Source: HDClipartall.com

- Retail Sales 0.% in September (forecast 0.2%, August 0.4%)

- UK PM fires the Chancellor

- US dollar opens little changed from Thursday, Gold and GBP are the exceptions

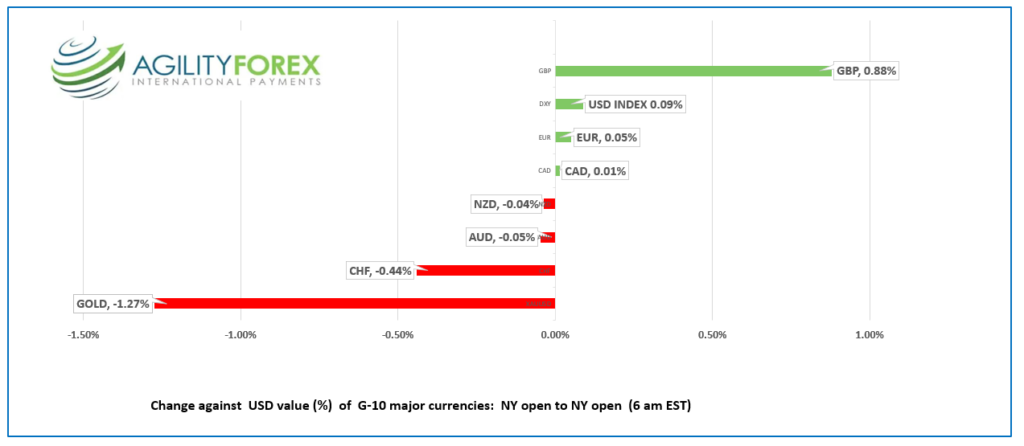

FX at a glance:

Source: IFXA Ltd/RP

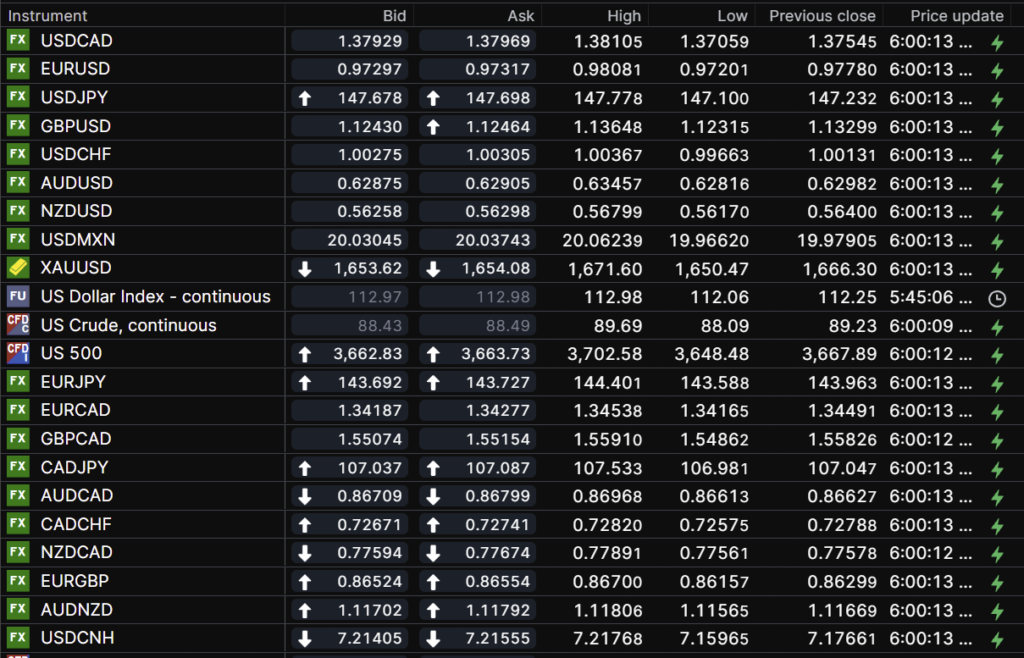

USDCAD Snapshot: open 1.3793-97, overnight range 1.3706-1.3825, close 1.3755

USDCAD had a wild ride yesterday, rising from 1.3775 prior to the US inflation report to 1.3976 in the immediate aftermath. Prices dropped sharply in tandem with the rebounding S&P 500 index and dropped to 1.3709 before climbing back to 1.3755 at the close.

Domestic issues did not have anything to do with the price volatility, and still don’t.

USDCAD ticked up to 1.3825 ahead of the Retail Sales data then retreated to its opening level

WTI oil prices are stuck in a $85.00-$95.00/b range. Prices are underpinned by Opec production cuts while fears of a global economic slowdown cap gains. A key reason that WTI prices are having a reduced impact on USDCAD trading is that Canada’s key oil export, Western Canada Select (WCS) is trading at a hefty discount to WTI Yesterday WTI closed at $89.23/b while WCS finished at $66.02.

Canada Manufacturing Sales fell 2.0% m/m in August (July -0.6%) while Wholesale Sales rose 1.4% m/m (-0.6% in July).

USDCAD Technical outlook

The intraday technicals are bullish are bullish above 1.3690, looking for a break above 1.3860 to extend gains to 1.4000. A drop below 1.3690 targets 1.3560 then 1.3500

For today, USDCAD support is at 1.3730 and 1.3690. Resistance is at 1.3830 and 1.3890. Today’s range: 1.3730-1.3830

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

If you just glanced at the graph showing the change in the value of the US dollar against the G-10 majors comparing Thursday’s NY open to today’s opening level, it is easy to conclude that not much happened yesterday. Boy, would you be wrong!

Traders were slapped silly yesterday and the handprints are still visible on their cheeks today.

Bonds, equities, and the US dollar whip-sawed in extremely volatile and wide-ranging markets after September CPI was a touch firmer than expected. Fortunes were made, lost, and remade in the span of a few hours in one of the wildest days since the Financial Crisis.

The S&P500 opened at 3520.37, then dropped to 3491.58 following the CPI data, then soared 3685.41. Bonds were just as erratic. The US 10-year Treasury yield ripped higher from 3.89% to 4.03% then dropped to 3.897% in NY today. The US dollar index (USDX) jumped from 112.57 to 113.84 before plunging to 112.05 just after lunch.

There wasn’t a specific catalyst for the turmoil leaving plenty of room for speculation. One theory was a massive, short squeeze in stocks which were positioned for further equity market weakness. Another theory pointed to Europe where an ECB staff model suggested the ECB terminal rate was 2.25%, not the 3.0% that is priced in. Another guess suggested the Fed would need to slow the pace of rate hikes to prevent trashing other G-10 economies. So now ya know. 😊

The market turmoil occurred against a backdrop of missiles, suicide drones, and oil market discord. Russia stepped up drone attacks on civilians, while North Korea is firing missiles and sending fighter jets near the South Korea border. Meanwhile Washington cancelled an October 17 meeting with Saudi Arabia to show displeasure at the latest Opec production cuts. Not to worry, though, it’s the Fed’s interest rate outlook that is important.

Asia equity indexes closed sharply higher. Australia’s ASX 200 rose 1.75%, while Japan’s Nikkei 225 index jumped 3.25%. European bourses opened in positive territory and then extended gains with the French CAC index rising 1.51%. S&P 500 futures are a tad less enthusiastic and only 0.26% higher. Meanwhile, gold and WTI oil prices are lower.

US Retail Sales were as expected which helped S&P 500 futures regain its footing

EURUSD bounced in a 0.9720-0.09808 range overnight and sits at 0.9747 in NY. Many ECB officials comments have led to speculation ECB rates will rise 75 bps on October 27. Nevertheless, traders are leery after an ECB staff modeling forecast predicted the terminal rate was just 2.25%.

GBPUSD rallied from 1.1067 to 1.1379 yesterday, then chopped about in a 1.1232-1.1365 range overnight. Prime Minister Liz Truss fired Chancellor of the Exchequer Kwasi Kwarteng this morning which some pundits described as a “Kami-Kwasi” move. The turfing of Kwasi was due to the market reaction to the mini-budget and a deliberate move by Truss to save her job.

USDJPY is at the top of the 146.55-147.87 band since Thursday. BOJ intervention has not been reported.

AUDUSD and NZDUSD direction is at the whim of broad US dollar sentiment. Both currencies are well-above yesterday’s lows.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

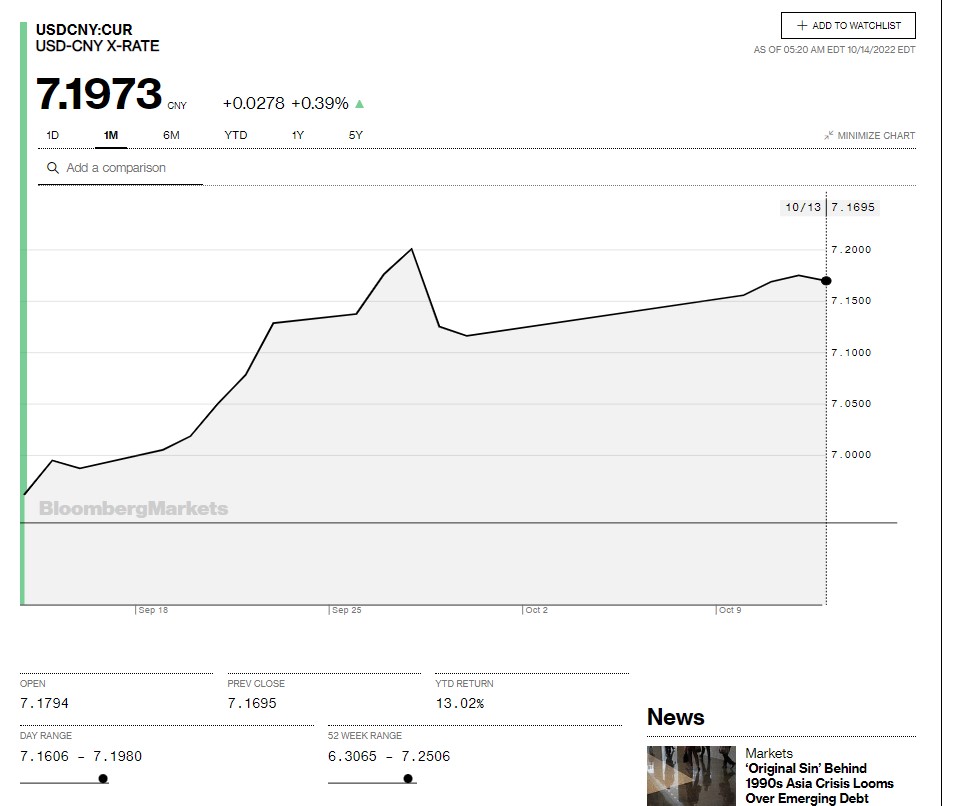

China Snapshot

Today’s Bank of China Fix: 7.1088, previous 7.1101

Shanghai Shenzhen CSI 300 rose 2.39% to 3842.47

September CPI 0.3% m/m (forecast 0.4%, August -0.1% m/m)

September PPI 0.9% y/y (forecast 1.0%, August 2.3% y./y)

Chart: USDCNY 1 month

Source: Saxo Bank