Photo: BingAI

June 30, 2023

- US PCE data ticks lower

- Canada April GDP flat compared to forecast for 0.2% rise.

- CAD poised to end June as best performing currency vs US dollar.

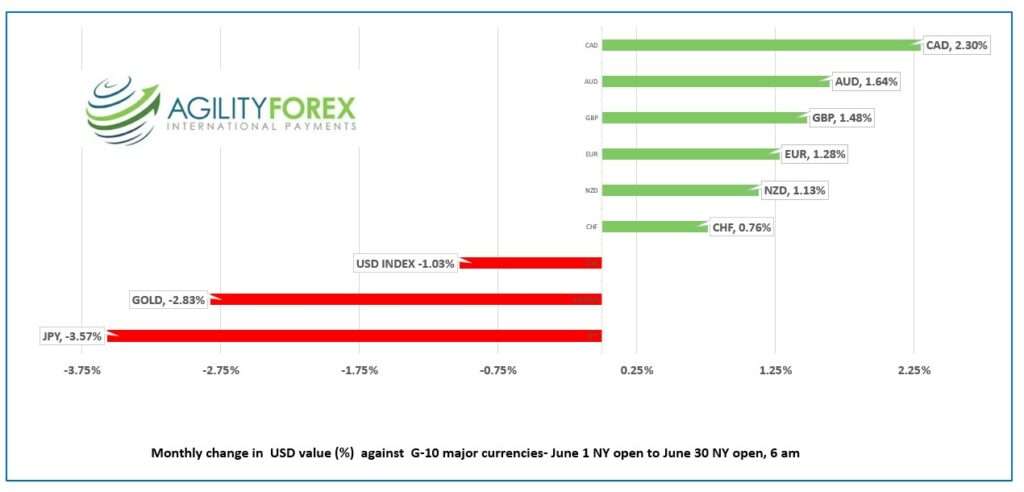

Monthly FX at a glance

Source: IFXA Ltd/

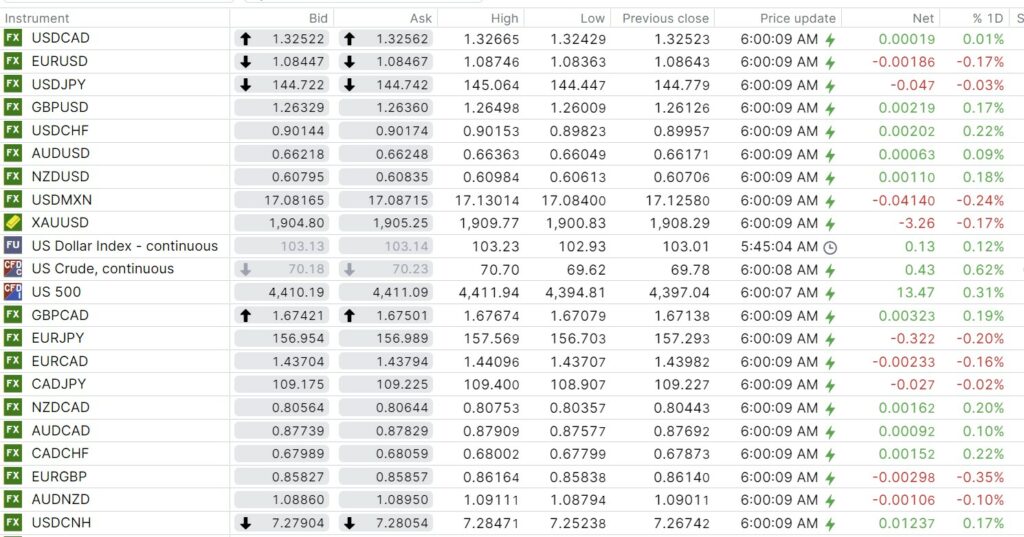

USDCAD Snapshot: open 1.3252-56, overnight range 1.3243-1.3267, close 1.3252

USDCAD lost 2.3% from the NY open on June 1 to today, mainly due to the Bank of Canada’s surprise 25 bp rate hike on June 7, which lifted the overnight rate to 4.75%. That hike squeezed the CAD/US 10-year interest rate differential to its narrowest level for the month (-28.6 bp), while the 2-year CAD/US interest rate differential turned positive (6.7 bp). The spreads have widened out to -50.5 bp and -21.7 bp, respectively.

The Bank of Canada releases its quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations today at 10:30 am EDT. Both surveys will be scrutinized for evidence that the aggressive BoC rate hikes are having a dampening effect on inflation expectations.

Canada’s economy stagnated in April (actual 0.0% m/m) likely due to the impact of the Public Sector strikes. The results suggest the BoC may be less motivated to raise rates on July 12.

WTI oil prices shuffled between $69.62 and $70.70/b, underpinned by hopes for renewed Chinese demand while the risk of higher US rates caps gains.

Canada is closed Monday.

USDCAD Technical Outlook

The USDCAD technicals are unchanged from Thursday. They are bullish while trading above 1.3240, looking for a decisive break above 1.3280 to extend gains to 1.3350, which if broken targets the 100 and 200-day moving averages at 1.3493 and 1.3412, respectively.

Longer term, the downtrend from the 1.3855 March peak is intact while prices are below 1.3550.

For today, USDCAD support is at 1.3240 and 1.3180. Resistance is at 1.3280 and 1.3330.

Today’s range 1.3180-1.3280

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

The US economy continued to flex its muscles yesterday when Q1 GDP rose 2.0% (forecast 1.3%), and Initial Jobless Claims fell 26,000 to 239,000, rather than remaining unchanged as anticipated.

The strong data followed hawkish comments from Fed Chair Powell, suggesting at least two more interest rate hikes because monetary policy was not sufficiently restrictive to lower inflation. Cleveland Fed President Raphael Bostic countered by saying he doesn’t see the need for more hikes, but since he is not a voting member, his remarks were ignored.

The Fed’s favorite inflation gauge, Core-PCE, ticked lower in May. Core-PCE rose 0.3% m/n compared to April’s 0.4% rise and was 4.6% y/y compared to 4.7% in April. The results are not enough to stop the Fed from raising rates in July, but could raise questions about the September decision.

Asia equity indexes were little changed at the close, but the Nikkei 225 finished the month with a 7.45% gain, while Australia’s ASX 200 rose 1.58% for June. European bourses are robust, led by a 1.19% rise in the German DAX, which is on pace to close with a 3.0% gain in June. S&P 500 futures are up 0.45%, and the S&P 500 index is on pace to close June with a 5.20% gain.

EURUSD traded in a 1.0836-1.0875 range, then rose to 1.0889, post US data. Eurozone HICP fell to 5.5% May, (April 6.1% y/y), however core HICP rose to 5.4% y/y from 5.3%. The news won’t prevent another ECB rate hike in July. The intraday EURUSD technicals turned bullish with the move above 1.0880 and are targeting 1.0960.

GBPUSD is at the top of its 1.2601-1.2690 range with the peak occurring after the US PCE data. The UK Q1 GDP rose 0.1%. GBPUSD is modestly bullish and attempting to recover yesterday’s losses.

USDJPY traded in a 144.35-145.06 range due to higher US 10-year Treasury yields, which rose from and dovish BoJ monetary policy. Tokyo inflation data was a tick lower than expected, but May Industrial Production fell 1.6% m/m (forecast 0.7%).

AUDUSD traded in a 0.6605-0.6651 with prices tracking broad US dollar sentiment and supported by the risk of another RBA rate hike in July.

The US is closed Tuesday July 4 and many traders have booked off Monday as well.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

China Snapshot

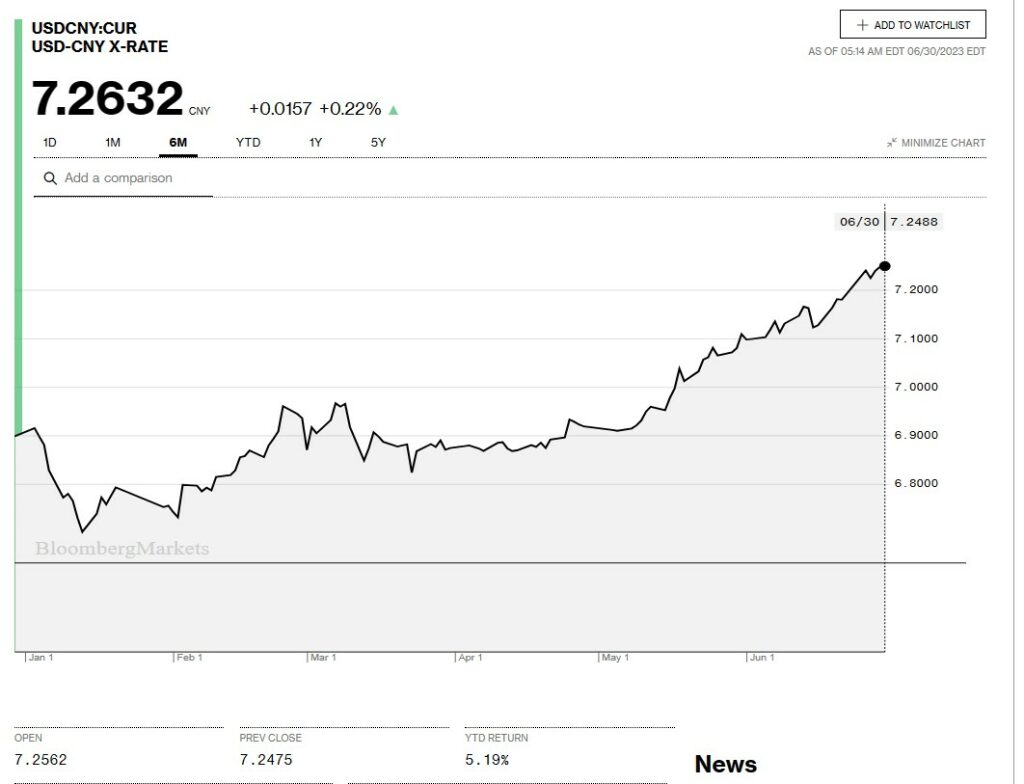

Bank of China Fix: 7.2258, previous 7.2208

Shanghai Shenzhen CSI 300 rose 0.54% to 3842.45.

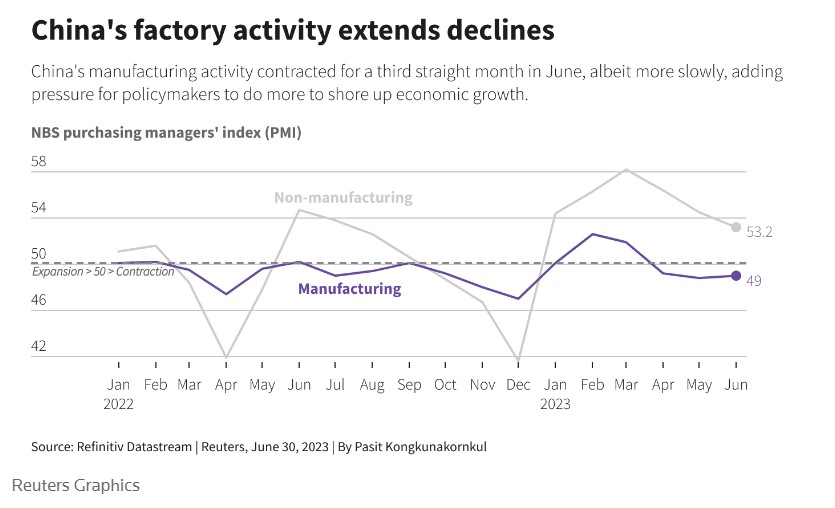

NBS June Manufacturing PMI 49 (forecast 49, May 48.8)

NBS Non-manufacturing PMI 53.2 (forecast 50.8, May 54.5)

Chart: USDCNY 6 month

Source: Bloomberg