Photo: pixabay

February 23, 2023

- FOMC minutes, mildly hawkish but very stale

- US Q4 GDP dips to 2.7% (forecast 2.9% y/y)

- US dollar opens mixed, commodity currency bloc slightly higher.

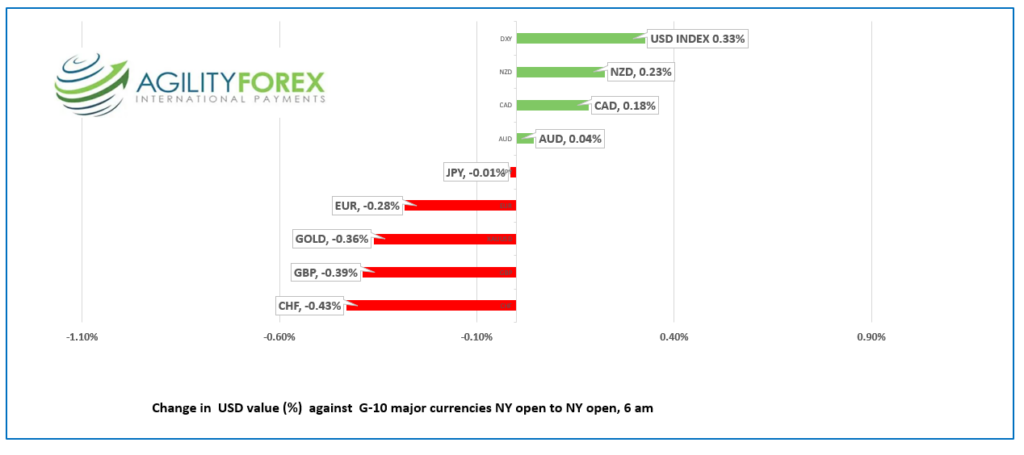

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3520-33, overnight range 1.3520-1.3551, close 1.3552

USDCAD attempted to break through resistance in the 1.3560-70 area following the release of the FOMC minutes but failed. However, the retreat has been rather shallow which suggests another re-test is inevitable.

USDCAD continues to be underpinned by the Bank of Canada’s announcement that it is pausing rate hikes, even as the US plans for at least another 75 bps of rate increases. The drop in oil prices added additional support to the currency pair.

WTI oil traded in a $73.86/b-$74.96 range overnight after falling from $76.23/b. Tuesday, the American Petroleum Institute said crude inventories rose 9.895 million barrels last week after rising 10.5-million-barrels the week before.US dollar strength, post-FOMC minutes was another factor.

USDCAD direction will track S&P 500 moves today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish above 1.3490, looking for a break above 1.3580 to extend gains to 1.3700. The 100-day moving average at 1.3510 guards support at 1.3490 which if broken will extend losses to 1.3430, then 1.3360.

For today, USDCAD support is at 1.3490 and 1.3460. Resistance is at 1.3580 and 1.3660.

Today’s range 1.3460-1.3560

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The FOMC minutes were mildly hawkish but too stale for markets to care. A series of robust top-tier data released since February 1 changed the landscape for policymakers. Nevertheless, the minutes showed the Fed plans a few more rate increases to take the Fed Funds rate to the 5.50% area.

Wall Street did not get too excited. The DJIA and S&P 500 indexes closed modestly lower while the NASDAQ managed a small gain. Asian equity indexes closed negatively led by a 1.34% drop in Japan’s Nikkei 225 index.

European bourses are posting gains led by a 0.57% rise in the German Dax. The UK FTSE 100 is the outlier as it is down 0.13% (as of 5:50 am PT). S&P 500 futures are inching higher (+0.11%), while the US 10-year Treasury yield is a 3.963% compared to yesterday’s close of 3.923%.

Turkey slashed its interest rate by 0.50% to 8.5% (as expected) in an on-going, yet misguided effort to combat inflation which was 57.68% in January.

The US Bureau of Economic Analysis (BEA) reported “GDP increased at an annual rate of 2.7 percent in the fourth quarter of 2022, after increasing 3.2 percent in the third quarter. The increase in the fourth quarter primarily reflected increases in inventory investment and consumer spending that were partly offset by a decrease in housing investment.”

US weekly jobless claims were 197,000 in the week ending February 18, a drop of 3,000, and better than expected.

The data did not have much impact on markets.

EURUSD bounced from the low but remains in the 1.0587-1.0627 overnight range. EURUSD is being pressured because traders believe the Fed is more hawkish than the ECB which overshadowed upwardly revised Euro inflation data. EURUSD is in a short-term downtrend channel bound by 1.0540 and 1.0680.

GBPUSD is trading in a 1.2016-1.2074 band. Hawkish comments from Bank of England’s policymaker and Catherine Mann warning that rates may have to stay higher and longer if the BoE fails to hike now. GBPUSD is bullish above 1.1990.

USDJPY is modestly bid, rising from 134.72 in Asia to 135.36 in NY after today’s data dump, before retreating to 135.20.-134.99 range. Kazuo Ueda the Japanese government nominee for BoJ governor testifies tomorrow.

AUDUSD traded in a 0.6805-0.6841 range with US dollar demand following the FOMC minutes offset by AUD demand due to the prospect of RBA rate hikes.

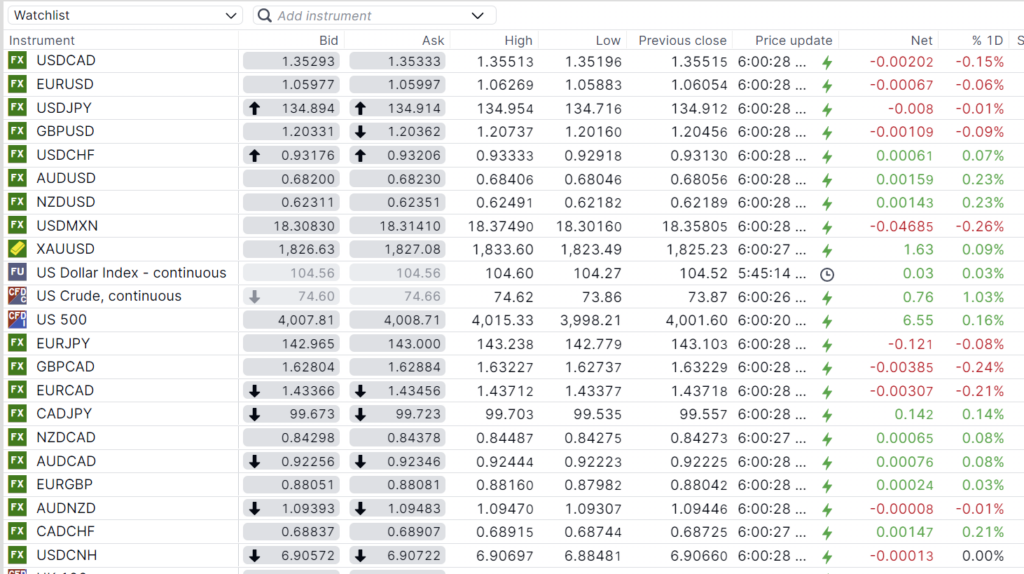

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

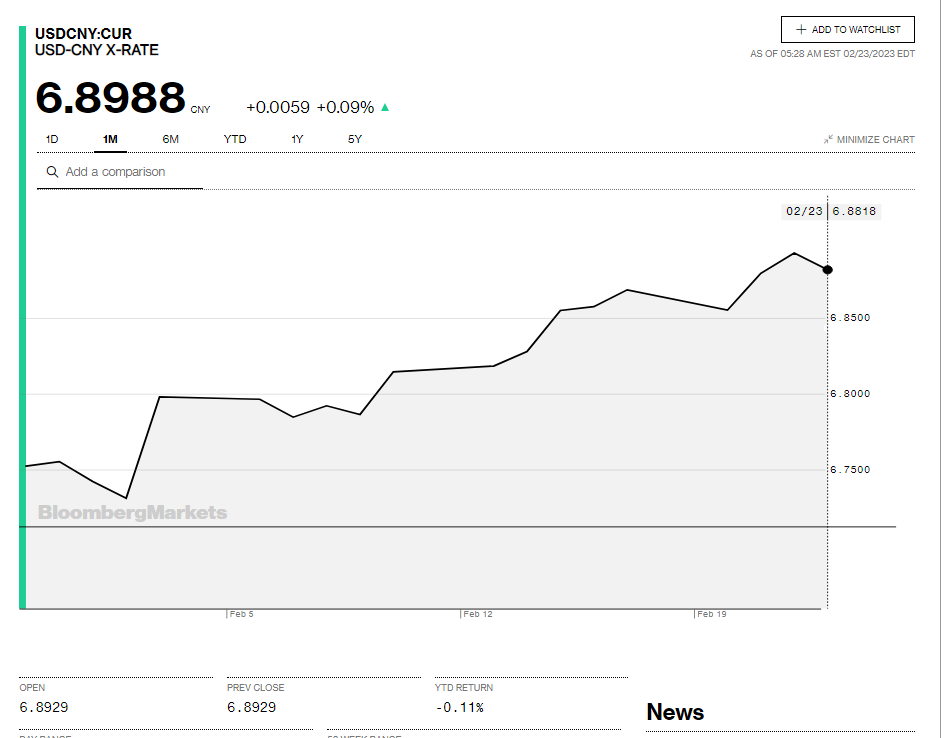

China Snapshot

Bank of China Fix: 6.9028, Feb. 20, Previous: 6.8759

Shanghai Shenzhen CSI 300 fell 0.06%% to 4103.65.

Chart: USDCNY 1 month

Source: Bloomberg