Photo: Bing AI

October 10, 2023

- Monday’s risk aversion sentiment is fading rapidly.

- IMF raises global inflation outlook.

- USD down as rate hike risks fade.

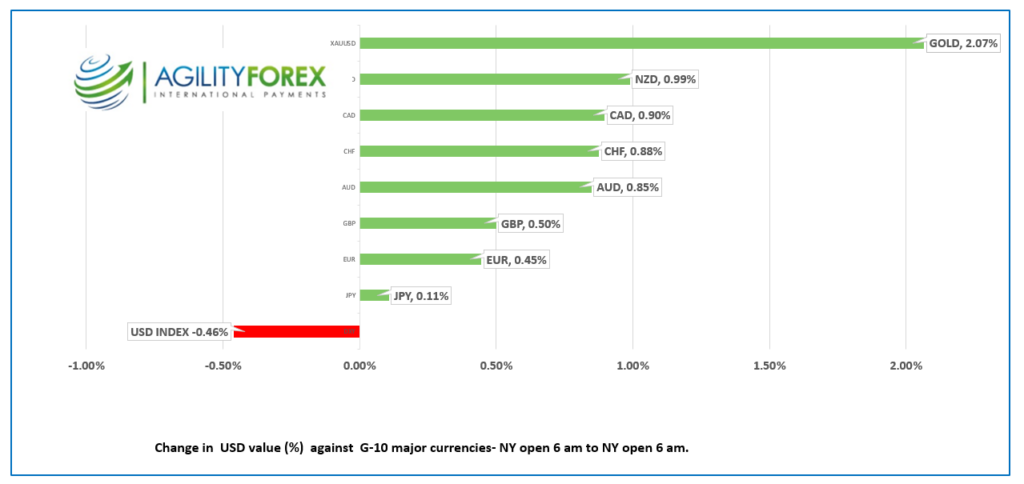

FX at a Glance

Source: IFXA/RP

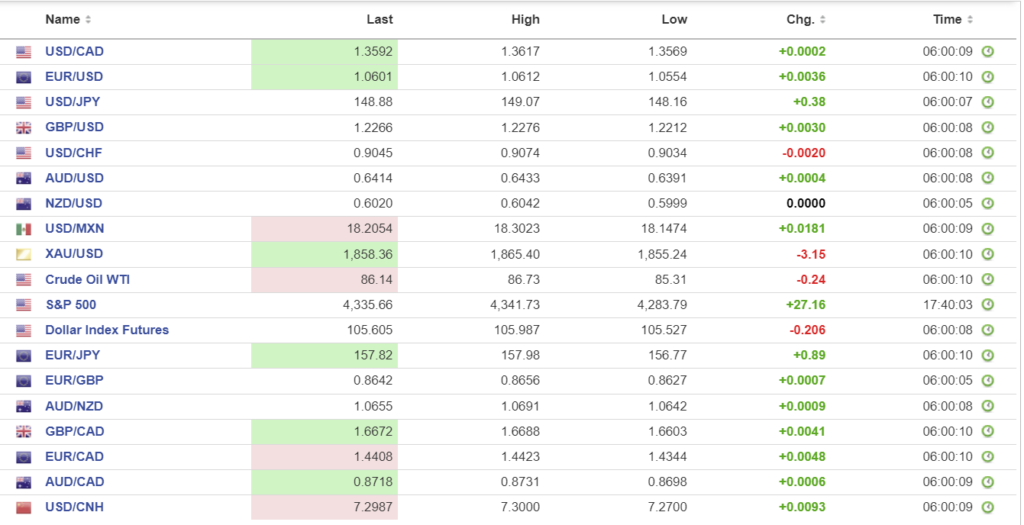

USDCAD Snapshot: open: 1.3592, Range Fri. close. Tues. open: 1.3569-1.3680, Friday close 1.3664

The bottom fell out of USDCAD on Monday following news that heavily-armed Hamas terrorists cowardly attacked Israel, targeting unarmed concert goers, and babies in strollers.

USDCAD dropped in tandem with plunging US Treasury yields and a spike in oil prices which triggered stop-loss selling on the breech of support at 1.3640.

USDCAD was undermined by Friday’s robust employment report which in reality wasn’t that robust as all the gains were due to teachers returning to work. Many economists suggest that the jobs report will not force the BoC to hike rates on October 25.

WTI oil prices spiked 6.0% on Monday, rising from $81.80 to $87.20/b on fears that the Hamas actions will disrupt supplies from the Middle East. Prices have since consolidated in a $85.31-$86.73/range. Talk of new Chinese fiscal stimulus also helped lift prices on anticipation of higher Chinese demand.

USDCAD Technicals

The intraday USDCAD technicals are bearish while prices are below 1.3630 looking for a break below support in the 1.3540-60 area to extend losses to 1.3490. A break above 1.3630 negates the downtrend and targets 1.3750.

Longer term, the uptrend line from July 14 is intact while prices are above 1.3490.

For today, USDCAD support is at 1.3560 and 1.3530. Resistance is at 1.3630 and 1.3680. Todays Range 1.3570-1.3660

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

It’s a risk-off, risk-on world. Financial market traders have already started unwinding safe-haven trades after the terrorist group Hamas attacked Israel. News of the atrocity led to a stampede for Swiss francs, Japanese yen, and US Treasuries, and lifted oil prices off their recent lows.

But that was Monday. After offering the usual and trite “thoughts and prayers,” traders shifted their focus back to the US interest rate outlook. Friday’s blow-out nonfarm payrolls report suggested the Fed would be hiking rates again. However, Fed officials appeared to disagree. Vice Chair Philip Jefferson suggested the Fed could wait due to the lag effect of previous rate hikes and also pointed to high long-term yields. His colleague, Dallas Fed President, agreed, saying, “If long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed funds rate.”

Her remarks helped lift global equities. Asian equity indexes closed higher, with Japan’s Nikkei 225 index gaining 2.43% and Australia’s ASX 200 rising 1.07%. European bourses are sharply higher, led by a 1.71% gain in the German Dax and a 1.51% increase in the FTSE 100 index. S&P 500 futures are up 0.26%, while the US 10-year Treasury yield has inched back to 4.337% after falling from 4.782% at Friday’s close to 4.624% on Monday.

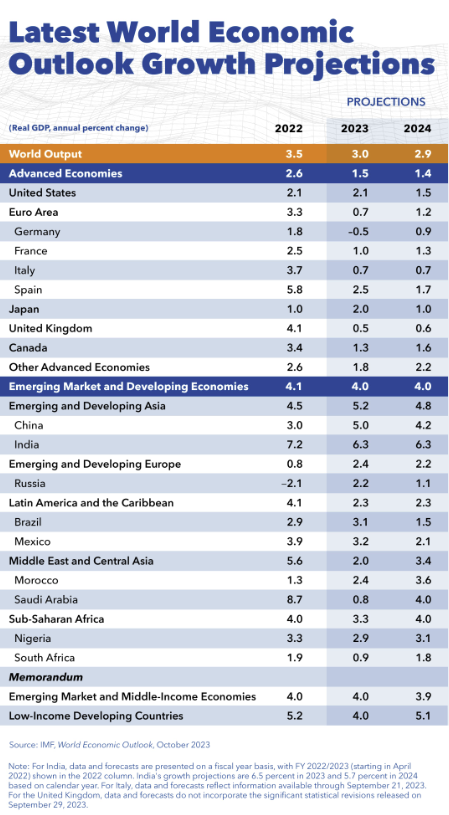

Meanwhile, the IMF is doing its bit to curb the rally, with its latest forecasts calling for interest rates to remain elevated while forecasting global inflation will rise to 5.8% in 2024, compared to its forecast of 5.3% just three months ago

Source: IMF

EURUSD rallied from yesterday’s Asia low of 1.0519 to 1.0612 in Europe, powered by softer US Treasury yields and hopes US rate hikes are a thing of the past.

GBPUSD sank on Monday, falling from Friday’s NY close of 1.2239 to 1.2162 in Asia, then rallied to 1.2262 just before NY opened today. GBPUSD gains are due to yesterday’s dovish Fed comments suggesting US rates may have peaked. The IMF is doing its best to rain on the GBPUSD rally parade. The IMF expects UK growth to have dropped to just 0.5% in 2023 from 4.1% in 2022, with inflation around 7.7% this year.

USDJPY dropped from its Friday close of 149.30 to 148.18 in Asia on Monday due to a wave of safe-haven demand for yen and Treasuries. Prices climbed back to 149.07 overnight after US treasury yields rose modestly, but gains were capped due to speculation that the BoJ will raise its inflation forecast to 3.0% from 2.5% at the October meeting, setting up another yield curve control tweak.

AUDUSD shrugged off initial weakness from the terrorist attack on Israel and traded firmly from a 0.6342 low Monday to 0.6433 in Asia overnight before drifting down to 0.6415 in NY. Prices garnered a bit of support from Consumer Sentiment rising 2.9% to 82 in October from 79.7 in September. Even so, the index is still deeply in pessimistic territory.

The US data calendar is light but there are three Fed officials speaking today. (Waller, Kashkari, Daley

FX high, low, open

Source: Investing.com

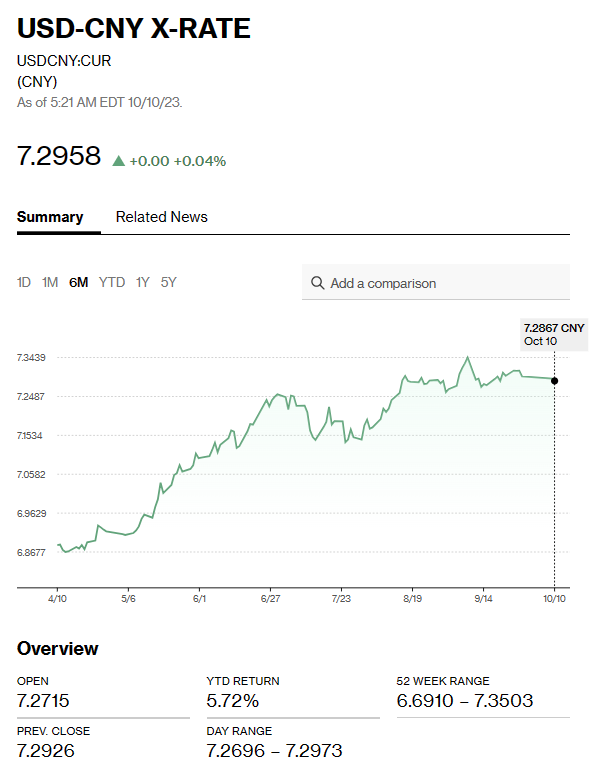

China Snapshot

Bank of China Fix: today 7.1781, Monday 7.1789, Friday 7.1798.

Shanghai Shenzhen CSI 300 fell 0.75% to 3657.13.

Bloomberg reports Chinese authorities are contemplating new fiscal stimulus of $137 billion on infrastructure projects.

Chart: USDCNY

Source: Bloomberg