Photo: creazilla

June 1, 2023

- Markets back to expecting the Fed to pause in June.

- US ADP rises higher than expected.

- USD drifts lower in cautious overnight session.

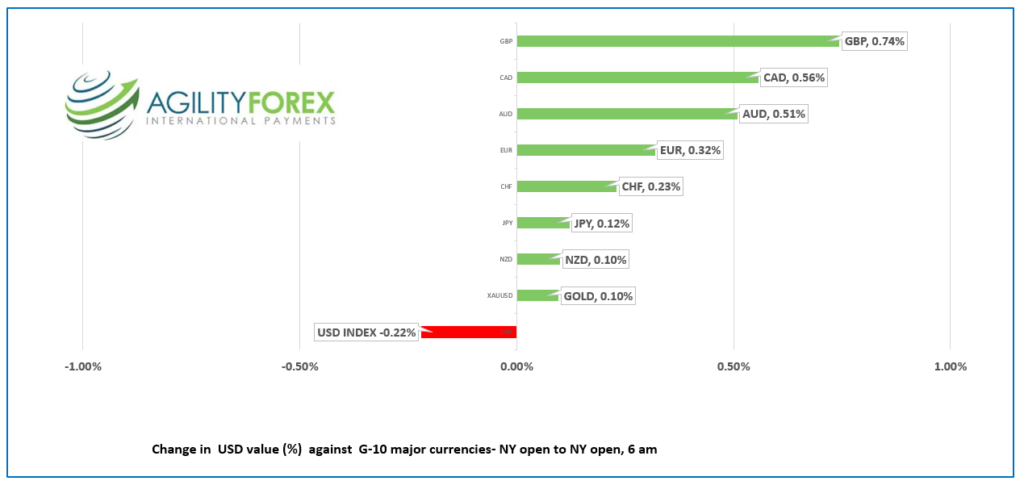

FX at a glance

Source: IFXA Ltd/RP

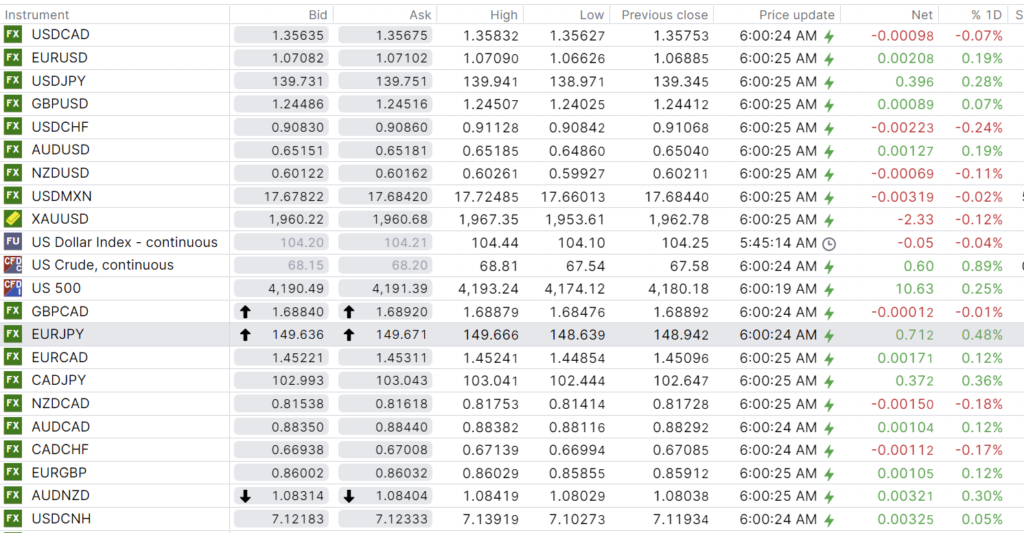

USDCAD Snapshot: open 1.3564-68, overnight range 1.3546-1.3583, close 1.3575.

USDCAD retreated yesterday and extended the losses overnight and in early NY trading. The drop occurred following the US House of Representatives passing the debt ceiling deal along with the improved risk sentiment from downgraded US rate hike concerns.

Prices are also seeing support from expectations the Bank of Canada will hike rates by 25 bps next week, supported by a spate of robust domestic data and yesterdays stronger than expected GDP data.

Traders are ignoring the slide in WTI oil prices which fell from $68.81/barrel to $67.54. Global growth concerns stemming from China’s weak-post pandemic rebound are weighing on prices. Prices are vulnerable to a rebound ahead of this weekend’s Opec meeting.

There is no Canadian data of note today.

.USDCAD Technical Outlook

The intraday USDCAD technicals continue to flip between bullish and bearish within the confines of the broad 1.3250-1.3650 range. At the moment they are bearish while prices are below 1.3580 looking for a break below 1.3540 to extend losses to 1.3480. A break above 1.3580 targets 1.3640.

The uptrend line from May 4 is intact while above 1.3540. If broken, USDCAD will retest support at 1.3400.

For today, USDCAD support is at 1.3540 and 1.3480. Resistance is at 1.3580 and 1.3640.

Today’s range 1.3480-1.3580

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Fed-speak and Chinese data turned the frown upside down. The last day of May was shaping up to be bullish for the US dollar and bearish for stocks until Fed officials began flapping their gums.

Soon-to-be Fed Vice Chair Philip Jefferson and Philadelphia Fed President Patrick Harker spoke about “skipping” an interest rate hike in June. Harker said skipping means rates can still rise higher while a pause means they are on hold for a while.

The CME Fedwatch tool flipped from a 67% chance of a rate hike on June 14, to a 68% chance rates will be left unchanged.

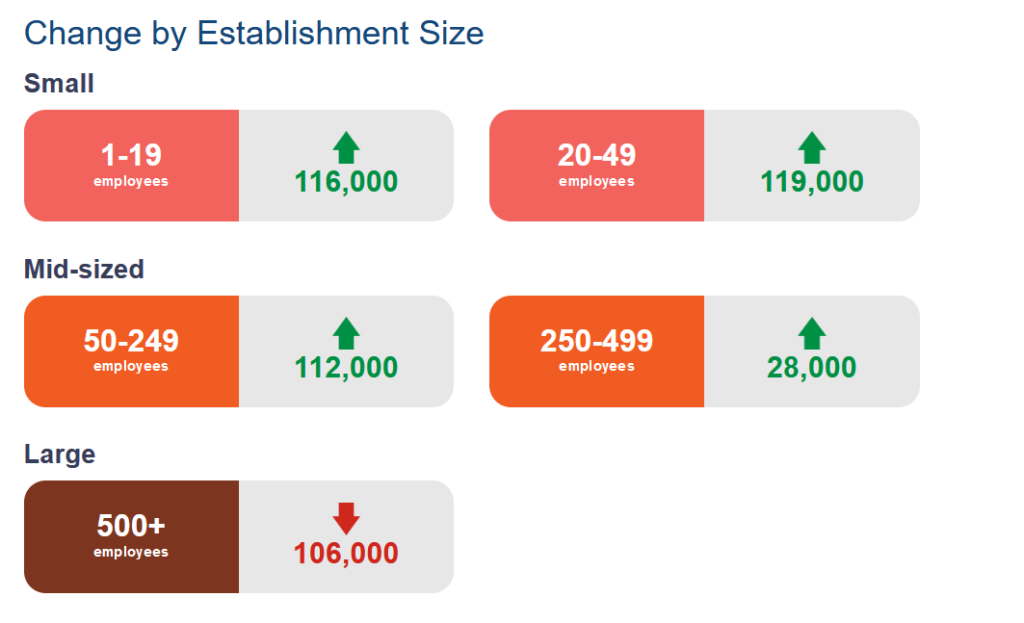

Those odds may change again, today. US weekly jobless claims rose 2,000 while the ADP Job change report showed private sector employment rising by 278,000 jobs. The report also noted that pay increased 6.5% y/y which is down 1.0% from the previous month.

Chart: Change in employment

Source: ADP

Risk sentiment improved in Asia, helped by news that the US House passed the Debt Ceiling deal. Sentiment got perkier after the Caixin China Manufacturing Index rose to 50.9 which was higher than the expected 49.5, suggesting that the Chinese economy was no longer contracting.

The major Asian equity indexes closed with gains (except the Hong Kong Hang Seng Index) and European bourses are sharply higher. The German Dax is up 1.18% while the UK FTSE 100 index has gained 0.60%. S&P 500 futures have gained 0.27%.

EURUSD traded in a 1.0663 to 1.0715 range and prices are hovering around 1.0700 in NY. Eurozone May inflation fell to 6.1% y/y from 7.0% in April (forecast 6.3%), which serves to make the ECB rate hike debate murkier. A decisive move above 1.0720 will negate the EURUSD downtrend that has been in place since the beginning of May.

GBPUSD rallied from 1.2403 to 1.2482 in NY supported by downgraded Fed rate hike expectations and better than expected UK Manufacturing PMI (actual 47.1, vs forecast 46.9).

USDJPY churned in a 138.97-139.94 range and is trading at 139.20 in NY. Talk that the Fed will skip a rate hike in June fueled the sell-off while the Jibun Bank Manufacturing PMI (actual 50.6 vs April 50.9) did not have much impact.

AUDUSD rallied to 0.6557 in NY from an Asia low of 0.6486 thanks to Fed officials contemplating skipping a June rate increase. Caixin Chinese PMI data was better than expected which underpinned prices while Australian Manufacturing PMI data was largely ignored.

US construction spending, and ISM Manufacturing PMI are ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

China Snapshot

Bank of China Fix: 7.0965, previous 7.0821.

Shanghai Shenzhen CSI 300 rose 0.22% to 3806.87.

Caixin Manufacturing PMI rises higher than expected to 50.9 (forecast 49.5) helping to improve risk sentiment in Asia markets.

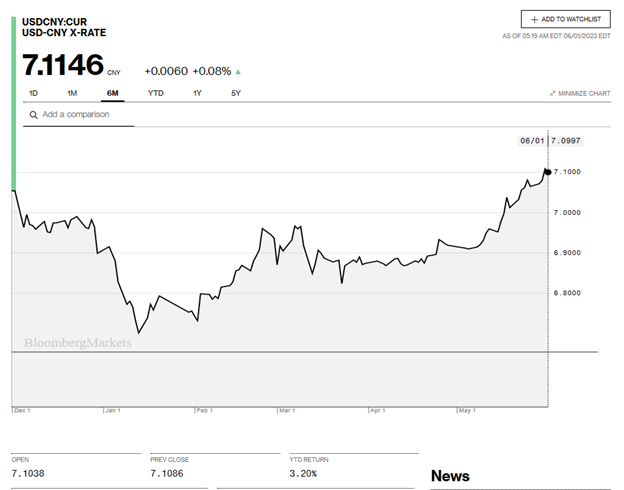

Chart: USDCNY 6 month

Source: Bloomberg