March 18, 2024

- Canada CPI rises just 2.8% y/y (January 3.1%)

- USDJPY rallies despite BoJ rate hike.

- S dollar consolidating overnight gains.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3573-1.3577, overnight range 1.3520-1.3610, close 1.3534

USDCAD opened on a firm note than spiked from 1.3567 to 1.3610 in the wake of a cooler than expected inflation report. February CPI rose just 2.8% y/y compared to the estimates for an increase of 3.2%. The more important BoC Core CPI rose just 2.1% y/y, well below the 2.4% seen in January. Today’s result puts CPI well within the BoC target range (1-3%) and opens the door to a BoC rate cut, perhaps as early as June 5.

USD/CAD gains may be limited by higher oil prices. WTI rose from $81.83 to $82.26 after successful drone strikes on Russian oil terminals raised fears of another supply disruption. In addition, there are reports that Iraq will reduce exports in the coming months.

USD/CAD Technicals

The USD/CAD intraday technicals are bullish, supported by the uptrend line from March 14, which comes into play at 1.3540 (hourly chart), and the break above resistance at 1.3560 overnight. That sets the stage for a test of the resistance cluster in the 1.3590-1.3605 area, which, if broken, extends the rally to 1.3630.

The USD/CAD uptrend line from the beginning of January is intact while prices are above 1.3470, and looking for a break above 1.3630 (61.8% Fibonacci retracement of the November-January range) to extend gains to 1.3770.

For today, USD/CAD support is at 1.3540 and 1.3510. Resistance is at 1.3610 and 1.3630. Today’s range is 1.3540-1.3630.

Chart: USDCAD daily

Source: Investing.com

G-10 FX

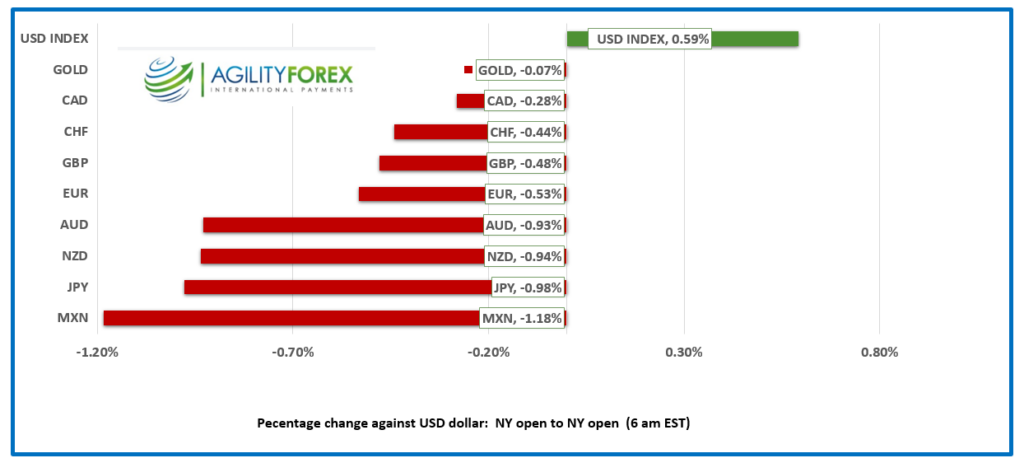

“Hark! The herald angels sing, ‘Negative rates are not a thing.’” The Bank of Japan did almost exactly as the Nihon Keizai Shimbun newspaper (Nikkei news) said they would in an article on Monday. The BoJ ended its 17-year long negative interest rate policy to great media fanfare.

Traders were less than impressed. The major Asian equity indexes closed higher except for Hong Kong’s Hang Seng, which lost 1.24%. European bourses are positive, with the French CAC 40 rising 0.39% and leading the way. The UK FTSE 100 is the odd man out, and it is down 0.13%. S&P 500 futures are down 0.13%. The US 10-year Treasury yield is steady at 4.316%.

EURUSD inched lower in a 1.0835-1.0877 range. The German and Eurozone ZEW surveys provided mixed results. “Economic expectations for Germany are significantly improving. At the same time, more than 80 percent of those surveyed anticipate that the ECB will cut interest rates in the next six months,” ECB policymaker Luis de Guindos said that the central bank would be in a position to discuss cutting rates in June, which is really not saying anything.

GBPUSD traded defensively in a 1.2667-1.2747 range ahead of Wednesday’s UK inflation data dump (PPI, CPI, and Retail Price Index), the FOMC meeting, and Thursday’s BoE monetary policy decision.

USDJPY is garnering all the headlines. The news did not sink USD/JPY like many expected but instead drove prices from 149.01 to 150.70. “Sell-the-rumour, Buy-the-fact” in action. Traders were well short USD/JPY, and they scrambled to book profits. More importantly, the BoJ scrapped its yield curve control strategy (YCC). The reality is that instead of being charged next to nothing for deposits, Japanese savers can now earn next to nothing.

AUDUSD dropped rapidly, falling from 0.6564 to 0.6503 due to the one-two punch of a dovish RBA and a rallying US dollar. The RBA left rates unchanged as was universally expected, but they tweaked the policy statement. Instead of “not ruling out a further increase in interest rates,” which is what they wrote in February, they are now “not ruling anything in or out.” Analysts claim the tweak signals a neutral bias.

NZD/USD traded negatively in a 0.6033-0.6092 range due to broad US dollar strength. The RBNZ remains relatively hawkish due to elevated inflation. USD/MXN extended yesterday’s gains and rose from 16.8173 to 16.912 with prices tracking broad US dollar sentiment. Banxico meets on Thursday and could cut rates by 25 bps to 11.00%.

US Housing starts and Building permits data is ahead.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0985 vs exp. 7.2056 (prev. 7.0943))

Shanghai Shenzhen CSI 300 fell 0.72% to 3577.63.

The outlook for the Chinese economy remains soft. The property sector is depressed and the rise in retail sales was due to the Lunar New Year holidays however government infrastructure investment is helping to provide some support.

Source: FXStreet

Chart: USDCNY and USDCNH daily

Source: Investing.com