Picture: Pixabay/IFXA Ltd

Norges Bank hikes rates; BoE and SNB leave rates unchanged

Evergrande Group contagion fades, boosting risk sentiment

US dollar opens lower despite modestly hawkish FOMC, CAD outperforms

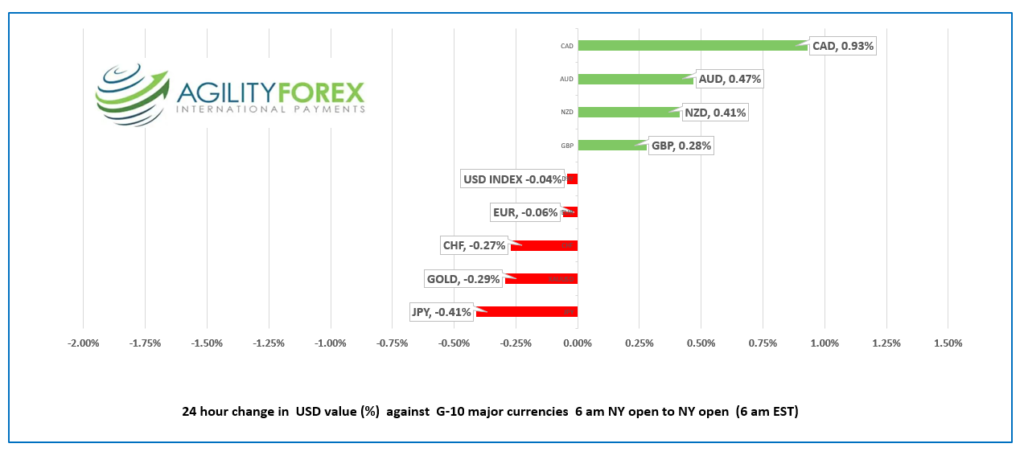

24-hour FX at a Glance:

Source: IFXA/RP

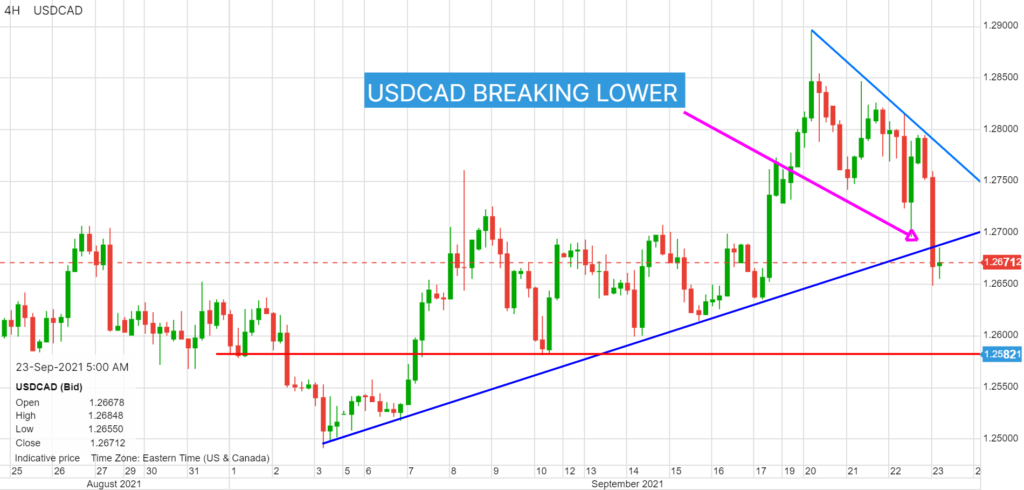

USDCAD Snapshot Open 1.2670-74 Overnight Range 1.2652-1.2794 Previous close 1.2776

USDCAD was trading around 1.2725 prior to the FOMC meeting, the bounced between 1.2699 and 1.2787 immediately afterwards. The dip occurred because the FOMC did not announce a tapering program at this meeting. The rally happened when it was implied tapering begins in November. Prices traded firmer and peaked in Asia at 1.2794. News the Chinese government continued to pump liquidity into the market and that the Chinese government may restructure Evergrande, turned risk sentiment positive. The US dollar retreated against the majors and USDCAD went along for the ride.

USDCAD saw further downside pressure from steady to firm WTI oil prices which bounced from a low of $69.55/barrel on Tuesday to $72.52/b overnight. Forecasts predicting a very cold start to winter, falling US crude inventories, and improved risk sentiment supported the rally.

USDCAD may see added pressure if July Retail Sales data (forecast 4.4% m/m vs 4.2% m/m in June)

Nevertheless, in the big picture, USDCAD direction is determined by the impact of US data on US rate hike expectations.

Technical view: The intraday USDCAD technicals are bearish below 1.2790, the downtrend from the September 20 peak of 1.2894, supported by today’s breach of the September 3 uptrend line at 1.2690. A break below 1.2630 targets 1.2580. A move above 1.2790 shifts the focus to 1.3000.

For today, support is at 1.2610 and 1.2580. Resistance is 1.2690 and 1.2740. Today’s range 1.2610-1.2690.

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

There was a flurry of activity around the FOMC statement and Fed Chair Powell’s press conference. The FOMC did not announce tapering, which was the consensus view. Still, during the press conference Mr Powell suggested that if things progress as anticipated, the conditions for “substantial further progress” would be met. That’s Fed-speak for tapering starts in November.

Chinese government actions served to downgrade the threat of contagion from Evergrande’s financial woes. The PBoC pumped liquidity in the market and there are reports Chinese authorities may restructure the company.

Asia stock markets closed mixed. The Hang Seng and ASX 200 gained while the Nikkei dipped. European bourses are higher except the FTSE which is flat. Wall Street futures point to a positive open. US 10-year Treasury yields are 1.337%, and gold is trading at $1771.24.

Norway’s Norges Bank raised interest rates from 0.0% to 0.25%, the first major central bank to do so in the post-pandemic world. Further increases are expected. The Swiss National Bank deferred changing monetary policy but promised to intervene in FX “as needed.”

US weekly jobless claims rose 16,000 to 351,000, compared to forecasts for a 15,000 dip to 320,000. The results had little impact on FX.

GBPUSD rallied from 1.3614 to 1.3683, then extend gains to 1.3718 after the BoE left interest rates and QE unchanged as expected. Two policymakers voted to reduce QE purchases. Traders noted that surging energy prices could drive inflation over 4.0%, which sparked talk about an earlier than expected interest rate increase. Traders ignored weaker than expected UK PMI data ahead. GBPUSD snapped the downtrend from September 14 and are targeting further gains to 1.3850.

EURUSD rallied from the post-FOMC low of 1.1684 to 1.1732. Disappointing German and Euro area Markit PMI data capped gains. German Manufacturing PMI fell to 58.5 from 62.6, while Eurozone PMI dropped to 58.7 from 61.4. The reaction was muted as the dips were due to supply bottlenecks. EURUSD remains vulnerable to a drop to 1.1600 due to the hawkish Fed outlook compared to the dovish ECB view.

USDJPY rallied to from 109.12 on Tuesday to 109.99 today due to safe-have yen flows being unwound, as Evergrande worries fade, and due to steady to firm US 10-year Treasury yields.

AUDUSD and NZDUSD bounced from overnight lows due to improved risk sentiment and higher commodity prices. AUDUSD gains were hampered by record COVID-19 cases in Victoria state.

US weekly jobless claims are expected 320,000 compared to 332,000 last week.

Chart of the Day- GBPUSD

Chart: Yahoo Finance

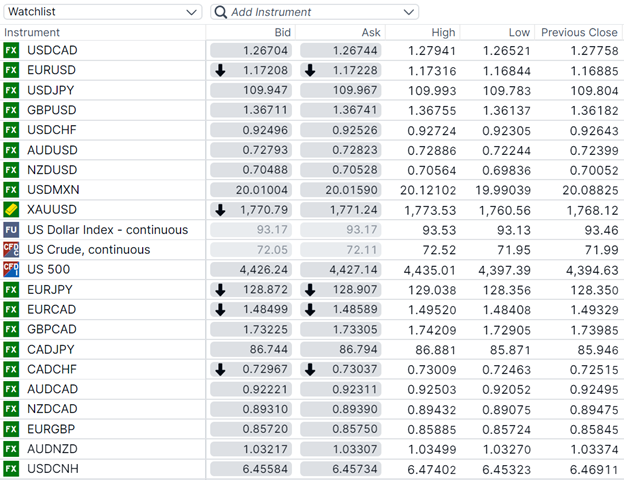

FX open, high, low, previous close

Source: Saxo Bank

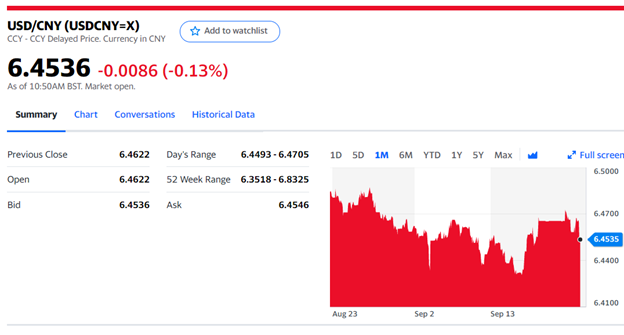

China Snapshot

Today’s Bank of China Fix, 6.4749, Previous 6.4693

Shanghai Shenzhen CSI 300 rose 0.65% to 4853.20

There are reports the Chinese government told Evergrande Group to avoid near-term default on USD bonds and that the Chinese government may restructure the company.

In addition, Evergrande did not mention payments for other bonds due Thursday.

PBoC injects CNY 60 billion into market.

Chart: USDCNY 1 month

Source: Yahoo Finance