December 12, 2024

- ECB cuts rates by 25 bps-outlook dovish

- November CPI and today’s weekly jobless claims support 25 bp Fed rate cut.

- US dollar trading slightly lower ahead of data and ECB

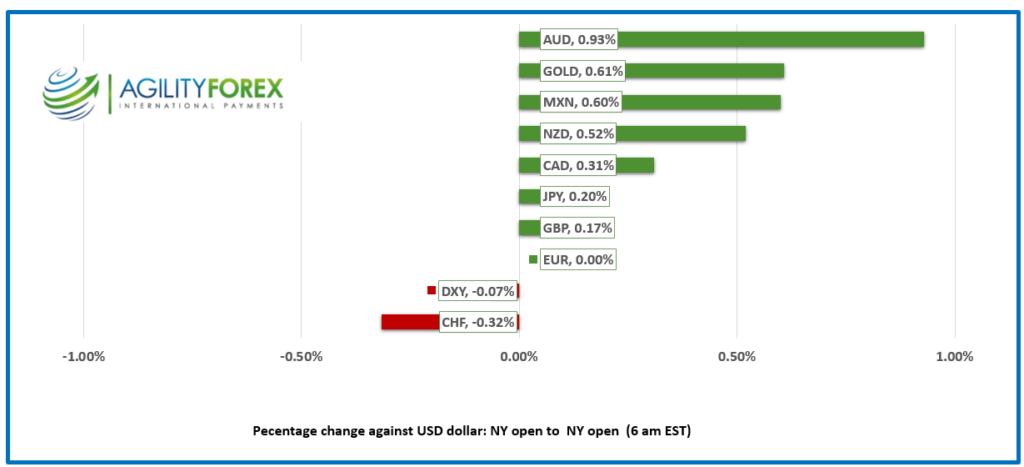

FX at a Glance

Source: IFXA/RP

USDCAD open 1.4145, overnight range,1.4131-1.4175, close 1.4161

The Bank of Canada slashed its benchmark rate by 50 bps yesterday.

The move was mostly expected, and USDCAD dropped from 1.4165 just before the news to 1.4120 immediately afterwards. The move did not last. USDCAD topped out this morning at 1.4175 after the ECB rate decision boosted US dollar demand.

USDCAD rallied as traders quickly realized the rate cut was the Bank of Canada admitting that the domestic economy is extremely weak.

Tiff Macklem justified the action due to the belief that the Federal government’s plan to lower immigration will negatively impact GDP growth. Of course, that is assuming that the government actually follows through on the plan. The cut was also justified because of the risk of a drop in inflation to 1.5% in January due to the GST holiday.

He also suggested the 50 bp cut was needed to help offset uncertainty surrounding tariff threats.

Oil prices climbed yesterday and consolidated the gains in a 70.12-70.72 range overnight.

Prices were boosted after Opec slashed its oil demand forecast for 2024 due to China’s sluggish economy. Opec cut its 2025 forecast of oil demand growth to 1.45 million bpd from 1.54 million bpd.

There are no Canadian economic reports of note today.

USDCAD Technicals

The USDCAD technicals are bullish. Yesterday’s failure to extend losses following the BoC rate cut and the quick rebound suggests an underlying bid. At the same time, the failure to rally above 1.4200 suggests traders are awaiting a fresh catalyst which may be next week’s FOMC meeting. Until then, a 1.4100-1.4200 range is likely.

The daily chart shows that the uptrend line that started at the beginning of October will continue to guide prices higher while 1.4040 remains intact. The trend line is guarded by support at 1.4100 and 1.4060.

For today, USDCAD support is 1.4130 and 1.4100. Resistance is 1.4200 and 1.4250.

Today’s Range: 1.4110-1.4190.

Chart: USDCAD 4 hour

Source: Investing.com

Trump Mistakes Inauguration for Coronation.

President-elect Donald Trump reportedly invited China President Xi Jinping to his January 20 inauguration. Mr Trump may be confused—after all, he is 78 years old, a mere 4 years younger than faculty-challenged President Biden.

Traditionally, world leaders get invited to coronations, which symbolize hereditary monarchy and divine right. Inaugurations are meant to celebrate democracy and the peaceful transfer of power (except for January 6, 2020).

Maybe Donnie thinks he is getting crowned?

Mixed Bag of US Data

US weekly jobless jumped to 242,000 from 218,500 last week. It supports a Fed cut but historically the number is still low. PPI rose 0.4% in November (forecast 0.2%). However the results were distorted by a 54% jump in the price of eggs.

EURUSD

EURUSD drifted aimlessly in a 1.0492-1.0531 range ahead of this morning’s ECB rate decision and then dropped to 1.0469 after the ECB announced a 25 bp rate cut. The statement was somewhat dovish as it said that “Most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis.” The ECB also lowered their inflation forecast with Core CPI projected at 2.9% in 2024 and 2.3% in 2025.

The Swiss National Bank surprised traders when it slashed its benchmark rate by 50 bps. The SNB move was designed to offset other central bank rate cuts and to put the brakes on CHF gains.

GBPUSD

GBPUSD is spinning its wheels in a 1.2740-1.2788 range as traders await the ECB decision. A larger-than-expected rate cut would underpin GBPUSD due to EURGBP selling.

The BoE is expected to leave its benchmark rate unchanged at next week’s meeting, which will provide additional GBPUSD support.

USDJPY

USDJPY traded sideways in a 151.95-152.79 band as news reports suggested that the BoJ will leave rates unchanged next week.

The Japan Times reported that BoJ officials see little cost to waiting as there are few signs that inflation could overshoot.

AUDUSD and NZDUSD

AUDUSD surged from 0.6369 to 0.6430 following a hotter-than-expected employment report. Australia added 35,600 jobs (forecast 25,000) in November while the unemployment rate dropped to 3.9% from 4.1% in October.

Forecasters were expecting that the unemployment rate would rise to 4.2%. The results lowered the odds for an RBA rate cut in February to 50/50.

NZDUSD traded higher in a 0.5784-0.5817 range despite soft electronic card retail sales data, which fell 2.3% y/y compared to a 1.1% y/y result in October.

USDMXN

USDMXN continued to trade defensively in a 20.1029-20.1608 range. The recent soft inflation data raised the odds that Banxico cuts rates by 25 bps next week.

In addition, Trump has toned down his anti-Mexico tariff rhetoric, which has given the peso a reprieve from selling. Mexican markets are closed today for a holiday.

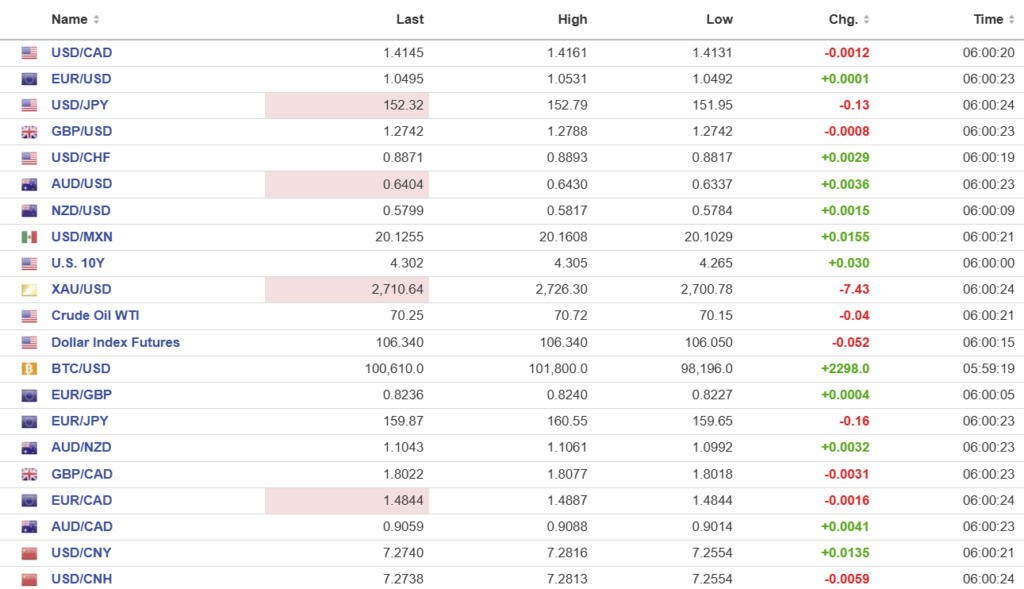

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC Fix: 7.1854 vs exp. 7.2438 (prev. 7.1843)

Shanghai Shenzhen CSI 300 rose 0.99% to 4028.50

The China Finance 40 Forum suggests that policymakers should anchor the yuan to a basket of non-US dollar currencies. The group wrote, “Given the stronger dollar and tariff threats posed by Donald Trump’s re-election, intensified external uncertainties could limit the space for domestic monetary policies aimed at maintaining internal and external balance.”

The PBoC doesn’t appear to be a fan. One of their publications “Financial News” wrote that the yuan’s exchange rate was poised to stabilize or strengthen by the end of the year.

Chart: USDCNY and USDCNH

Source: Investing.com