Source: HDClipart.com

- UK Conservative’s say “ In Liz we Truss”

- Oil retreats despite Opec cutting production, reversing previous increase

- US dollar stays mixed, AUD soft despite RBA 50 bp hike

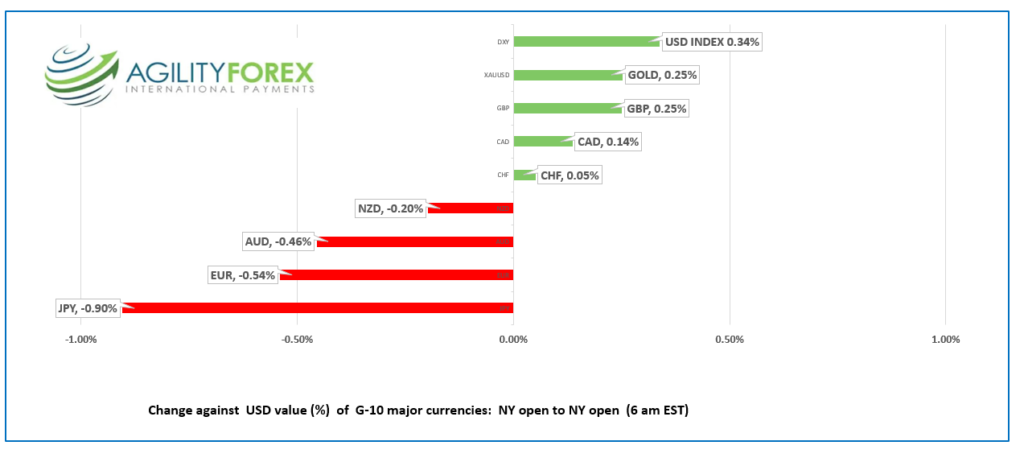

FX at a glance:

Source: IFXA Ltd/RP

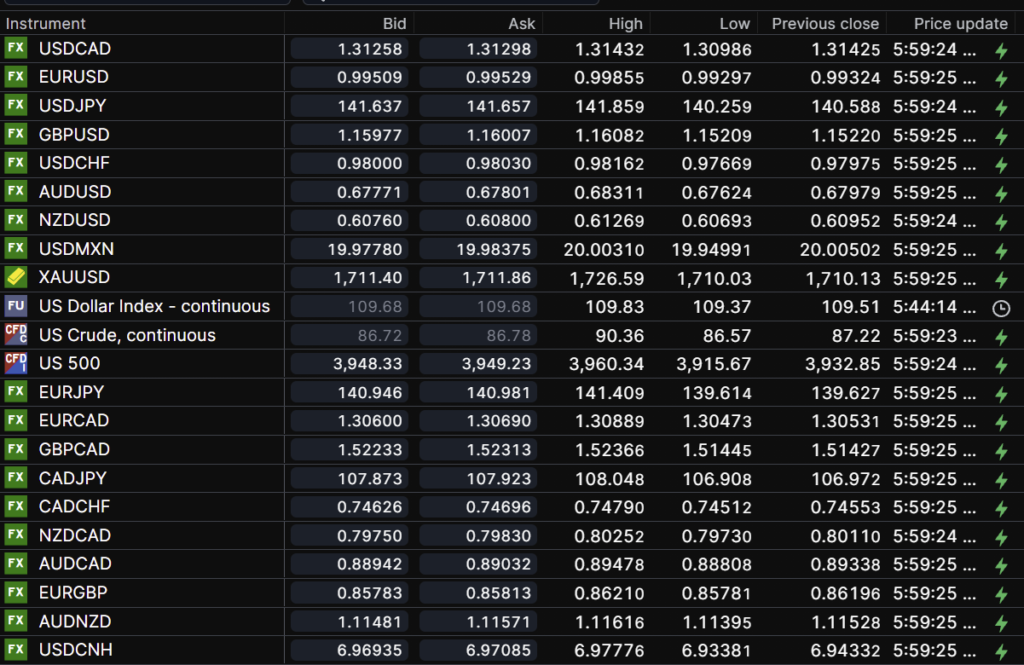

USDCAD Snapshot: open 1.3126-30, overnight range 1.3099-1.3143, close 1.3143

USDCAD was an after-thought for FX traders. The currency pair traded erratically in a 1.3075-1.3175 range since Friday morning.

USDCAD remains underpinned following a rash of Fed-speak suggesting sharply higher US interest rates which will remain at elevated levels throughout 2023. That view is a sharp contrast to the early-August sentiment of a Fed-pivot and a rate cut in January 2023.

However, the hawkish US rate outlook ignores the fact that the Bank of Canada is just as, or even more hawkish than the Fed. The consensus is the BoC will raise rates 75 bps tomorrow, but a 100 bp is a strong possibility. If so, USDCAD should test support in the 1.3000 area. However, further losses are not likely as USDCAD tends to rally into Q4.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.3100, looking for a move above 1.3180 to extend gains to 1.3225. A break below 1.3100 targets 1.3060, then 1.3000. The uptrend on the daily chart is intact above 1.3030.

For today, USDCAD support is at 1.3090 and 1.3060. Resistance is at 1.3160 and 1.3190. Today’s range: 1.3090-1.3160

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

There were plenty of doom and gloom headlines on the weekend, but traders were not impressed. The fall-out from Russia shutting down its Nord Stream 1 pipeline was limited to “been there, done that.” Russia cannot do any more energy damage to the EU, and governments have taken steps to mitigate the impact.

Opec, particularly Saudi Arabia, thumbed their noses at the US and announced they were cutting production by 100,000 b/day, effective October 1, reversing the 100,000/b increase that began September 1. They say it’s because they fear a global growth slowdown will lead to excess supply.

Global stock markets were relatively tame on Monday due to the US Labor Day holiday. Tuesday, Asian equity indexes were modestly lower, except for China’s Shenzhen Shanghai CSI 300 index, which gained 0.92%.

European bourses are grinding higher, led by a 1.12% rise in the German Dax index. DJIA and S&P 500 futures are trading higher, suggesting a positive open on Wall Street. Gold prices are steady, and oil prices are lower.

The US 10-year Treasury yield consolidated last week’s gains in a 3.208-3.279% range, which helped limit US dollar losses vs the majors.

EURUSD plunged from 1.0030 on Friday around noon to 0.9880 yesterday just as Europe opened due to Russia turning off the Nord Stream 1 taps. Europeans shrugged off the news due to “Russia fatigue” and anticipation of EU support to mitigate the impact of soaring prices. EURUSD climbed steadily and traded in a 0.9927-0.9986 range overnight.

Traders ignored weaker than expected Euro area composite and services PMI data and soft Eurozone retail Sales for July, preferring to await the ECB monetary policy meeting on Thursday.

GBPUSD rallied from 1.1444 in Asia Monday to 1.1608 just before NY opened today. The gains were partly due to “short-covering” after Liz Truss was announced as the latest UK Prime Minister, which allows the government to refocus on the economy rather than themselves. The Bank of England monetary policy meeting isn’t until September 15.

USDJPY roared higher, rising from Monday’s 139.85 low to 141.86 today. Traders are attempting to find the level which forces the BoJ to scrap its 0.25% yield curve cap.

AUDUSD traded in a 0.6762-0.6831, with the peak occurring before the RBA monetary policy decision and the bottom in the aftermath. The RBA hiked rates by 50 bps to 2.25%, which is considered to be the “neutral rate.” The statement was on the dovish side as the line about normalizing policy was ditched in favor of blather about helping bring inflation to target. Tomorrow, Q2 GDP is expected to rise to 3.5% y/y from 3.3% previously.US ISM Services PMI is expected at 55.1 for August compared to 56.7 in July.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

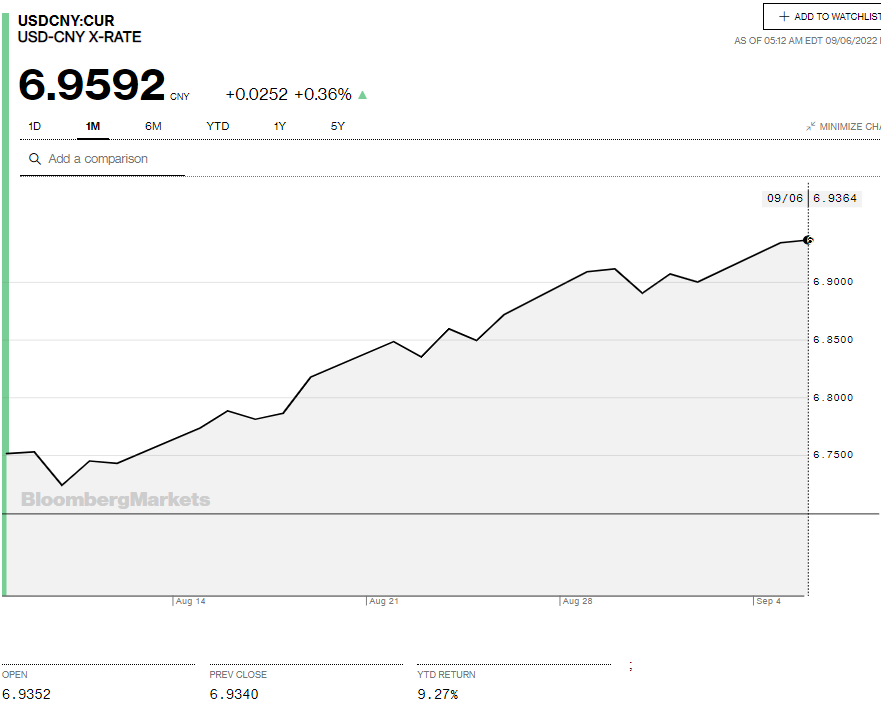

China Snapshot

Today’s Bank of China Fix: Sept 6, 6.9096, Sept 5, 6.8998 Sept 2, 6.8917

Shanghai Shenzhen CSI 300 rose 0.92% to 4,052.26

Caixin Services PMI was 55 in August compared to 55.5 in July

Bloomberg reports PboC to cut RRR by 200 bps on September 16 as well as Reserve Requirement Ratio for FX from 8.0% to 6.0%.

Chart: USDCNY 1 month

Source: Bloomberg