Photo:Etsy

May 19, 2023

- Powell discussion with Bernanke at 11:00 am.

- June rate hike pause hopes fading as debt deal hopes rise.

- US opens mildly defensive on pre-weekend profit-taking.

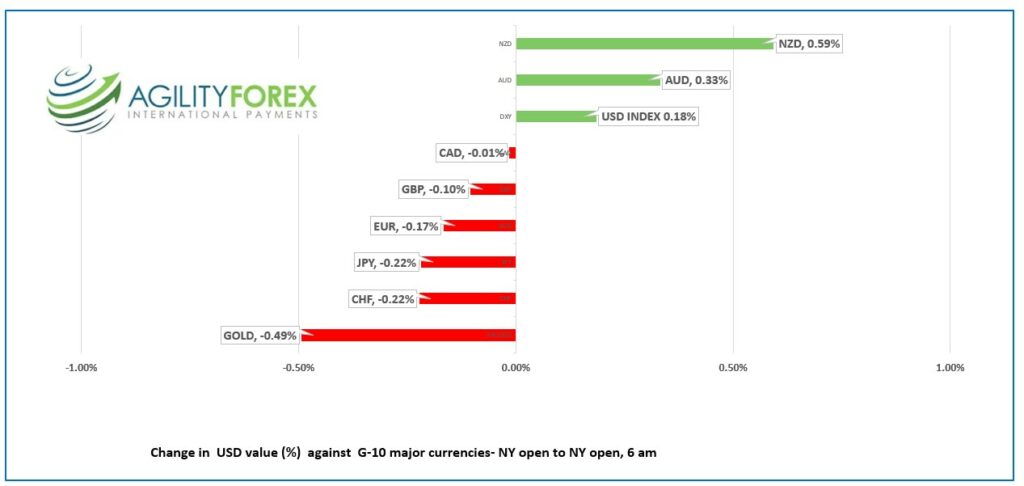

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3470-74, overnight range 1.3472-1.3511, close 1.3502

USDCAD slipped after touching 1.3511 in Asia on renewed hopes for a US debt ceiling deal some time next week. Those hopes improved risk sentiment which sparked US dollar selling due to profit-taking and position adjustment ahead of the weekend.

The Bank of Canada Financial System Review stated the obvious. It noted that financial conditions have tightened over the past year. The BoC is more concerned than it was last year about the ability of households to service their debts, especially as mortgages get renewed. That’s on Governor Macklem.

On June 15 2020, he said “If you’ve got a mortgage of if you’re considering making a major purchase, or you’re a business and you’re considering making an investment, you can be confident rates will be low for a long time.”

Three years is not a long time. Maybe its time to turf Tiff.

Canada’s Retail Sales fell 1.4% m/m in March, as expected while the ex-autos component fell 0.3%, which was better than the -0.8% dip forecast. USDCAD did not react to the data.

Canadian’s will be fleeing offices early to get a head start on the first long weekend of the summer.

USDCAD Technical Outlook

The USDCAD intraday technicals are in a symmetrical triangle pattern defined by 1.3410 at the bottom and 1.3520 at the top. A topside break targets 1.3660 while a downside move will hit support at 1.3310.

Longer term, the USDCAD technicals are bullish. Prices are in an uptrend from the beginning of June 2021 while above 1.2960 and consolidating the post September 2022 rally in a 1.3210-1.3660 range.

For today, USDCAD support is at 1.3430 and 1.3390. Resistance is at 1.3520 and 1.3550

Today’s range 1.3430-1.3530

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

“There are strange things done in the midnight sun” and I’m not talking about the cremation of Sam McGee. Financial markets are in the throes of spring fever.

The US 10-year Treasury yield climbed to 3.652% today from 3.468% on Tuesday. Trader’s are beginning to believe the Fed’s narrative and are lowering expectations that the Fed will leave rates unchanged on June 14. That should mean falling equity prices, but not this time.

The Nasdaq closed 3.04% higher since Monday, while the S&P 500 gained 2.14% and the US dollar gave back some gains overnight.

The G-7 are rumoured to be discussing a Russia-Ukraine peace proposal although, without Russia involved, it sounds like a waste of breath. Ukraine President Zelensky is a guest at the meetings, and he is expected to ask for more sophisticated weapons.

Risk sentiment is also positive, hoping a debt ceiling deal will be reached next week.

Fed Chair Jerome Powell is slated for a panel discussion with former Fed Chair Ben Bernanke.

EURUSD ranged in a 1.0761-1.0815 band. Prices are supported by the improved risk tone but concerns the Fed could raise rates in June will limit the upside.

GBPUSD is at the top of its 1.2394-1.2461 range due to broad US dollar weakness on improved risk sentiment.

USDJPY retreated from its overnight peak but stayed inside its overnight 137.98-13872 range. Firm US Treasury yields, and a dovish Bank of Japan outlook is underpinning prices.

AUDUSD climbed from 0.6618 in Asia to 0.6671 in early NY thanks to US dollar weakness and higher S&P 500 futures.

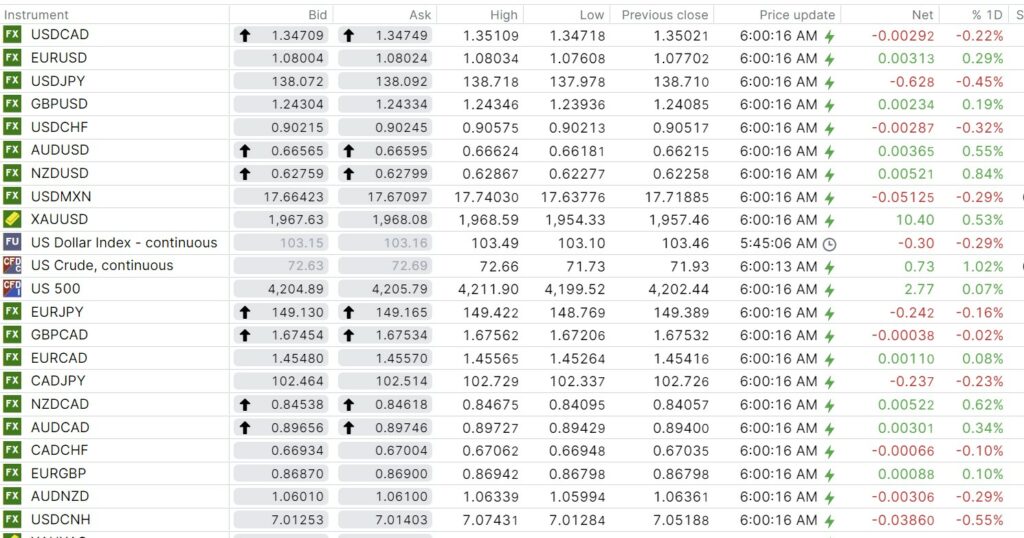

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

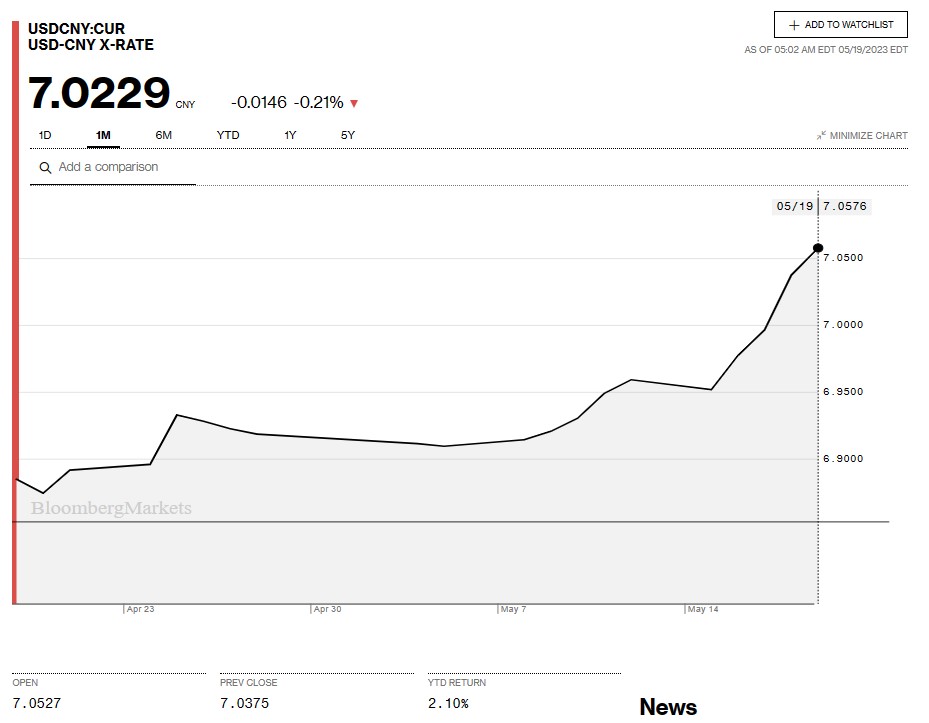

China Snapshot

Bank of China Fix: 7.0356 previous 6.9967

Shanghai Shenzhen CSI 300 fell 0.29% to 3944.54.

Chart: USDCNY 1 month

Source: Bloomberg