Image by DALL-E,

December 11, 2023

- China CPI and PPI evidence of weak demand.

- Traders awaiting US inflation data due Tuesday.

- US dollar opens firm, consolidating Friday’s NFP gains.

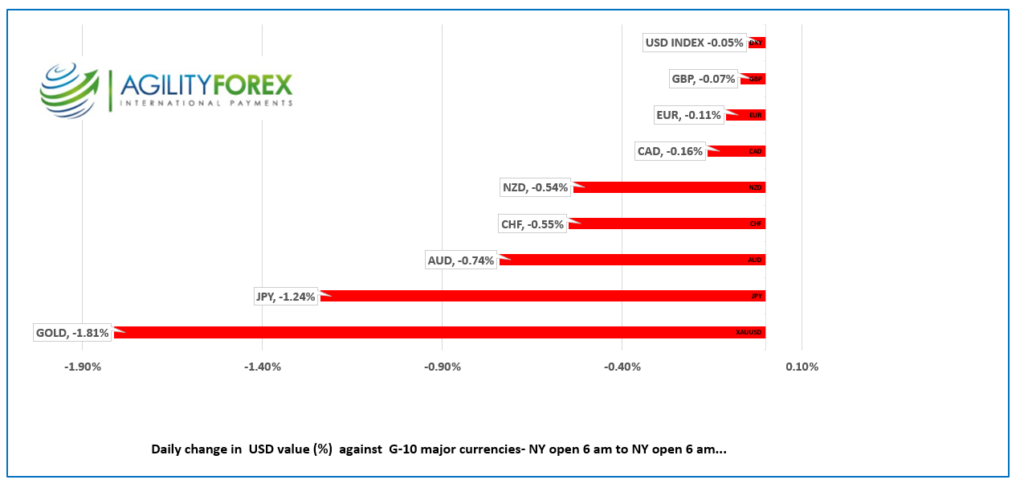

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3594-98, overnight range 1.3570-1.3605, close 1.3584

USDCAD is stuck in a well-traveled range and is unlikely to see much movement today due to a complete lack of economic data. That will change starting Tuesday with the release of the US November inflation report which wis followed by the FOMC meeting on Wednesday.

The Fed is likely to warn that inflation has not been tamed and rates need to remain in restrictive territory. However, traders won’t care too much because most believe that rates will be cut and whether its March, May or June, its no big deal.

WTI oil prices continue to be sluggish and trading in the $70.00-$72.00/barrel range. Weaker than expected Chinese CPI and PPI data is seen as further evidence of soft Chinese demand weighed on prices.

USDCAD Technicals:

The intraday USDCAD technicals are unchanged. They are bearish below 1.3610 looking for a break below support in the 1.3510-40 zone to extend losses to 1.3460. A topside break above resistance in the 1.3630-1.3660 zone would suggest further gains to 1.3780.

Longer term, the USDCAD uptrend channel from July is guiding prices higher while above 1.3470.

For today, USDCAD support at 1.3550 and 1.3510. Resistance is at 1.3630 and 1.3660. Today’s range 1.3550-1.3630

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

It was a reasonably silent night in financial markets, but not so much in the conflict zones across the globe.

Friday’s US nonfarm payrolls data injected an element of caution into the enthusiasm for Fed rate cuts beginning in March 2024. Payrolls grew by 199,000, beating the consensus forecast of 180,000, while the unemployment rate ticked down to 3.7% from 3.9% in October.

The news lifted the US 10-year Treasury yield from 4.128% in Asia Friday morning to 4.245% at Friday’s close. The US dollar caught a bit of a bid, while expectations for a March 20 rate cut flipped from 60% to 42.07%. Markets will be jittery until tomorrow’s US CPI report and Wednesday’s FOMC meeting.

Asian equity markets closed in positive territory except for the Hong Kong Hang Seng index, which fell 0.81%. Japan’s Nikkei 225 index gained 1.50% on the heels of a weaker yen, while Australia’s ASX hovered around flat. European bourses are negative, except for the French CAC 40 index, which is flat. The UK FTSE 100 index fell 0.67%, and S&P 500 futures are down 0.13%.

EURUSD treaded water in a 1.0751-1.0779 range, with traders content to be sidelined until ahead of US CPI Tuesday, FOMC Wednesday, and the ECB meeting Thursday. Policymakers are sure to push back on hopes for a rate cut in March.

GBPUSD traded with a modest bid, rising from 1.2532 to 1.2580 in early NY. The UK employment report is due Tuesday, followed by Trade, GDP, Industrial Production, and Manufacturing Production on Wednesday, with the BoE meeting on Thursday.

USDJPY rebounded from an overnight session low of 144.81 to 146.46 after a Bloomberg article suggested that the BoJ would leave monetary policy unchanged in December.

AUDUSD drifted in a 0.6551-0.6583 range, with price action tracking US dollar sentiment.

The US economic calendar is empty today.

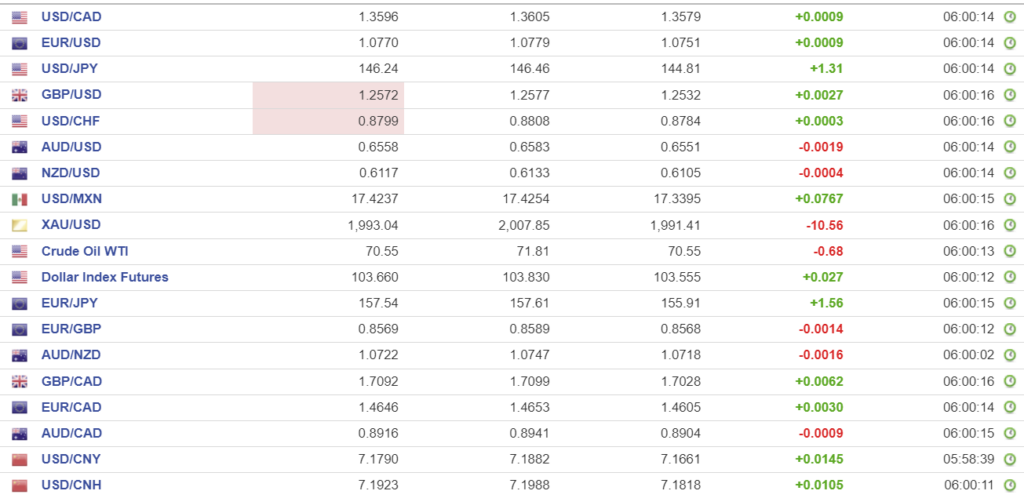

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1163, expected 7.1690, previous 7.1123

Shanghai Shenzhen CSI 300 rose 0.59% to 3419.45.

China November CPI -0.5% y/y vs -0.2% previously.

China November Producer Price Index -3% y/y vs -2.6% in October.

Chinese authorities were rumoured to be buying ETF’s of state-owned companies in a not so subtle effort to lift the CSI 300 index.

The weaker than expected CPI and PPI data indicates a lack of domestic demand from Chinese consumers.

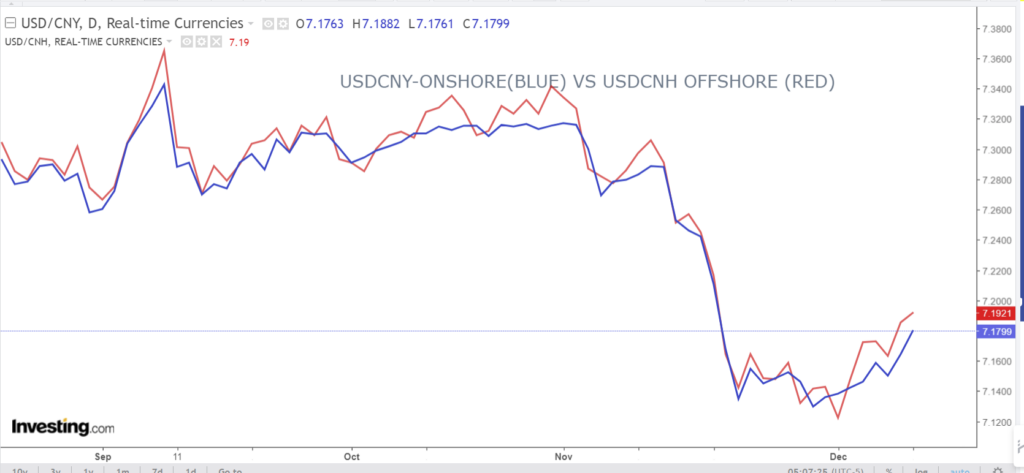

Chart: USDCNY and USDCNH

Source: Investing.com