Source: Clip-art-Library.com

- GBPUSD in turmoil-No confidence in Chancellor, or Bank of England

- US 10-year Treasury yield eases to 3.839% from 3.912% yesterday

- US dollar retreats from NY closing levels, but still higher compared to Monday open

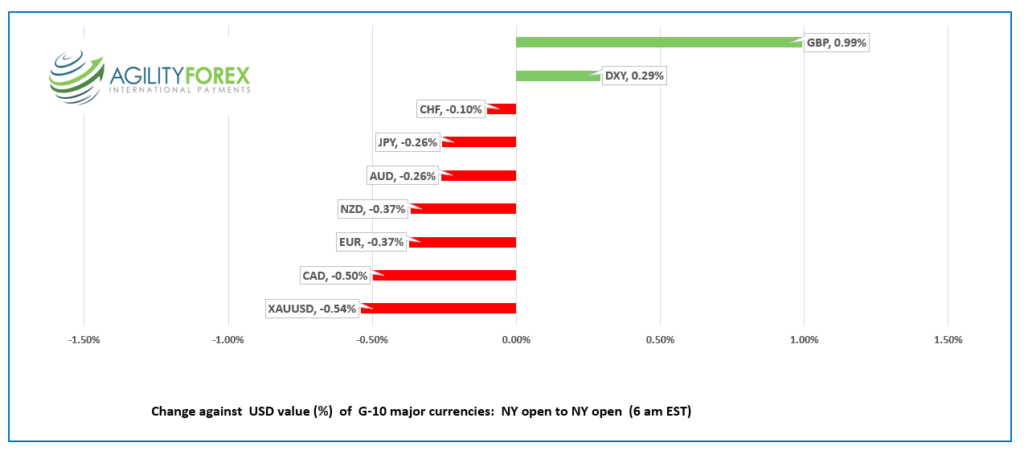

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3709-13, overnight range 1.3642-1.3740, close 1.3740

USDCAD spiked to 1.3809 yesterday, coinciding with the S&P 500 index dropping to 3,644.76 and the US 10-year Treasury yield touching 3.91%.

The USDCAD strength was powered by external forces which included hawkish Fed rate rhetoric, fears Russia will go nuclear in Ukraine, the GBPUSD crisis fueling risk aversion demand for US dollars, and weaker commodity prices. Those same factors will govern trading today.

WTI oil touched $80.24/b yesterday and the bottomed out at $76,25 in early Asia, mainly due to the surging US dollar. Oil prices are struggling to gain upward momentum because of rising global recession fears and slowing growth in China. Goldman Sachs cut their 2022 forecast from $125.00/barrel to $100.00/b.

There are no Canadian economic reports today.

USDCAD Technical outlook

The intraday USDCAD are bullish above 1.3640, looking for another move above 1.3740 to retest yesterday’s 1.3809 peak. A break below 1.3640 suggests a drop to 1.3540 (4-hour chart. The September 13 uptrend line is intact above 1.3540.

For today, USDCAD support is at 1.3630 and 1.3580. Resistance is at 1.3720 and 1.3750. Today’s range: 1.3630-1.3730

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

US Durable Goods Orders dipped for the second consecutive month, falling-0.2%, compared to a 0.1% dip in July. The results were better than expected but ignored by markets.

Traders are licking their wounds after Monday’s free-for-all that saw the soaring 10-year US Treasury yield come within spitting distance of 4.0%, GBPUSD collapse, and the venerable Dow Jones Industrial Average close in bear territory. The Boomtown Rats sang about hating Monday, and Wall Street rats croon about hating September since historically it is the worst month for stocks.

The outlook for higher US interest rates was at the forefront yesterday after a gaggle of Fed policymakers championed the need for higher rates to tame inflation and then suggested they would need to remain elevated far longer than previously expected.

Nothing new there. It has been the story since Fed Chair Powell’s Jackson Hole speech at the end of August.

Russia’s phony referendum in Ukraine and reports that Putin will formally announce the occupied Ukraine lands as being part of Russia on Friday are keeping European traders on edge.

The British Pound is well on its way to dropping a weight class and becoming the British Ounce.

Will rookie Chancellor of the Exchequer Kwasi Kwarteng and the imbeciles at the Bank of England be sacrificed to the market gods?

Investors are rather unhappy about the surge in government spending in the face of soaring inflation and a fractured central bank. Speculation is rife that BoE policymakers will hike rates at an unscheduled meeting shortly.

GBPUSD rebounded sharply from yesterday’s “flash crash” low. The currency pair is garnering a bit of support from speculation the Bank of England may have an emergency meeting and hike interest rates to provide the currency with some support. Nevertheless, the GBPUSD outlook is negative.

EURUSD is at 0.9635 in NY, after bouncing in a 0.9585-0.9670 band overnight. Gains are limited due to the weak Eurozone economic outlook, the ongoing energy crisis, and Russia’s threat to use nukes in Ukraine. The short term technicals are bearish below 0.9680.

USDJPY rose to 144.72 from 144.07 after the US 10-year Treasury yield touched 3.91%. Prices dropped on fears of Bank of Japan intervention and softer yields which fell to 3.837% in NY today.

AUDUSD rose steadily in a 0.6454-0.6512 range while NZDUSD rallied from 0.5635 to 0.5720 after comments from RBNZ Governor Orr. He said the tightening cycle is mature but there is still room to tighten monetary policy further.

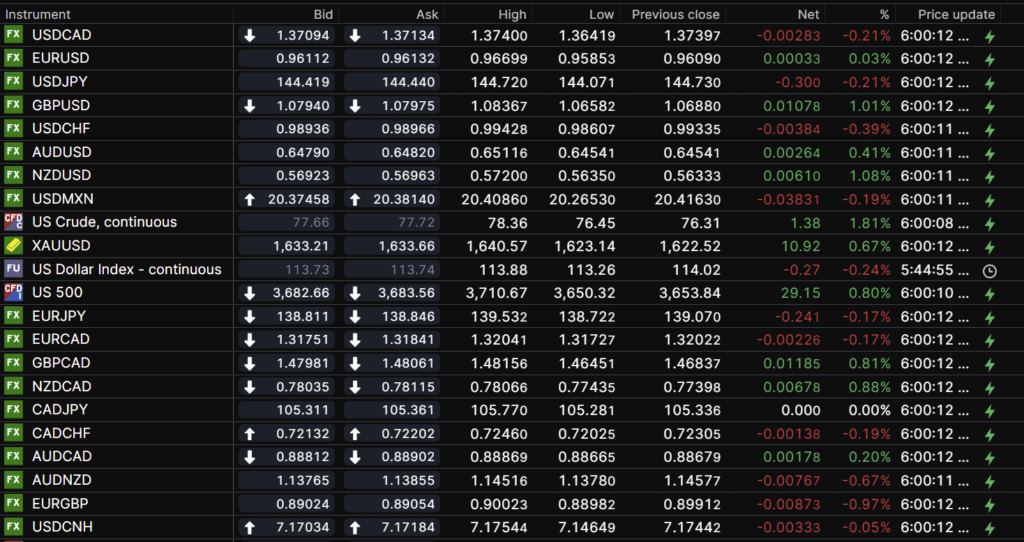

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

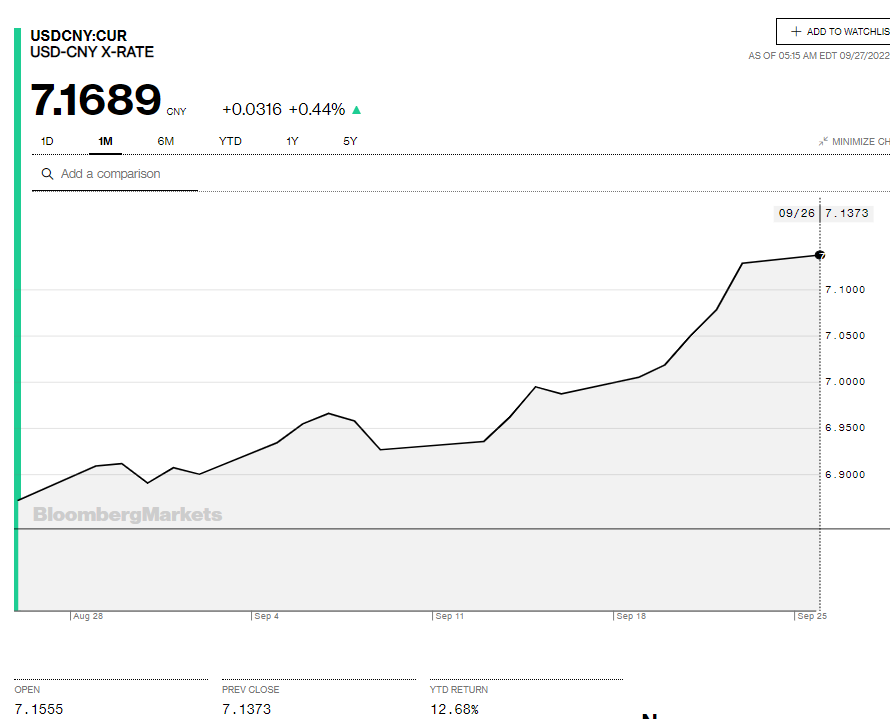

China Snapshot

Today’s Bank of China Fix: 7.0722, previous 7.0298

Shanghai Shenzhen CSI 300 fell 0.34% to 3,856.02

Growth concerns an issue after World Bank predicted China’s growth would lag that of the rest of Asia for the first time since 1990. Xi Jinping’s zero-tolerance covid policy and ongoing real estate drama are behind the weakness.

Chart: USDCNY 1 month

Source: Bloomberg