By Michael O’Neill, Agility Forex, Senior Analyst

Jacob and Wilhelm Grimm were a couple of German brothers who among other achievements, popularized such famous fairy tales as “Cinderella,” Sleeping Beauty”, and “Snow White”.

They did not author “Building a Strong Middle Class-Budget 2017”. That was Bill Morneau. It may not have the staying power of a Brothers Grimm story, but Budget 2017 is a Liberal fairy tale nevertheless.

“Can you guess who will live happily ever after? Hint: not the tax-payer “ Source IFXA/Dept of Finance

A Global news story quoted an unnamed journalist, describing this budget as “wrapping up an empty box”. It is a poetic description especially since Prime Minister Justin Trudeau, the boss of Mr. Morneau, has been described as an empty suit.

The 2017/2018 budget deficit is forecast to widen out to $28.5 billion from the $25.4 billion projected in the fall. Prime Minister Trudeau is on record saying that “budgets balance themselves”. Mr. Morneau clearly did not get the message or perhaps he is using a defective algorithm since this budget is far from balanced.

Mr. Morneau announced a brand-new bureaucracy. He said this was a new agency to research and measure skills development. All the Canadian provinces call it the “Ministry of Education”.

The Liberals have a plan to strengthen and grow the middle class. Unfortunately, the growth will come from shrinking what used to be called the upper middle class.

The 2017 budget makes a “Case for Innovation”. The government says “To strengthen and grow the middle class, and remain competitive in the global economy, Canada must do more to encourage innovation. The future success of all Canadians relies on it. The Government understands those concerns, and that’s why its approach to innovation is centred on what Canadians need to succeed in an evolving economy”.

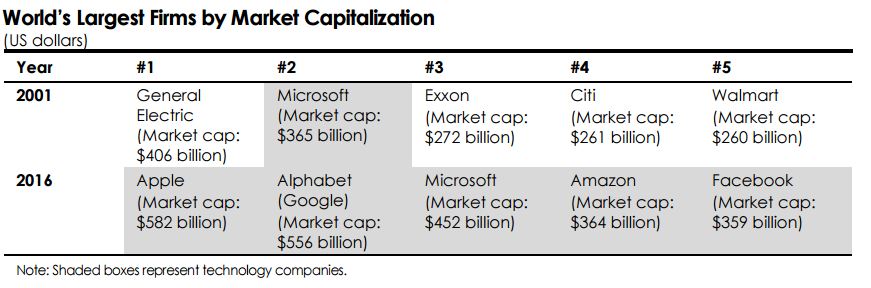

Mr. Morneau included the following chart in his budget document.

Source: Government of Canada Finance Department Budget 2017

Does that mean the Liberal plan for innovation is to buy American companies?

The Canadian dollar reacted to this budget by not reacting at all. There was no need. The Canadian government announcing a slightly higher deficit than what was previously forecast is the norm and therefore not a surprise. The string of projected deficits in 2018 and beyond is also, as expected.

That leaves the currency exposed to the Bank of Canada’s interest rate policy, the Federal Reserve’s interest rate policy, oil prices, and President Trump’s Nafta renegotiation plans.

Oil prices have collapsed over 14 percent since West Texas Intermediate (WTI) touched $54.90/barrel on February 23. They are back to just above the pre-Opec production cut announcement level of November 30. The Opec announcement led to a large number of oil contracts being bought on anticipation of price gains to $60.00/barrel. Oil prices rallied but the rally could not sustain gains above $55.00/barrel. The $60.00/barrel forecast proved to be a fairy tale

Bearish oil price factors which had been ignored during the rally started to weigh on prices. The number of new oil rigs rose weekly from the middle of February (which implies new production) while US crude inventories stayed at or near record levels. Traders were spooked when Saudi Arabia announced that February oil production climbed back above 10 million barrels/day.

On March 22, Goldman Sachs analysts warned of a material over-supply in the next three years. They believe that there is a new wave of supply coming down the pipe (literally) from oil projects that have been built over the past few years and are coming on stream. That production, combined with expected renewed Shale production, would add another one million barrels per day of crude to the market. Those factors and positioning led to the oil price collapse.

FX markets seem to think that the Federal Open Market Committee’s (FOMC) 2017 dot-plot forecast is just a fairy tale. And for good reason. The December 2015 dot-plot forecast four rate hikes in 2016 and the Fed could only manage one.

The problem is that 2017 is not even three months old and the Fed has already raised rates once. Fed Chair Janet Yellen said that the Committee wanted to avoid “waiting too long” to raise rates which could force them to “raise rates rapidly down the road, possibly disrupting financial markets”. There is plenty of time left for two or even three more rate increases this year. A hawkish Fed and a dovish Bank of Canada will keep the Canadian dollar on the defensive.

President Trump has promised to “tweak” the North American Free Trade Agreement (NAFTA). That is not a good thing for Canada or the Canadian dollar. There could be serious repercussions for softwood lumber exports, protectionist Canadian dairy policies and the auto industry. The Canadian dollar is likely to suffer when the Nafta talks get started.

As a rule, fairy tales have happy endings. For the Canadian dollar, the fairy tales of the self-balancing budget, $60.00/barrel WTI oil prices, and the 2017 dot-plot forecasts, could mean tears.

“I should never have sold USDCAD” Photo: Google Images