February 28, 2024

- US 10-year Treasury Yield at 4.29% fuel US dollar rally.

- US Q4 GDP revised down to 3.2% from 3.3%.

- US dollar opens with gains across the board.

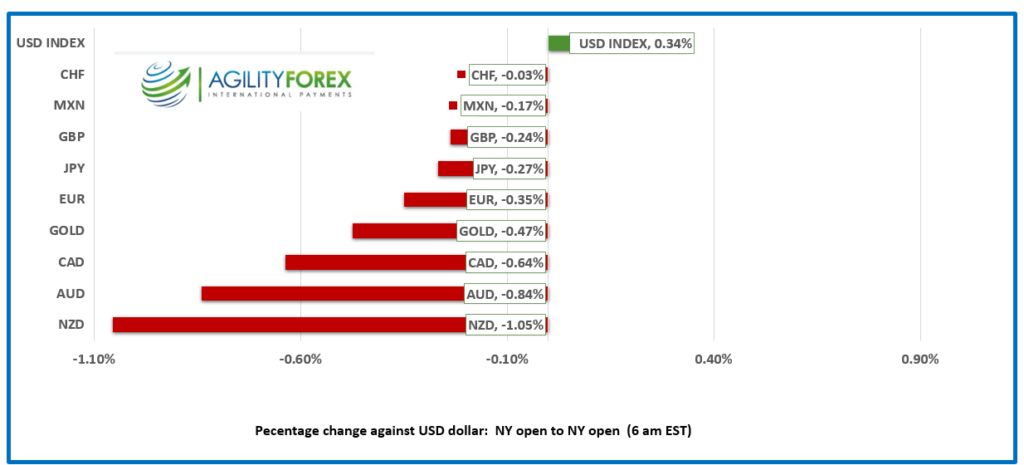

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3577-81, overnight range 1.3524-1.3588, close 1.3531

USDCAD took off like a scared cat yesterday, rising from 1.3484 to 1.3541, then continued the rally overnight, as US 10-year Treasury yields continue to grind higher. However The 10 year yield has dipped to 4.28% this morning which should help to cap USDCAD gains.

WTI oil prices are steady at $78.06/b on talk that Opec may extend voluntary production cuts into Q2.So far, the cuts have only had a limited effect on prices and if forecasts that 2024 crude supply will exceed demand are correct, it is hard to see much upside.

Canada’s Q4 current account deficit narrowed less than expected (actual -$1.62 billion (forecast -$1.25 billion) while the previous data was revised to -$4.74 billion from -$3.22 billion.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3540, looking for a decisive break above resistance in the 1.3590 area to extend gains to 1.3620. A break below 1.3540 suggests further 1.3450-1.3600 range trading.

The Bollinger bands indicate that the latest rally is overdone and vulnerable to a retracement.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3590 and 1.36200. Today’s range is 1.3520-1.3620.

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

It has been a good 24 hours for US dollar bulls in the wake of the US 10-year Treasury yield climbing to 4.32% yesterday from 4.22% on Monday. Markets have chopped Fed rate cut expectations from 175 bps at the beginning of the year to 75 bps now. Coincidentally, 75 bps is what the Fed projected. Perhaps policymakers have a clue.

Asian equity indexes closed close to flat except for the Chinese ones. Hong Kong’s Hang Seng index fell 1.51%. European bourses are mixed. The UK FTSE 100 index is down 0.69%, the German Dax has gained 0.21%, and S&P 500 futures have dropped 0.31%.

Today’s US Q4 GDP ( actual 3.2% vs forecast 3.3%), and quarterly Personal Consumption and Expenditures (actual 2.1% vs forecast 2.0%) were ignored. Traders are eagerly awaiting tomorrows Fed favourite Core PCE price index.

EURUSD traded lower in a 1.0796-1.0848 range, with soft Eurozone sentiment data weighing on prices. Economic sentiment fell to 95.4 from 95.2, Industrial confidence dropped to -9.5 from -9.3, while Consumer Confidence was unchanged at -15.5.

GBPUSD took a dip, juggling between 1.2622 and 1.2689, but the fall was cushioned by a nugget of wisdom from BoE’s Deputy Governor, Dave Ramsden. He’s yet another central banker promoting a wait-and-see position before they even think about trimming rates.

USDJPY rallied with rising Treasury yields, climbing from 150.38 to 150.88. Traders are extremely short, and the BoJ is reluctant to reward them, so they may allow USDJPY to rise enough to trigger stop losses before they intervene.

AUDUSD fell from 0.6550 to 0.6490, where it trades in early NY, as prices tracked broad US dollar demand from firmer Treasury yields. AUDUSD didn’t get much benefit from better-than-expected January inflation data. CPI rose 3.4% y/y, unchanged from December but below the 3.5% forecasted. It is the lowest annual rate since November 2021.

NZDUSD dropped from 0.6178 to 0.6093 where it sits in early NY trading, thanks to a dovish surprise from the Reserve Bank of New Zealand. The central bank was expected to leave rates unchanged at 5.50%, which they did, but leave the door open to further tightening. Instead, they expressed comfort with their inflation outlook and lowered the June OCR (overnight cash rate) forecast to 5.59% from 5.67%, which implies the next move in rates is lower.

USDMXN rallied from 17.0578 to 17.1160 on the heels of broad-based US dollar demand against the majors due to the rise in US Treasury yields.

BTCUSD is having a big week. Prices opened on Monday at $50,981.96 and popped above $60,000 today for the first time since November 2021. The gains are due to the launch of spot Bitcoin exchange-traded funds in January and a bit of a short squeeze. The sharp uptrend is intact while prices are above $57,350.00.

Fed policymakers, Atlanta Fed President Raphael Bostic, Boston Fed President Susan Collins, and NY Fed President John Williams are speaking.

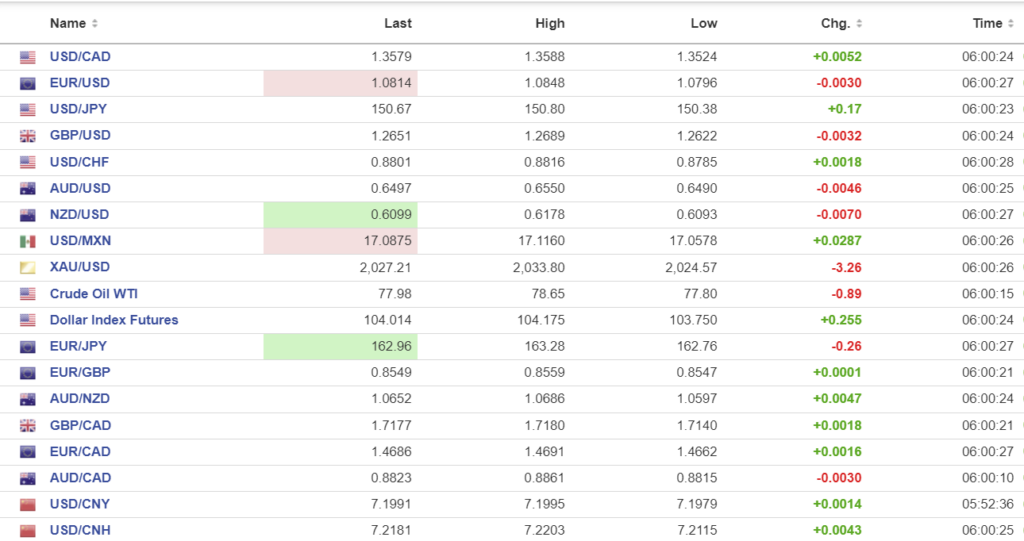

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: closed 7.1075, expected 7.2023, previous 7.1057.

Shanghai Shenzhen CSI 300 fell 1.27% to 3450.26.

China’s equity rally ended abruptly after property developer Country Garden Holdings said Ever Credit filed a petition of liquidation due to the non-payment of a $205 million loan.

Chart: USDCNY daily

Source: Bloomberg