June 12, 2024

- US May inflation cools, slightly.

- FOMC dot-plot forecasts are key to US dollar direction.

- US dollar eases in cautious overnight trading.

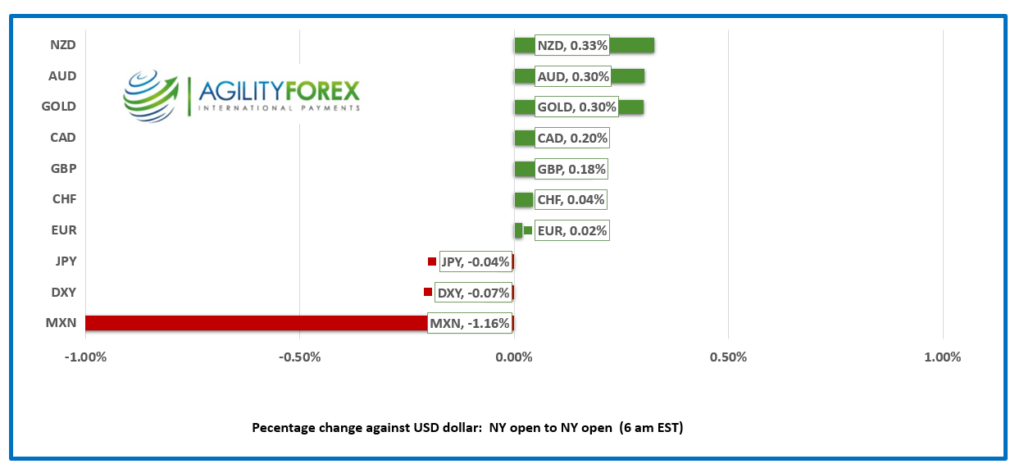

FX at a Glance

Source: IFXA/RP

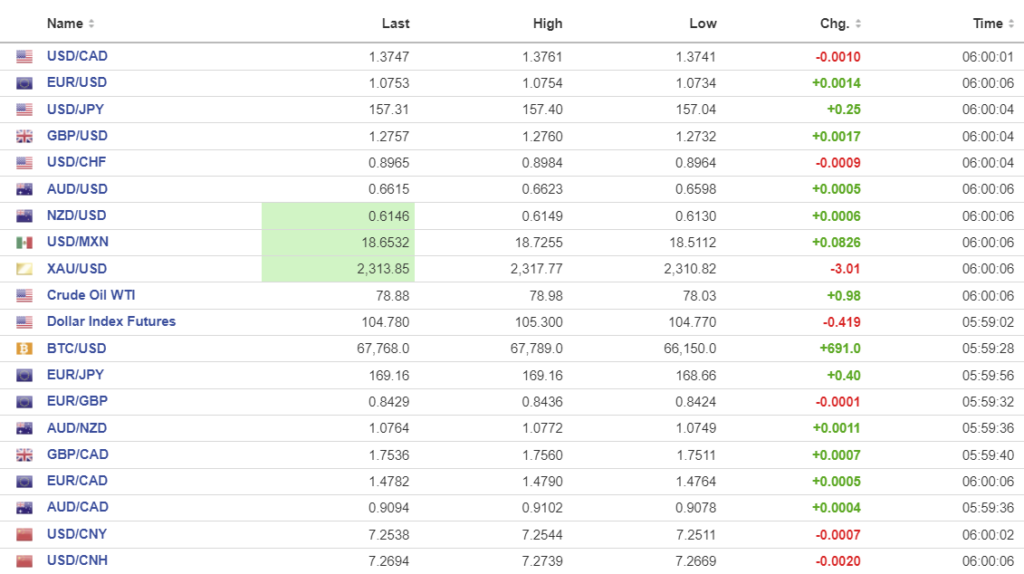

USDCAD open 1.3747, overnight range 1.3703-1.3761, close 1.3759

USDCAD dropped to 1.3703 after US CPI cooled a tick more than expected. Prices had inched lower overnight coinciding with the10-year CAD/US interest rate spread narrowing to 89.0 today from 93.2 yesterday. USDCAD direction is at the mercy of US dollar sentiment following today’s US CPI data and FOMC meeting.

WTI oil prices inched higher, rising from 78.03 to 78.98, supported by yesterday’s API data showing US crude inventories fell 2.42 million barrels in the week ending June 7. Traders are also digesting the latest International Energy Agency (IEA) report that warned global oil demand would peak in 2029, followed by a major supply surplus.

There are no Canadian economic reports of note today.

USDCAD Technicals

The USDCAD intraday technicals are modestly bearish while trading below 1.3760 and looking for a move below the June uptrend line at 1.3710 to extend losses to 1.3650. All of that is possible if today’s CPI data and FOMC meeting are tame.

Longer term, the uptrend line from the beginning of January 2024 is intact while prices are above 1.3610. Support from the 100-day and 200-day moving averages lies just below that level.

For today, USDCAD support is at 1.3740 and 1.3710. Resistance is at 1.3810 and 1.3850. Today’s range is 1.3710-1.3810.

Chart: USDCAD 4 hour

Source: DailyFX

Inflation cools-10-year Treasury Yield plummets.

US CPI rose 3.3% y/y in May, a tick lower than the 3.4% expected and Core-CPI rose 3.4% rather than the 3.5% predicted and 3.6% y/y in April. Bond traders were overjoyed and drove the US 10-yeear Treasury yield from 4.40% to 4.28%. The data is not likely to alter the FOMC dot-plot projections.

Patience, Patience, Patience

The FOMC will leave rates unchanged today but issue a new set of projections and forecasts. A host of Fed policymakers have spent the time since the last meeting telling all who would listen that the Fed needs to be patient and is in no hurry to cut interest rates. Neel Kashkari tossed out the (slim) possibility that rates could be raised. With that in mind, the dot-plot should indicate just two or fewer cuts for 2024. If so, the US dollar will remain bid.

G-7 to China—Stop Enabling Russia’s War on Ukraine

The G-7 is already leaking parts of the end of summit communique from Italy which starts this weekend. So essentially, they are issuing a statement about the leaders’ discussions which haven’t taken place. Bloomberg reports that the G-7 “will call on China to stop enabling and sustaining Russia’s war against Ukraine. China’s ongoing support for Russia’s defense industrial base has significant and broad-based security implications.” The G-7 leaders are very quiet about China’s harassment and bullying of Taiwan and the Philippines. In addition, Canada’s Justin Trudeau will likely pledge tens of billions of dollars for climate change initiatives to some country, somewhere, preferably one with pristine beaches and 5-star accommodation.

EURUSD

EURUSD traded in a 1.0734-1.0755 range, then spiked to 1.0827 after US inflation rose a tad less than expected. The steep drop in 10-year Treasury yields fueled the rally. Earlier today, German CPI data came out as expected and it was ignored. EURUSD gains are limited due to uncertainty around the French elections with the first round of votes due June 30. French Finance Minister Bruno Le Maire invoked the horror of the UK Liz Truss/Kwasi Kwarteng bond debacle if Marine LePen’s right-wing party gains a majority.

GBPUSD

GBPUSD soared to 1.2845, post—CPI, after trading in a 1.2732-1.2760 range overnight.UK Manufacturing and Industrial Production data were soft but ignored. The UK economy stagnated in April with GDP at 0% compared to 0.4% in March. The poor economic growth was attributed to rainy weather as April was one of the wettest months on record.

USDJPY

USDJPY dropped to 156.32 after peaking overnight at 157.43 on the back of the steep drop in US Treasury yields.

AUDUSD rallied sharply, post US CPI, reaching 0.6684 after drifting in a 0.6598-0.6623 range overnight. Australian Treasurer Jim Chalmers is touting a “soft landing” for the economy despite the RBA hiking rates aggressively. Premier Li Qiang is visiting Australia on the weekend—a sign of improving Australia/Chinese relations.

NZDUSD mirrored AUDUSD moves and jumped to 0.6210 after trading quietly in a 0.6130-0.6149 range.

USDMXN

USDMXN rallied further, rising from 18.5112 to 18.9874 overnight and did not get much of a reprieve after the US inflation numbers. USDMXN sentiment is bullish after incoming President Claudia Sheinbaum said she would proceed with her predecessor’s 20 constitutional reforms which many believe, eliminates regulatory and oversight agencies, in order to increase presidential power.

BTCUSD (Bitcoin)

BTCUSD was uninspired and traded in a 66,150-67,909 range overnight then pooped to 69,486 after the inflation data.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

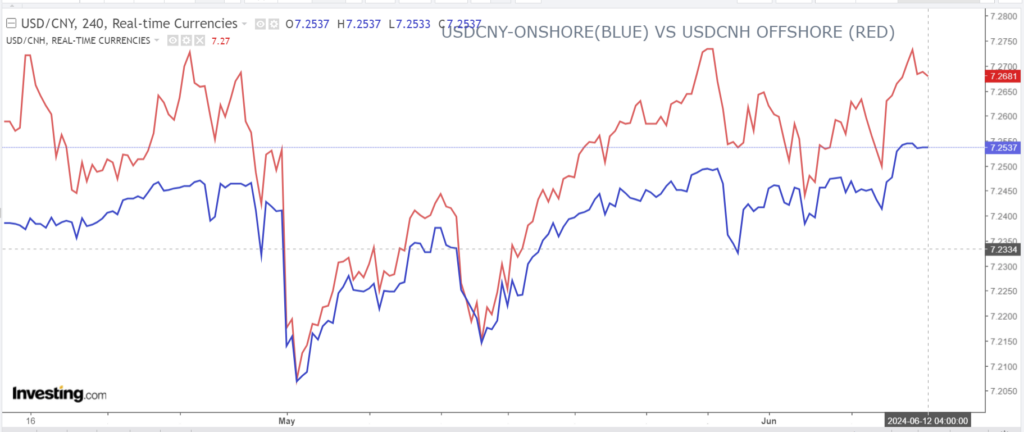

China Snapshot

PBoC fix: .1133 vs exp. 7.2558 (prev. 7.1135).

Shanghai Shenzhen CSI 300 rose 0.04% to 3544.12.

China May CPI falls 0.1% m/m (forecast 0, April 0.1% m/m) Annual CPI rises 0.3% y/y, unchanged from April but below the forecast of 0.4%y/y.

Producer Prices fall 1.4% y/y, forecast -1.5%, April -2.5%

Today’s inflation data suggests Chinese authorities have more work to do to boost the economy.

Chinese officials are considering a ban on retail distribution for hedge funds

Chart: USDCNY and USDCNH

Source: Investing.com

Vietnam Snapshot

Chart 3 month

Source: Yahoo

Malaysia Snapshot.

Chart 3 month

Source: Yahoo