Image by DALL-E

November 30, 2023

- Fed fave-CORE PCE Price Index ticks down to 3.5% y/y from 3.7%.

- Canada September GDP tops expectations-barely.

- US dollar opens modestly stronger vs close but mixed from yesterday’s open.

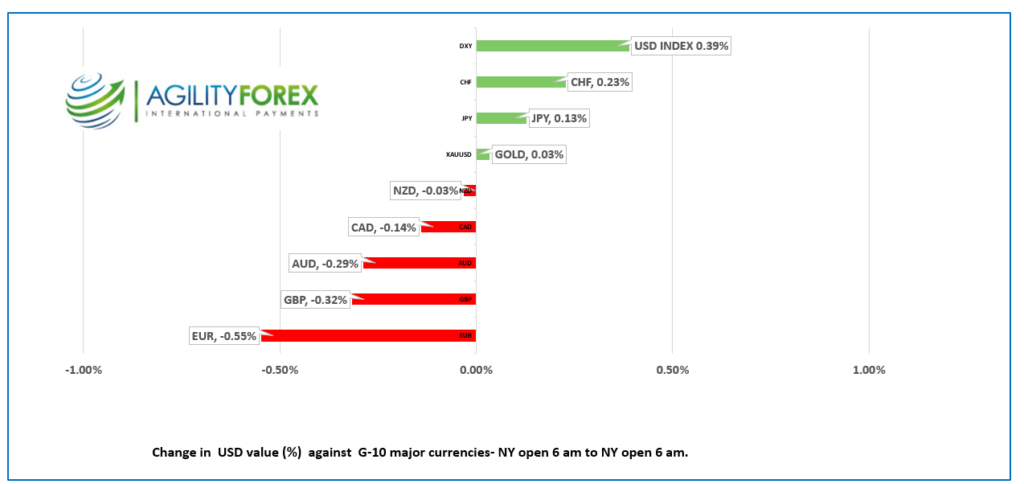

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3604-08, overnight range 1.3541-1.3622, close 1.3590

Canada’s economy grew in September, although the result is nothing to cheer about. September GDP rose 0.1% m/m compared to the forecast for 0% and a tick better than the August result. Real gross domestic product (GDP) declined 0.3% in the third quarter, following a 0.3% increase in the second quarter. The news was ignored, and attention shifted to the US data.

USDCAD is mildly bid due to speculation that the major central banks (other than the Bank of Japan) will be following or matching Fed policy moves when Jay Powell and friends begin to cut US rates. US economic growth is still expected to outperform compared to Canada which suggests limited USDCAD downside.

The UK Financial Times is reporting that Saudi Arabia may have convinced other cartel members to reduce Opec oil production. The meeting is still going on any anything can happen which explains why WTI spiked to $79.59/b on the news then promptly retreated to $78.97/b.

USDCAD Technicals:

The intraday USDCAD flipped to bullish with the rally above 1.3600. A move above 1.3630 targets 1.3680 and suggests that a short term low is in place at 1.3540. Failure to take out 1.3630, points to another test of the recent low.

The longer term view remains bullish after yesterday’s breech of the 1.3580 uptrend line was not sustained which keeps a retest of 1.3780 in play.

For today, USDCAD support at 1.3570 and 1.3540. Resistance is at 1.3630-1.3680. Today’s range 1.3570-1.3650.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

“Another one bites the dust.” November is soon to vanish into the rearview mirror of history under a cloud of “déjà vu.”

At this time last year, analysts were predicting that Fed rates would peak in the 4.5-4.75% area and the first rate cuts occurring at the start of Q3. Flash forward to today, and markets are pricing the first rate cut at the May 1, 2024, meeting. Eventually, they will be right.

Traders took to comments from noted Fed hawk, Christopher Waller like a pit bull on a postman. Mr. Waller said that if inflation continued to fall for “three, four, or five months, we could start lowering the policy rate just because inflation is lower.”

Cleveland Fed President and Fed voter Loretta Mester’s comments yesterday avoided mention of when rates would be trimmed but repeated that “monetary policy is in a good place.”

That “good place” may have experienced some “lease-hold” improvements following todays data. Fed Chair Jerome Powell’s favourite measure of inflation, the Core PCE price index dropped to 3.5% from 3.7%. In addition weekly jobless claims did not increase as expected and only rose by 7,000 from last week’s upwardly revised 211,000 result.

FX markets are seeing the usual chop due to month-end portfolio rebalancing.

EURUSD traded negatively in a 1.0909-1.0984 range and is near session lows in NY. Traders did not cheer news that Eurozone inflation fell to 2.4% in November, down from 2.9% in October. Even better, core CPI dropped to 3.6% from 4.2%. The news prompted chatter that ECB rates would be cut as soon as the summer, and that speculation drove the single currency lower. The EURUSD uptrend from November 1 is intact while prices are above 1.0900.

GBPUSD dipped in a 1.2631-1.2711 range due to a rebounding US dollar as traders assess the prospects for the Bank of England to begin easing. The currency continues to garner some support because BoE Governor Bailey has stuck to his view that rates need to remain at elevated levels to tame inflation. GBPUSD is bullish while prices are above 1.2430.

USDJPY got a boost from broad US dollar strength and rallied from 146.84 to 147.79. The rally got an assist from slightly higher US 10-year Treasury yield, which climbed to 4.292% from 4.256% where it closed on Wednesday. Japanese Retail Trade was weaker than expected at 4.2% y/y (forecast 5.9%) but the news was offset by higher than expected Industrial Production in October (actual 1.0% vs. September 0.5% y/y).

AUDUSD is at the bottom of its 0.6595-0.6651 range following the US data.

Chicago PMI forecast 45.4 vs previous 44) and October Pending Home Sales (forecast -2.0% vs 1.1% y/y in September) are due.

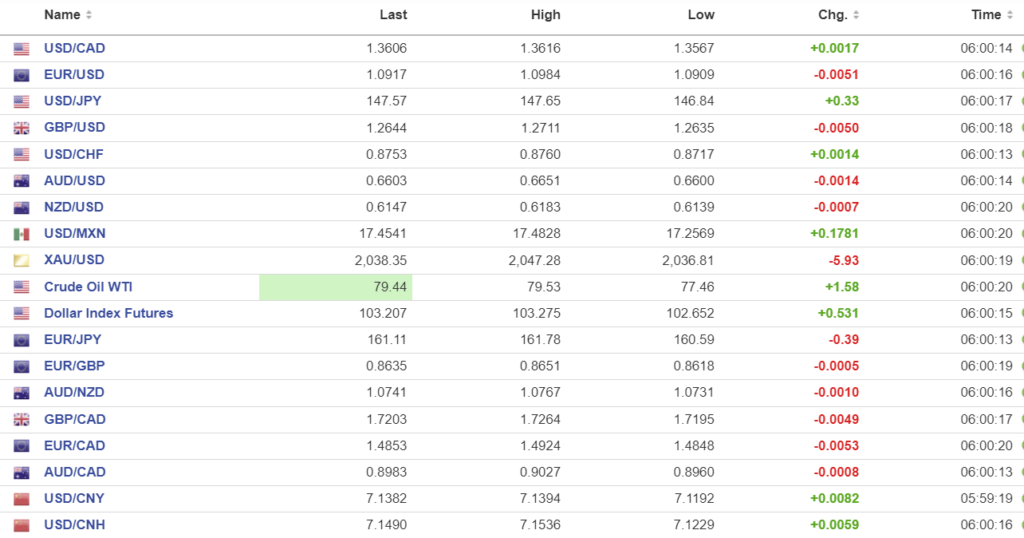

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

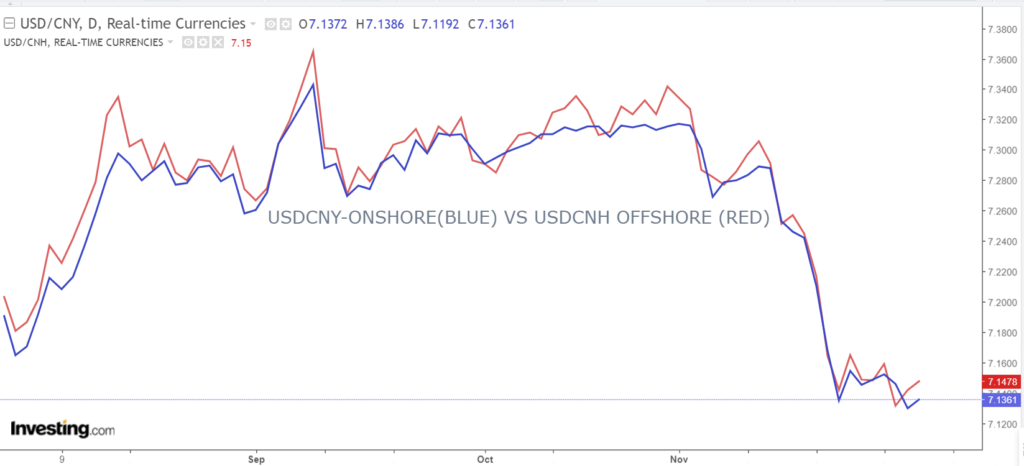

China Snapshot

PBoC fix: today 7.1018, expected 7.1273, previous 7.1031.

Shanghai Shenzhen CSI 300 rose 0.23% to 3496.20.

NBS Manufacturing PMI 49.4 (forecast 49.7, October 49.5)

November non manufacturing PMI 50.2 (forecast 51.1, October 50.6)

Traders were disappointed with the November PMI data which shows factory activity is slowing further and consumer spending looks to fall due to thee weaker than expected services PMI. On the bright side, analysts are hoping that the data will spur authorities to increase stimulous.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com