Source: Pixabay

- Meat Loaf off the menu

- Russia and rate hike risks sour sentiment

- US firms on safe-haven demand

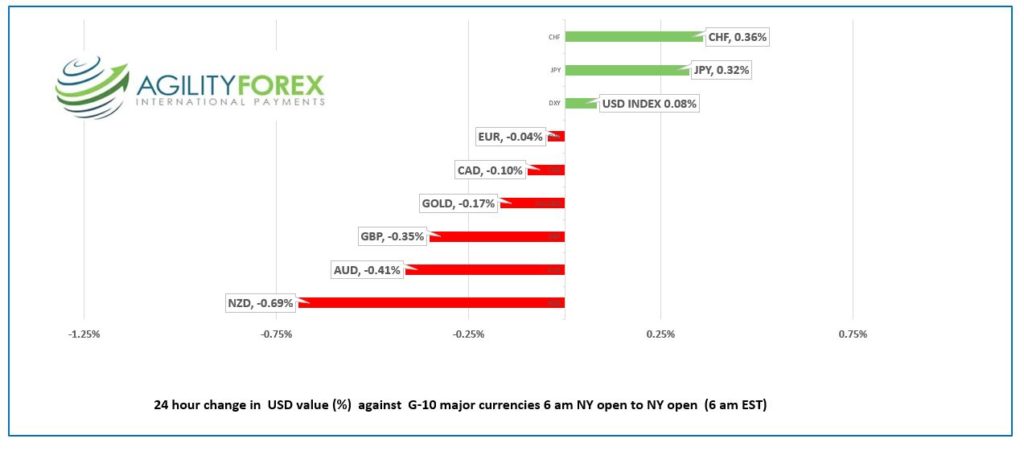

FX at a Glance

Source: IFXA Ltd/RP

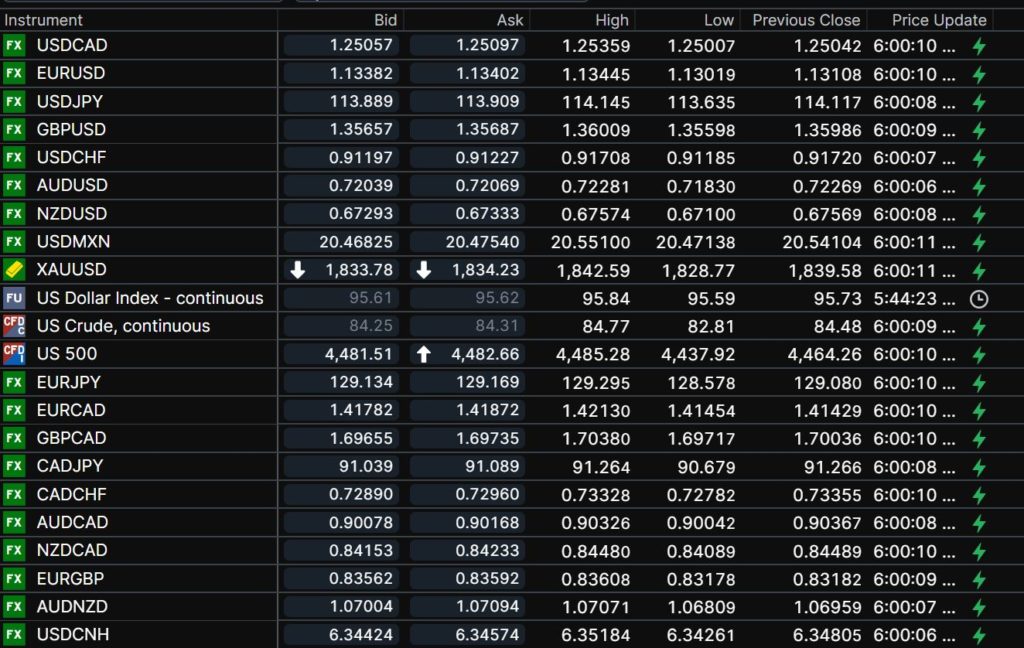

USDCAD Snapshot: Open 1.2506-10, Overnight Range-1.2501-1.2536, previous close 1.2504

USDCAD rallied alongside sliding US equity prices yesterday and consolidated those gains in a narrow band overnight. Prices rallied to the top of the range in early NY trading following renewed equity weakness.

Prices were underpinned by softer oil prices. WTI dropped from $87.39/b yesterday to $82.89/b in Asia on profit-taking after US weekly crude inventories were a tad higher than expected. Oil prices remain supported by geopolitical tensions, and forecasts for rising demand.

USDCAD traders are awaiting next week’s Bank of Canada interest rate statement and Monetary Policy Report. There is a debate as to whether the Bank hikes interest rates by 0.25% or uses Omicron as an excuse to leave policy unchanged. Some in the “unchanged” camp suggest the Governor Tiff Macklem will prefer to follow, not lead the Fed. Maybe they will be surprised.

The FOMC meeting (on the same day) is expected to set the stage for a March rate hike, The debate is whether the hike will be 25 or 50 basis points.

Canada Retail Sales are expected to have risen 1.2% m/m in November compared to October’s1.6% increase. The data is stale and should not be a factor for FX, especially with the BoC meeting looming.

Technical view: The intraday USDCAD technicals are bullish above 1.2490, which guards the weekly uptrend line at 1.2430. A break above 1.2570 targets 1.2630, while below 1.2490 suggests a retest of 1.2450.

For today, USDCAD support is at 1.2490 and 1.2460. Resistance is at 1.2550 and 1.2570. Today’s Range 1.2470-1.2550

Chart USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

The dashboard light blinked out, and the world is a darker place. Global traders are uneasy as the hostile rhetoric between Russia and the US intensifies, and rising inflation threatens steep increases in interest rates.

The US approved NATO members sending US made weapons to Ukraine. Will Russia approve sending missiles to Cuba?

Asia equity indexes closed in the red again. Hong Kong’s Hang Seng Index closed unchanged, helped by more minor easing by the PBoC. The German DAX index is down 1.54%, leading European bourses lower. S&P 500 and DJIA futures extended yesterday’s losses after pandemic-favourite stocks, Netflix and Peloton tanked. Gold prices consolidated earlier gains but opened a tad weaker. US 10-year Treasury yields retreated to 1.79% from 1.827%.

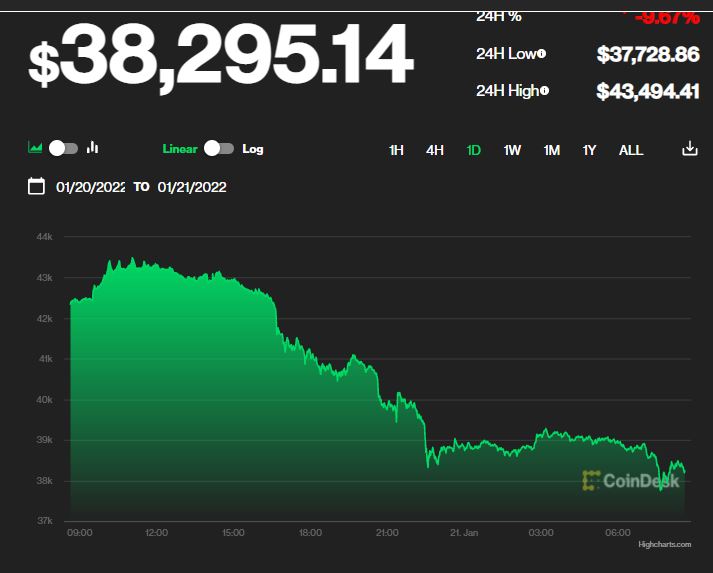

Bitcoin (BTCUSD) lost ground as risk sentiment soured and officials focused on bitcoin miners’ energy consumption.

EURUSD traded quietly in a 1.1302-1.1345 range, garnering a bit of support from rising Bund yields which narrowed. The single currency is also underpinned by the modest dip in US Treasury yields.

GBPUSD is at the bottom of its 1.3555-1.3600 range. Traders were disappointed by weaker than expected Retail Sales (-3.7%, forecast -0.6%, November 1.0% m/m) and Consumer Confidence data (actual -19, previous -15).

The poor results were blamed on rising inflation. Nevertheless, prices are underpinned by expectations that the Bank of England raises interest rates by 0.25% February 3.

USDJPY retreated from 114.15 to 113.64 due to safe-haven demand for yen and modestly softer Treasury yields. Japan inflation data was mixed. December CPI rose 0.8% vs 0.6% y/y in November, while Core CP fell to -0.7% from -0.6% y/y.

AUDUSD and NZDUSD dipped on broad US dollar demand and lower commodity prices. New Zealand PMI was 53.7, lower than expected but higher than November’s result.

There are no US economic reports today.

Chart of the Day: Bitcoin (BTCUSD)

Source: coindesk.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

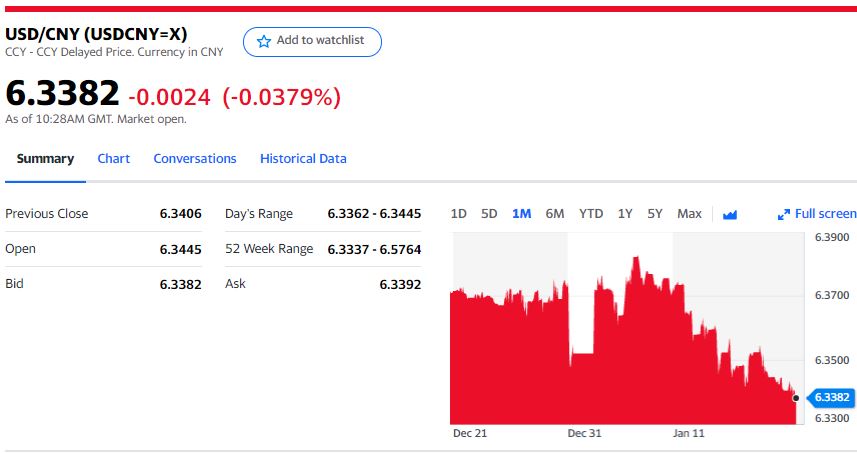

China Snapshot

Today’s Bank of China Fix 6.3492, previous 6.3485

Shanghai Shenzhen CSI 300 FELL 0.92% to 4,779.31

PBoC trims overnight, 7-Day and 1-month Standing Lending facility by 10 bps to 2.95%, 3.10% and 3.45%, respectively.

Chart: USDCNY 1 month

Source: Yahoo Finance