Photo: pixabay

April 26, 2023

- Microsoft and Alphabet earnings help traders forget Republic Bank woes.

- Sweden’s Riksbank hikes 50 bps as expected, suggests another 25 bp in the cards.

- US dollar flexes muscles against commodity currency bloc but falls vs Europe and JPY.

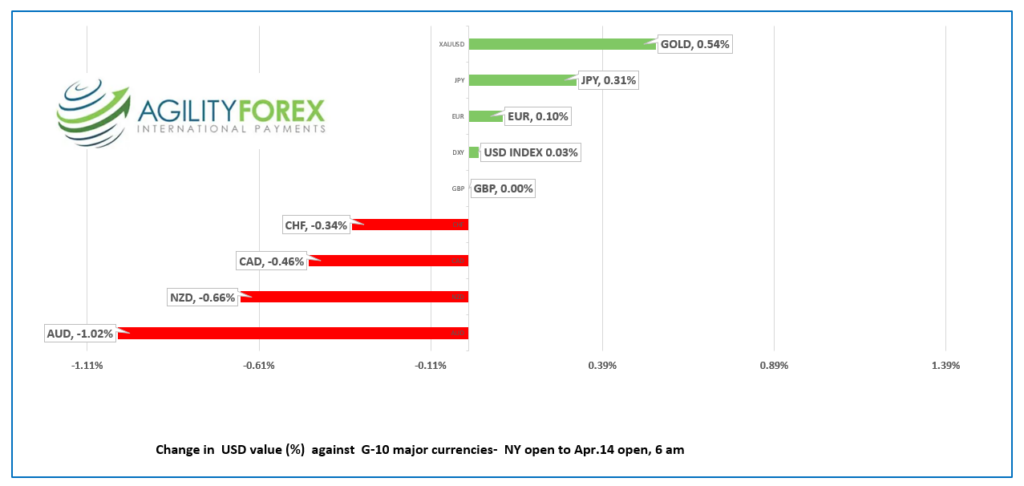

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3634-38, overnight range 1.3616-1.3641, close 1.3627

The First Republic Bank woes and a soft US consumer sentiment report soured risk sentiment and sent USDCAD soaring from 1.3527 to 1.3645 by mid-afternoon yesterday. Prices consolidated the gains in a 1.23616-1.3641 range overnight, supported by struggling oil prices which have failed to maintain upside momentum, following the surprise Opec production cut at the end of March.

WTI oil rallied in early Asia, rising from $77.03/b to $77.90/b after the American Petroleum Institute (API) reported crude inventories fell by 6.08 million barrels in the week ending April 21. However, ongoing US recession fears led to prices retreating to $76.39in early NY trading.

The Bank of Canada releases its Summary of Deliberations from the April 12 meeting at 1:30 pm today. They are not expected to reveal any fresh insight, especially because Governor Macklem has been chatting up a storm since April 13.

There is no Canadian economic data on tap.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish (hourly chart), but the rally is losing momentum in front of the 1.3650-60 resistance zone. Failure to extend gains above 1.3660 followed by a move below 1.3600 will extend losses to the April 14 uptrend line at 1.3530.

A break above 1.3700 sets the stage for further gains to 1.3900 while a break below the 1.3550 area (which is just about the mid-point of the January-March range) targets 1.3230.

For today, USDCAD support is at 1.3590 and 1.3560. Resistance is at 1.3650 and 1.3700

Today’s range 1.3570-1.3650

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

There is nothing like a bank crisis to send investors stampeding toward the exits. That’s what happened yesterday after First Republic announced it lost more than $100 billion of client deposits which sent its stock price down 50%. Negative sentiment was further exacerbated when the Conference Board’s consumer confidence index fell 2.7 points in April to 101.3.

Asian equity indexes closed with losses, following the lead from Wall Street. Japan’s Nikkei 225 index fell 0.71% while Australia’s ASX 200 finished unchanged. European bourses opened in the red and have continued to inch lower. The German Dax is down 0.62%. S&P 500 futures trimmed earlier gains and are up just 0.18% as of 5:40 am PDT. Gold is modestly higher while and WTI oil prices are down.

Headline US Durable Goods Orders soared 3.2% m/m in March, blowing away the forecast of an 0.8% increase and well above the downwardly revised 1.2% seen in February.

EURUSD soared from 1.2404 to 1.2483 just before NY opened, fully recouping yesterday’s losses after the First Republic Bank stock rout sparked a wave of “risk-off” selling. Sentiment improved after-hours when Microsoft (MSFT: Nasdaq) and Alphabet (GOOGL) reported better than expected earnings. The gains accelerated after Sweden’s Riksbank hiked rates 50 bps and indicated at least one more hike was in the cards.

GBPUSD found a bit of a floor at 1.2390 yesterday and drifted in a 1.2404-1.2483 range overnight and opened unchanged from Tuesday. Analysts expect GBPUSD to re-visit the 1.2550 area following encouraging UK data and the prospect of higher UK rates. However, GBPUSD gains will be hampered by EURGBP demand if the outcome of next week’s ECB meeting is as hawkish as expected.

USDJPY consolidated yesterday’s losses in a 133.40-133.92 range. Safe-haven demand for yen following the First Republic Bank woes and the drop in the US 10-year Treasury yield from 3.477% to 3.98% at the close fueled the selling pressure. Also, analysts expect a dovish outcome from Friday’s Bank of Japan monetary policy meeting.

AUDUSD gave up early Asian gains following a higher than expect CPI print. Prices rose from 0.6626 to 0.6638 after headline Q1 CPI rose 6.3% m/m (forecast 6.5%) then dropped to 0.6599 by the time NY opened. The CPI details were soft, giving the RBA and excuse to leave rates unchanged at the May 2 monetary policy meeting. In addition, prices were weighed down by negative risk sentiment.

Today’s US data includes March Durable Goods Orders (forecast 0.8%, previously -1.0%) and Wholesale Inventories.

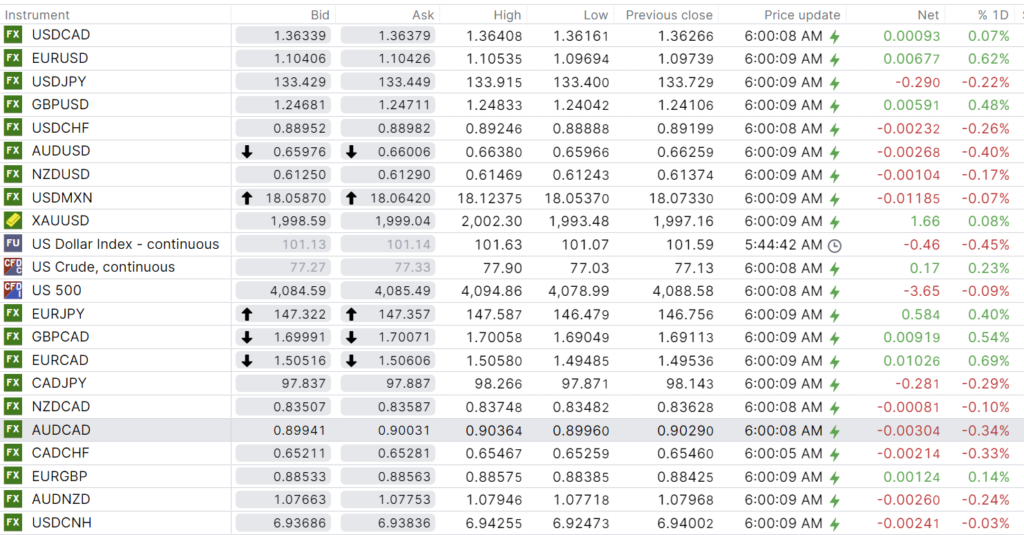

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

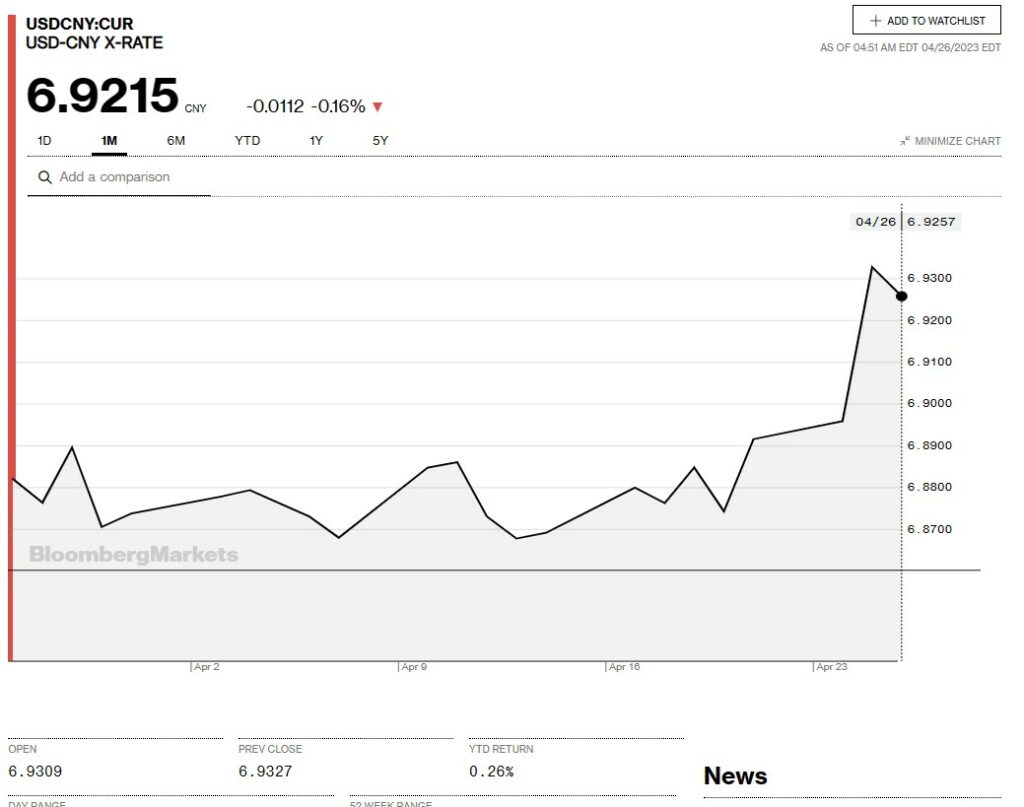

China Snapshot

Bank of China Fix: 6.9237, Previous: 6.8847

Shanghai Shenzhen CSI 300 fell 0.09% to 3959.23.

Chart: USDCNY 1 month

Source: Bloomberg