April 25, 2024

- US Q1 GDP rises 1.6% but PCE price index suggests inflation pressures.

- 10-year Treasury yield climbs to 4.704% after GDP, Equities sink.

- US dollar opens with losses but rallies post-GDP-JPY underperforms.

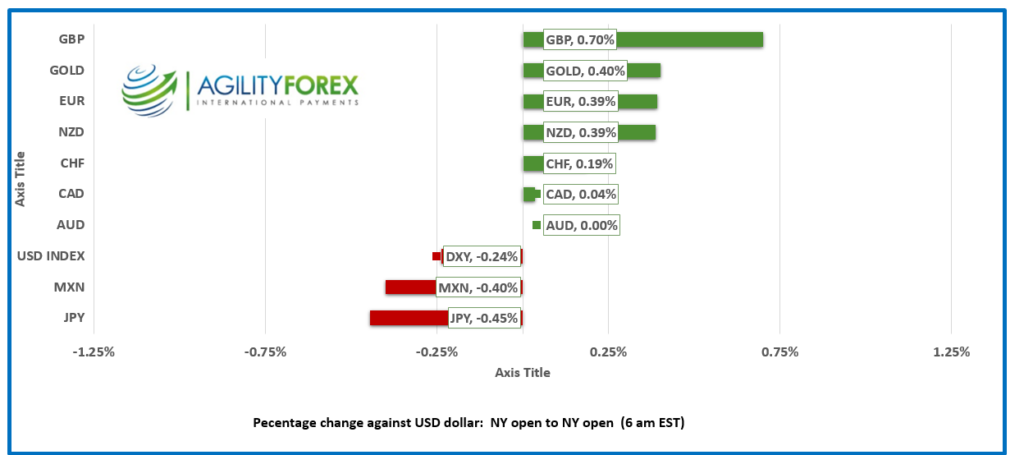

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3677, overnight range 1.3670-1.3708 close 1.3702.

USDCAD retraced some of yesterday’s gains in an uneventful overnight session, with the losses being driven by general US dollar weakness. That changed when today’s US Q1 GDP data showed a relatively strong economy but with burgeoning inflation pressures and prices jumped to the session peak.

The BoC’s Summary of Deliberations was as expected. The Council’s stance on interest rates is cautious, opting to monitor key inflationary indicators closely before adjusting the policy. Future rate adjustments, when deemed appropriate, are expected to be gradual, ensuring inflation targets are sustainably achieved without destabilizing economic recovery. That means that they will cut interest rates but at a measured pace.

WTI oil traded sideways in an 82.58-83.25 range. Support from the EIA’s report that crude inventories fell by 6.37 million barrels last week was offset by ongoing concerns about slowing Chinese growth, while Middle East tensions remain the wild card.

USDCAD Technicals

The intraday USDCAD technicals are bearish while below 1.3720, looking for a break below 1.3650 to extend losses to 1.3590. A move above 1.3720 shifts the focus to 1.3800.

Fibonacci analysis of the January-April range suggests that the break below 1.3690 puts 1.3590 (38.2% retracement) in play. Support from the uptrend line from January 3 is in the 1.3540-50 area.

For today, USDCAD support is at 1.3660 and 1.3620. Resistance is at 1.3720 and 1.3760. Today’s range is 1.3660-1.3740.

Chart: USDCAD daily

Source: DailyFX

“It’s the economy, stupid”

A strategist in Bill Clinton’s 1992 campaign coined the “It’s the economy, stupid” phrase to keep campaign workers focused on what he saw as the most pressing issue for voters. Fed officials are finding that the phrase is just as applicable today, which is one of the reasons US interest rates will remain unchanged until September at best.

And the US economy is just fine. US GDP growth slowed from 3.4% in Q4 2023 to 1.6% y/y in Q1 2024. The result was below the forecast but accelerating inflation is a sign stagflation could become an issue.

Data and Meta Sour Equity Mood

Meta (META: NASDAQ) stock nearly tripled in value in 2023 and the company earned 36.455 billion in Q1, beating estimates. Still, investors were not happy, and the stock dropped about 19% in after-hours trading. Investors (what have you done for me lately?) were not happy with Zuckerberg’s long-term AI plans. Japan’s Nikkei 225 index closed down 2.16%. European bourses are mixed. And little changed after the US data. The UK FTSE 100 index is up 0.74% while the French CAC 40 has lost 080%. S&P 500 futures are down 1.07 % while the US 10-year Treasury yield jumped from 4.642% to 4.706%, post GDP.

EURUSD

EURUSD rallied to 1.0730 from 1.0694 with prices getting a boost from improving Eurozone data. The better-than-expected German Ifo report on Wednesday and the improvement in Consumer Sentiment seen today (actual -24.2, previously -27.3) is underpinning prices. EURUSD retraced all its overnight gains, post-GDP.

GBPUSD

GBPUSD climbed from an Asian low of 1.2444 to 1.2523 in NY then dropped to 1.2476 after the US data. GBPUSD had been under pressure because of earlier comments by BoE officials that the inflation might be lower than previously expected. Those sellers got squeezed yesterday after BoE Chief Economist Hu Pill warned that cutting rates too early was worse than cutting them too late.

USDJPY

USDJPY traded in a 155.20-155.75 range overnight, comfortably above 155.00 which many analysts thought was a “Red Line” for the BoJ and Finance Ministry. Anticipated FX intervention failed to materialize while government and BoJ officials yammered on about “watching FX markets.” USDJPY gains are being fueled by JGB and Treasury yield differentials and until one rises or the other falls, 160.00 is a nice target.

AUDUSD and NZDUSD

AUDUSD drifted in a 0.6482-0.6539 range supported by firmer metals prices. Activity was subdued as Australian and New Zealand markets were closed for ANZAC day celebrations. NZDUSD traded in a 0.5928-05968 range at dropped to the low after the US data.

USDMXN

USDMXN consolidated yesterday’s gains in a 17.0331-17.1114 range. Yesterday’s bi-weekly inflation data showed Core-inflation rising 0.16% as expected and below the 0.32% increase previously. The results did not change the belief that Banxico will leave rates unchanged.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

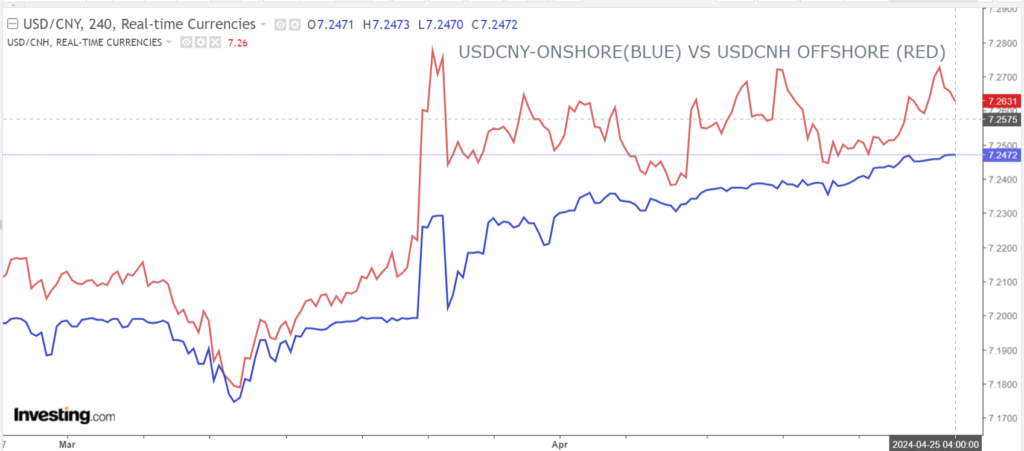

China Snapshot

PBoC fix: 7.1058 forecast 7.2442, (prev. 7.1048).

Shanghai Shenzhen CSI 300 rose 0.25% to 3530.28

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com