August 30, 2024

- Government spending boosts Canada GDP.

- Tame US Core PCE-Price index will not change market rate outlook

- US dollar opens with small gains-MXN is the biggest loser

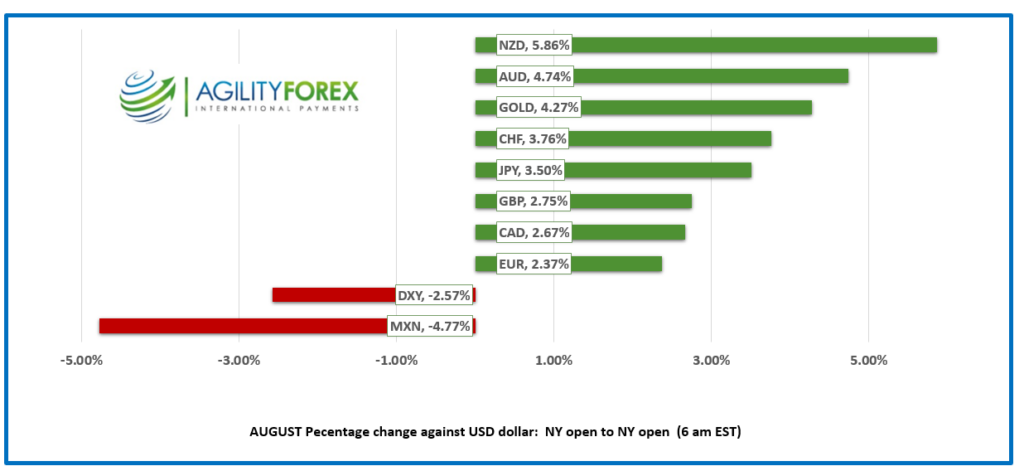

August FX at a Glance

Source: IFXA/RP

USDCAD open 1.3474, overnight range 1.3470-1.3491, previous close 1.3485

USDCAD has drifted higher since finding a bottom at 1.3440 on Tuesday, but it’s struggled to gain any real upward momentum. It didn’t change after the release of a disappointing GDP report.

The latest GDP report reveals modest growth, with a 0.5% increase in the second quarter, driven by higher government spending, hardly a harbinger of increased economic productivity. In addition, the economy faces challenges, including a decline in per capita GDP and ongoing weaknesses in exports and residential construction. The slowdown in household spending and reduced imports suggest softer domestic demand and the persistent decline in per capita GDP signals underlying issues.

WTI oil traded within a 75.66-76.58 range, with prices supported by supply concerns in Libya and reports that Iraq plans to reduce output. The reduction in Iranian output is primarily a gesture to appease OPEC after exceeding its quotas.

USDCAD downside may be limited today due to profit-taking ahead of the Canadian and US long weekends.

USDCAD technicals

The intraday USDCAD technicals are mildly bullish above 1.3450 and need a break above 1.3490 to extend gains to 1.3530. A topside failure shifts the focus to support in the 1.3440 area.

The daily chart shows USDCAD stuck in a 1.3440-1.3600 range and with a bearish bias. However, the RSI studies suggest USDCAD is very oversold which suggests support at 1.3440 will be tough to break. On the other hand, stretched short CAD/Long US dollar speculative positions should limit gains.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3490 and 1.3520. Today’s Range 1.3430-1.3510.

Chart: USDCAD daily

Source: DailyFX

Bailing on the Greenback

August wasn’t kind to US dollar bulls. The shift in the US interest rate outlook from slow and measured to deeper and faster propelled major G-10 currencies to impressive gains last month. Leading the charge, the New Zealand dollar rallied 5.89%, followed by a 4.74% rise in the Australian dollar. The Canadian dollar and Euro managed gains of 2.67% and 2.37%, respectively. The Mexican peso, however, bucked the trend, losing 4.77% due to a mix of rate cuts, carry trade unwinding, and domestic political concerns.

Past its Best-Before Date

The Bureau of Economic Analysis released the Fed’s favored Core PCE Price Index report today, which delivered a 0.2% m/m increase in July and 2.6% y/y rise, both unchanged from June. However, the significance of this data has greatly diminished. Once a headlining, stadium-packing rock star, it’s now just hoping to fill seats at a backwoods casino. The inflation beast has been tamed, and the Fed’s focus has shifted to the employment picture. The US 10-year Treasury yield rose to 3.889 from 3.852% on the news.

Global Equity Indexes Rally

Asian equity traders wrapped up August on a positive note, with all major indexes posting gains, including those in China. Japan’s Topix rose 0.73%, Australia’s ASX 200 gained 0.58%, and Hong Kong’s Hang Seng climbed 1.14%. In Europe, France’s CAC 40 is leading the charge with a 0.49% gain, while S&P 500 futures are up 0.31%.

EURUSD

EURUSD traded in a narrow 1.1069-1.1096 range overnight as a slew of Eurozone data muddied the waters. Eurozone Core CPI rose just 2.2% y/y, as expected, but well below June’s 2.6%. The decline, largely due to falling energy prices, keeps the door open for a potential 25 bps rate cut by the ECB in September. Meanwhile, the Eurozone unemployment rate ticked down to 6.4% from 6.5%.

GBPUSD

GBPUSD traded sideways in Asia, rising from 1.3160 to 1.3199 before drifting down to 1.3178 in New York. The currency found support from EURGBP selling, while weaker-than-expected August housing price data (actual -0.2% m/m vs. forecast 0.3%) had little impact.

USDJPY

USDJPY traded uneventfully within a 144.66-145.16 range. Tokyo’s August CPI rose 2.6% y/y, up from 2.2% in July, but any support from this was offset by higher-than-expected Japanese unemployment (2.7% vs. forecast and previous 2.5%) and a weaker-than-expected increase in July Retail Sales (2.6% y/y vs. forecast 2.9%).

AUDUSD and NZDUSD

AUDUSD traded sideways within a 0.6789-0.6817 range after July retail sales were flat (actual 0% vs. forecast 0.3%, June 0.5%). The Australian dollar, the second-best performing currency against the US dollar in August, rose 4.74% due to hawkish rhetoric from the RBA, contrasting with dovish comments from Fed Chair Powell and FOMC members. The currency found additional support overnight on rumors that China may allow consumers to refinance mortgages.

NZDUSD traded in a 0.6250-0.6274 range and is set to close out the month as the best-performing G-10 currency against the US dollar, with a 5.8% gain from the August 1 NY open to today. Prices are further buoyed by a 4-point rise in the ANZ Consumer Confidence Index to 92.2, suggesting the NZ economy is on the road to recovery. The currency pair is underpinned by broad US dollar weakness and growing expectations for a 50 bps Fed rate cut on September 18.

USDMXN

USDMXN drifted lower within a 19.7030-19.8765 range on mildly improved risk sentiment today, following yesterday’s US GDP data, which suggested that the risk of a US economic hard landing has faded.

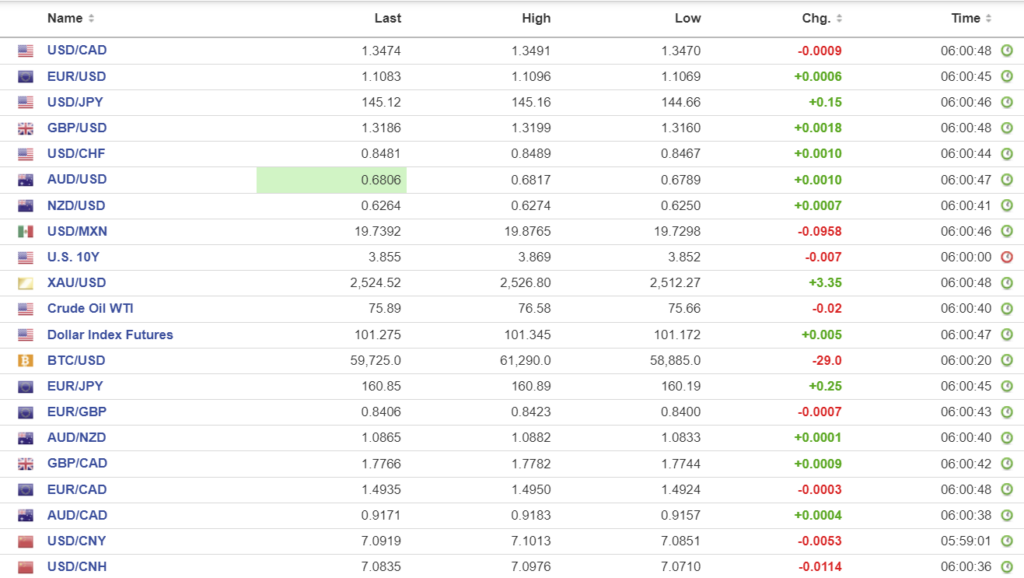

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1124 vs exp. 7.1116 (prev. 7.1299)

Shanghai Shenzhen CSI 300 rose 1.33% to 3321.43

Stocks rally on reports Chinese authorities are considering allowing refinancing on $5.4 trillion of mortgages. If done, it could spur economic growth as consumers would have more money to spend.

Chart: USDCNY and USDCNH

Source: Investing.com