August 1, 2024

- Bank of England cuts rates by 25 bps to 5.0%.

- FX direction will track equity market sentiment.

- US dollar closes July on a mixed note- CAD finishes nearly unchanged.

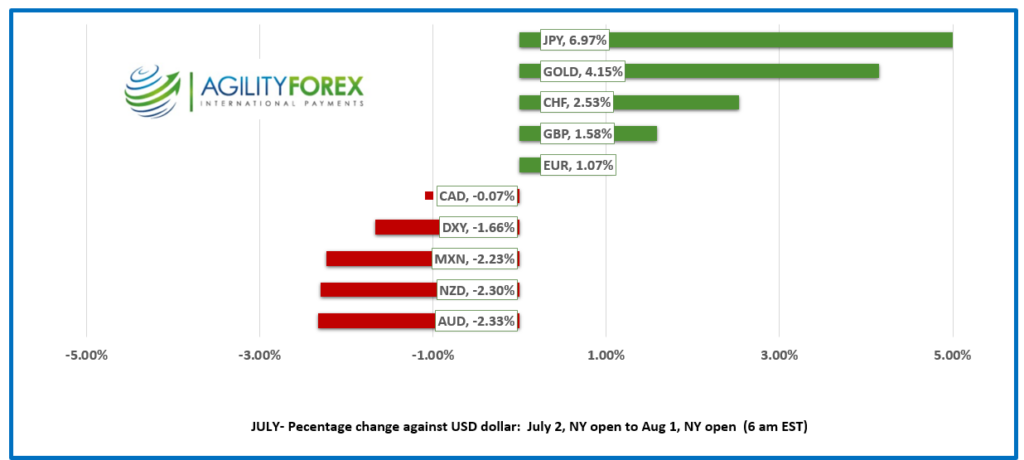

July FX at a Glance

Source: IFXA/RP

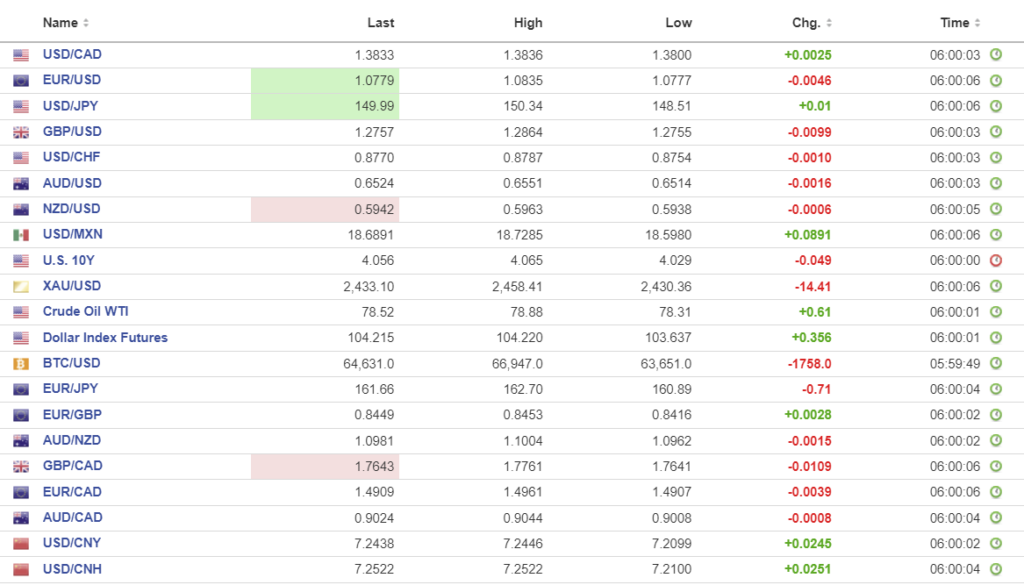

USDCAD open 1.3833, overnight range 1.3800-1.3836, previous close 1.3808

USDCAD dropped to a low of 1.3787 following the FOMC decision, mainly because the US dollar was under pressure across the G-10 spectrum. The move was short-lived, and USDCAD rallied to 1.3836 overnight. The currency finished July almost where it started.

Canada’s economy grew more than expected in May, rising 0.2% m/m compared to the forecast of 0.1%. The results look good, but the reality is the economy is still a basket case. Encouraging massive immigration without any semblance of a plan to deal with the influx is a major part of the problem. Additionally, Canada is spending gobs of money on developing a renewable energy industry while ignoring the existing wealth from proven fossil fuel reserves.

US weekly jobless claims rose by 14,000 to 249,000 last week which is further evidence that the US labour market is normalizing. It remains to be seen if todays ISM Manufacturing PMI (forecast 48.8) suggests the elusive “soft-landing” may be a reality. There is no Canadian data.

USDCAD Technicals

The intraday USDCAD technical bullish above 1.3810, looking for another test of resistance in the 1.3860 area. A breach of support at 1.3810 points to further losses to 1.3760.

The USDCAD uptrend line from the beginning of the year is intact above the 1.3610-20 zone and it is being guarded by support at 1.3750. Meanwhile the overbought USDCAD RSI is slowly dissipating which suggests the week-long 1.3750-1.3860 consolidation will continue.

For today, USDCAD support is at 1.3810 and 1.3770. Resistance is at 1.3860 and 1.3890. Today’s Range 1.3770-1.3860.

Chart: USDCAD daily

Source: DailyFX

Waiting, Waiting and More Waiting.

Fed Chair Jerome Powell had a Julius Caesar moment when he strode to the podium for his July 31 press conference. He peered above the top of his glasses and proclaimed, “I analyzed, I assessed, and I await.” That sums up the FOMC meeting outcome succinctly.

The Fed left its benchmark rate unchanged at 5.50%. He is waiting for September, although he didn’t say that explicitly, the statement certainly points to such a move. The FOMC statement read, “Recent indicators suggest that economic activity has continued to expand at a solid pace,” which is exactly what it said on June 12. This suggests an economic soft landing is likely.

The statement continued, saying, “Job gains have moderated.” That’s a definite downgrade from June when job gains “remained strong.” This shift implies that the labor market, while still healthy, is beginning to cool.

Lastly, the statement downgraded its inflation view from “inflation is elevated,” to “somewhat elevated” while noting there has been some “further progress” instead of modest progress. All of the above suggests that the Fed should have acted and cut rates by 25 bps to 5.0%, but alas, they were handcuffed by FOBW (Fear of Being Wrong).

Action Speaks Louder Than Words

Financial markets have blinders on. They only have eyes for interest rates and ignore all the rest. In particular, the percolating tensions in the Middle East. Iran vows to avenge the death of a Hamas leader who was blown to pieces by an Israeli missile while he visited Iran. The “mad mullahs of Tehran” are severely miffed and embarrassed to discover that sponsoring terrorist groups all over the region had consequences. They want to punish Israel in a demonstration of Iranian military might but are handcuffed because Israel has a massive nuclear arsenal, and they don’t. Nevertheless, common sense is not all that common in the Consultative Assembly in Tehran, and a military response could have implications for global markets, especially if the action severely disrupts oil production and shipping in the region. That would be inflationary, and all the central banks cutting rates will be forced to start hiking.

Bond Traders Know Best

The Fed may have left rates unchanged and attempted to suggest that rate cuts were not a done deal with the statement repeating, “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” Bond traders didn’t believe it. The 10-year Treasury yield plunged from 4.133% to 4.028% before settling at 4.05% overnight. The yield is a far cry from the 4.49% at the start of July.

EURUSD

EURUSD is trading negatively in a 1.0777-1.0835 range. The single currency is suffering from a mix of soft domestic economic data yesterday, weak China PMI overnight, and rate cut sentiment that suggests the ECB will cut deeper than the Fed. The intraday technicals are bearish below 1.0840 with the decisive break below 1.0800 targeting 1.0750, then 1.0710.

GBPUSD

GBPUSD plunged from 1.2864 to 1.2754 after the Bank of England surprised about half of the market and cut rates by 25 bps to 5.0%. The vote was close, 5 for and 4 against. GBPUSD has since recovered to 1.2811, supported by Governor Bailey suggesting rates “may not be cut too quickly or too much.”

USDJPY

USDJPY has been all over the map inside a 148.51-150.34 trading range as it tried to consolidate losses in the wake of the plunge from 153.89 yesterday. The JPY/G-10 carry trade is getting hammered as traders unwind short JPY trades due to expectations for higher Japanese and lower Fed interest rates. USDJPY fell nearly 7.0% in July, and it could do the same in August if support at 148.50 is broken.

AUDUSD and NZDUSD

AUDUSD recouped its post-FOMC losses and traded in a 0.6514-0.6551 range. Prices will struggle to overcome resistance in the 0.6560 area. The Australian dollar was the worst performing G-10 currency in July due to RBA rate cut concerns and the sluggish economic growth outlook for China, which was reinforced with the latest Chinese PMI data.

NZDUSD is steady in a 0.5938-0.5963 range, and it nearly tied the AUDUSD for the title of worst performing currency in July. Chinese economic growth issues are a key reason.

USDMXN

USDMXN peaked at 18.9445 yesterday and dropped to 18.5203 post-FOMC on the heels of the decline in the US 10-year Treasury yield.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1323 vs exp. 7.2167 (prev. 7.1346).

Shanghai Shenzhen CSI 300 fell 0.66% to 3419.27.

Caixin Manufacturing PMI shrank to 49.8 (contraction territory) from 51.8 in June which analysts suggest is a sign that exports may be cooling. Its another failing grade for Emperor Xi, who could react by banning the release of such data. China is back to hiding data that shows the weakness of the economy as it also shows the true incompetence of the ruling cadre. It used to be that Chinese data should be taken with a grain of salt. Today you need the entire salt shaker.

Chart: USDCNY and USDCNH

Source: Investing.com