March 1, 2024

- US ISM Manufacturing PMI expected at 49.5.

- Eurozone HICP ensures ECB will leave rates unchanged next week.

- US dollar opens on a mixed note-

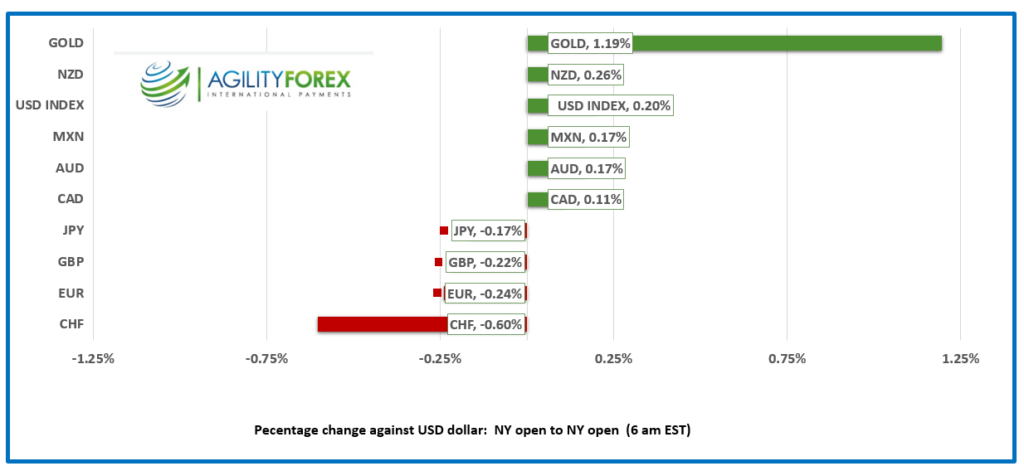

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3575-79, overnight range 1.3561-1.3592, close 1.3579

USDCAD is trading with a bit of a bid after recent US data reinforced the idea that the Fed is content to leave US interest rates at current levels for longer than previously expected. The currency is not getting any support from domestic data, as Thursday’s GDP report highlighted the weak economic performance compared to that of the US.

The CAD/US 10-year interest rate differential widened in favor of the US, which is also underpinning USDCAD.

However, oil prices may be helping to slow USDCAD gains. WTI is trading at $79.56/b today, a 4.9% gain since Monday. The gains are due in part because hundreds of oil tankers are avoiding the Red Sea due to Houthi missile and drone attacks, which is having an impact on physical markets. However, today’s China PMI data, which indicated its economy was still struggling, may limit WTI gains

USDCAD Technicals

The USDCAD technicals are bullish above 1.3550, looking for a break above the 1.3610 area to extend gains to resistance in the 1.3640-60 zone. A break above 1.3680 targets 1.3895 while a move below 1.3540 suggests renewed 1.3400-1.3600 range trading.

Longer term, USDCAD is trapped in a 1.3280-1.3660 range with the uptrend line from April 2022 coming into play in the 1.3280-1.3300 zone and resistance at 1.3660 capping the topside.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3620 and 1.3650. Today’s range is 1.3540-1.3640

Chart: USDCAD weekly

Source: Daily FX

G-10 FX recap

Yesterday’s highly anticipated PCE report proved inconclusive, and markets have reacted accordingly. Analysts and Fed officials have a slew of inflation metrics to choose from, including PCE, PCE core, PCE super core, CPI, CPI core, and the inflation components from ISM, GDP, and employment reports, to name just a few, which means there is a data point to validate any interest rate view. None of them paint a conclusive picture of the inflation trajectory, which suggests the Fed will be happy to leave rates unchanged for longer. This week, a slew of Fed officials were advocating patience.

The steady-for-longer view will be reinforced if today’s US ISM Manufacturing PMI pops into expansion territory with a move above 50.0. The forecast is 49.5.

Asian equity indexes closed with gains, and European bourses are in positive territory. SP500 futures are flat, and the US 10-year Treasury yield is 4.221%.

EURUSD chopped about in a 1.0798-1.0823 range. February preliminary HICP was a tad hotter than expected, rising 2.6% y/y (forecast 2.5%) but lower than the 2.8% seen in January. Core inflation fell to 3.1% from 3.3%. Analysts suggest the dips were just due to base effects and mean the ECB will have no interest in cutting rates at next week’s monetary policy meeting.

GBPUSD traded defensively in a 1.2617-1.2642 band with prices weighed down by weak February PMI data (actual 47.5, previous 46.1), which, although higher than in January, means the economy is still contracting. That result overshadowed the 1.2% y/y increase in the Nationwide Housing Price index.

USDJPY erased yesterday’s losses and rallied from Thursday’s close of 149.98 to 150.70 after BoJ Governor Kazuo Ueda contradicted yesterday’s comments by Board member Hajime Takata. Mr. Takata suggested that the inflation target was coming into sight. Mr. Ueda said, “I don’t think we are there yet.”

AUDUSD drifted in a 0.6490-0.6514 range with traders looking ahead to today’s US ISM Manufacturing PMI while largely ignoring the latest Chinese PMI data.

USDMXN is trading in a 17.0358-17.0695 range with prices tracking broad US dollar sentiment. Traders were unconcerned after Banxico downgraded 2024 GDP growth to 2.8% from 3.0% previously and expect Banxico’s first rate cut this month (March 21).

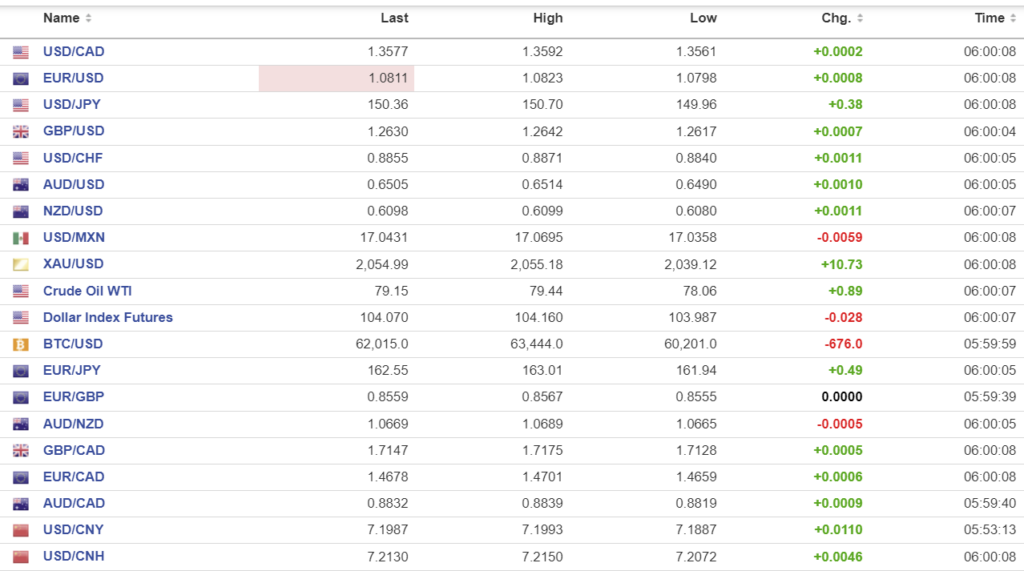

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1059, expected 7.2011, previous 7.1036.

Shanghai Shenzhen CSI 300 rose 0.62% to 3537.80.

NBS February Manufacturing PMI 49.1 (forecast 49.1, January 49.2)

Non-Manufacturing PMI 51.4 (forecast 50.8, January 50.7)

Caixin Manufacturing PMI 50.9 (forecast 50.6, previous 50.8)

The Peoples National Congress begins Tuesday, so it is no surprise that mainland stock markets rallied despite official Manufacturing PMI data shrinking for the 5th month in a row. The recent tightened regulations for quant short-selling equity strategies is also providing artificial support for stocks.

Chart: USDCNY and USDCNH daily

Source: Bloomberg