective except to highlight the range for the past 8 years, which is 1.2000-1.4650. The other notable fact is that the uptrend line from July 2021 comes into play at 1.3210. A decisive break above 1.3950 risks a retest of the 1.4650 peak.

For today, USDCAD support is at 1.3720and 1.3690. Resistance is at 1.3770 and 1.3810. Today’s Range 1.3710-1.3790

Chart: USDCAD 6 month bars

Source: DailyFX

“The Only Thing We Have to Fear is Fear Itself” (and a Recession)

JPMorgan Chase said the chances of a US recession by year-end have risen to 35% from 25%, citing “hints at a sharper-than-expected weakening in labor demand and early signs of labor shedding.” A couple of days earlier, Goldman Sachs economists increased the odds of a recession to 25% from 15% but argued that a recession is unlikely. Goldman states that the US economy looks fine overall and that the Fed has ample room to cut rates, which will prevent a hard landing.

Friday’s weak nonfarm payrolls data triggered a broad-based financial market meltdown. Rapidly increasing unemployment and weaker job gains are precursors to a recession. However, today’s weekly jobless claims data (actual 233,000, forecast 240,000, and previous 250,000) helped alleviated those concerns.

Chart: CBOE Volatility Index

Source: CBOE.

Geopolitical Tensions Priming Recession Pump.

A US recession is not necessarily a “Made in the USA” phenomenon. Escalating geopolitical tensions could tip the scales toward a US hard landing. Ukraine is on the offensive and has launched a cross-border attack on Russia using US missiles. Meanwhile, Hezbollah and Iran may be reconsidering a “retaliatory strike” to punish Israel for killing terrorist leaders. The USS Abraham Lincoln battle group will soon be in the region to keep Iran at bay. Israel has also promised a “disproportionate response” if Hezbollah kills any Israeli civilians.

Global Equity Indexes Covered in Red Ink

Asian equity indexes closed with losses. Japan’s Topix fell 1.11%, and Australia’s ASX 200 dropped 0.23%. European bourses were not faring any better until the jobless claims numbers turned things around. The French CAC flipped from being down 1.19% to rising 1.32%. S&P 500 futures are up 0.80%.

FX markets are far more subdued, partly because about 75% of carry trade positions have been unwound, according to JPMorgan.

EURUSD

EURUSD traded in a 1.0920-1.0945 range overnight then dropped to 1.0896 after the US jobless claims data suggested the labour market may not be as soft as indicated by the nonfarm payrolls report.

GBPUSD

GBPUSD traded in a 1.2665-1.2714 range and is testing the low post jobless claims numbers. GBPUSD is adrift due to a lack of actionable UK data.

USDJPY

USDJPY held onto its title of “most volatile G-10 currency,” bouncing in a 145.43-147.22 range with the top seen in the wake of the slightly better than expected US weekly jobless claims data. Traders continue to digest last week’s BoJ rate hike and hawkish rate outlook, and BoJ Deputy Governor Shinichi Uchida apparently downplaying rate hike fears.

AUDUSD and NZDUSD

AUDUSD traded in a 0.6507 to 0.6565 range and barely budged after today’s US weekly jobless claims numbers. and is near the top of that band in early NY trading. Hawkish comments by RBA Governor Michele Bullock suggesting rate hikes were still on the table underpinned prices. A December rate cut is fully prices in but Westpac Bank economists say it won’t happen until February.

NZDUSD traded defensively in a 0.5982-0.6009 range after the RBNZ Survey of Inflation report was released. Lower inflation expectations raised the odds of an RBNZ rate cut next week to over 80%.

USDMXN

USDMXN traded sideways in a 19.2073-19.3779 range then dropped to 19.1424 after Mexican inflation headline and core inflation were higher than expected. In July 2024, total INPP, including oil, increased 0.71 per cent at a monthly rate and 5.46 per cent at an annual rate. In the same month of 2023, it increased 0.32 % at a monthly rate and fell 0.69 per cent at an annual rate. The results may pre-empt a Banxico rate cut today.

Bitcoin (BTCUSD)

BTCUSD traded in a 54,659-57,731 range, nearly identical to yesterday’s overnight band. Traders are cautious due to today’s US jobless claims data and its impact on recession risks.

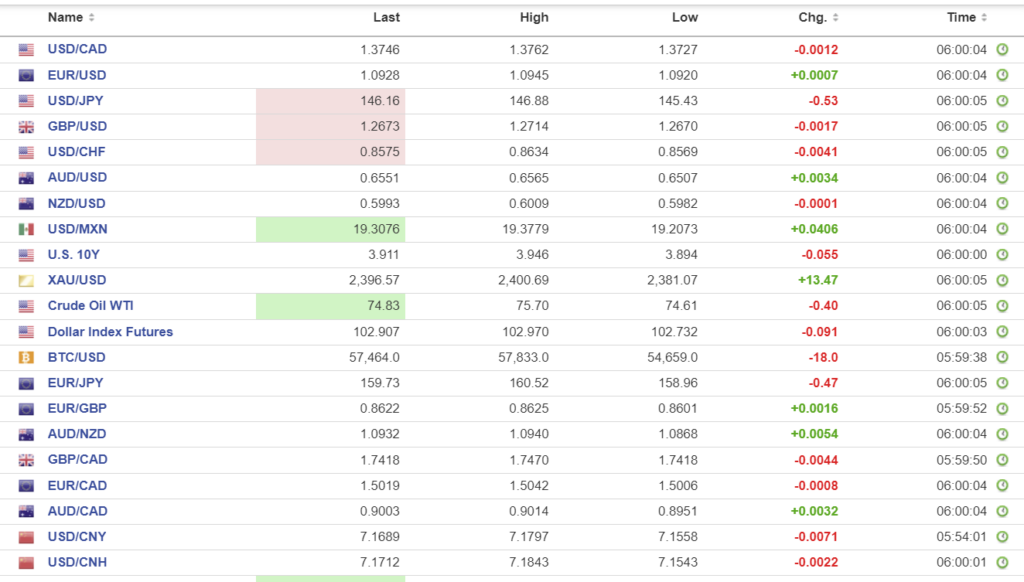

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1460 vs exp. 7.1821 (prev. 7.1386).

Shanghai Shenzhen CSI 300 rose 0.04% to 3342.94

Chart: USDCNY and USDCNH

Source: Investing.com