Photo: publicdomain vectors

April 18, 2023

- Canadian inflation falls to 4.3% in from 5.2% in March.

- US earnings reports will drive risk sentiment today.

- US opens mixed from Monday but lower across the board, overnight.

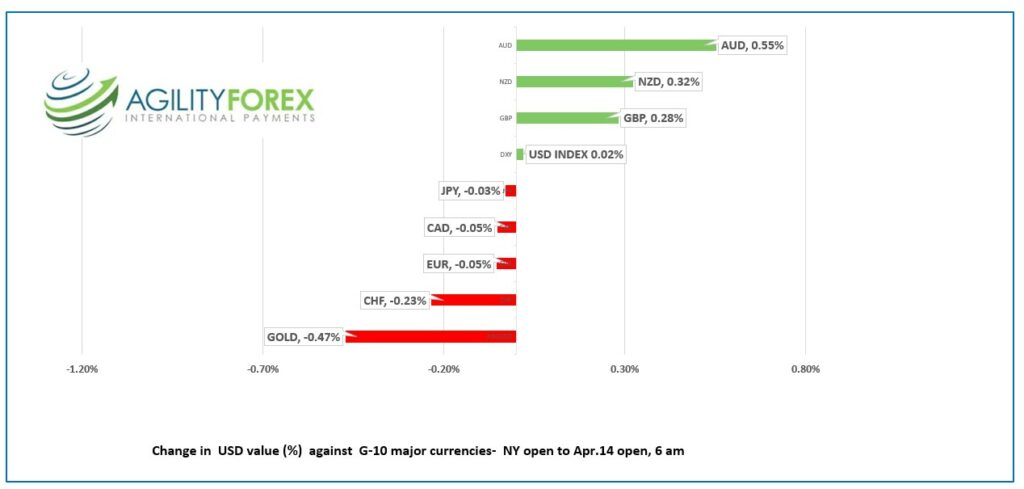

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3367-71, overnight range 1.3362-1.3395, close 1.3394

USDCAD dropped then bounced in the wake of the April inflation report and was basically unchanged within 15 minutes.

Statistics Canada wrote “The Consumer Price Index (CPI) rose 4.3% year over year in March, following a 5.2% increase in February. This was the smallest increase since August 2021 (+4.1%). On a year-over-year basis, Canadians paid more in mortgage interest costs, which was offset by a decline in energy prices.”

Consumers may not have noticed the slide in inflation, especially at the grocery store. Prices are still rising, just not as fast. Food prices rose 9.7%, compared to 10.6% in March.

Traders reacted with a collective “So What?” The results did not change the narrative of the BoC on hold and possibly planning to cut rates before year end.

WTI oil traded quietly in a $80.40-$81.25 range. Reuters is reported that the G-7 renewed its $60.0/b price cap for Russian oil, which according to Axios, reduced Russia’s export revenues by 50%.

USDCAD Technical Outlook

The intraday technicals are the same as yesterday. The short term downtrend and 200-day moving average are guiding prices lower while below the 1.3390-1.3400 area. A move below 1.3330 will lead to 1.3280. A topside break will lead to a test of the March downtrend line at 1.3440.

Longer term the move below the 200 day moving average (1.3400) targets 1.3220.

For today, USDCAD support is at 1.3330 and 1.3280. Resistance is at 1.3405 and 1.3440.

Today’s range 1.3300-1.3400

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global risk sentiment improved following better than expected Chinese growth data which took the wind from the sails of the recent US dollar rally. The improvement in risk sentiment is probably misguided as the y/y gain is measured against a period when China was closed due to covid.

Asian equity indexes closed with minor gains except the Australian ASX 200 which lost 0.29%. European bourses are in positive territory led by a 0.56% rise in the French CAC, followed by the German Dax index which has risen 0.51%. S&P 500 futures have gained 0.34%.

It is earnings season on Wall Street with quarterly reports from Johnson and Johnson, Bank of America, Netflix, and Goldman Sachs headlining the pack.

EURUSD traded firmer in a 1.0923-1.0982 range with traders ignoring disappointing German and Eurozone ZEW Survey results. German Economic Sentiment dropped 8.9 points to 4.1 in April. The ZEW survey statement said, “this means no significant improvement in ethe economic situation is expected in the next six months.” ECB President Christine Lagarde warned of a “new global map” as China and Russia try to move the world from the US dollar as the reserve currency.

GBPUSD jumped to 1.2443 from 1.2369, following stronger than expected three-month wage data (excluding bonus) which rose to 6.6% y/y (forecast 6.2%) while the data including bonus rose to 5.9% (forecast 5.1%). The previous data was revised upwards. The results raised the odds that the Bank of England will raise rates by 25 bps on May 11.

USDJPY climbed from 134.07 to 134.70 in Asia then drifted lower to 134.13 by the time NY opened. Prices are supported by the steady US 10 year Treasury yield (3.60%) and push-back against near-term Fed rate cuts. The USDJPY technicals are bullish above 132.20 but face resistance in the 135.10 area.

AUDUSD rallied from the opening bell, rising from0.6699 to 0.6744 in early NY trading. The gain was fueled by the RBA minutes pointing out that the rate hiking pause, may be just that-a pause, and not an end to the rate hiking cycle. In addition, risk sentiment improved after the Chinese GDP data raised the odds for a global recovery.

NZDUSD rallied from 0.6182 to 0.6218 due to improved risk sentiment and the prospect of more RBNZ rate hikes.

Today’s US data includes housing starts and building permits data.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Bank of China Fix: 6.8814, Previous: 6.8679

Shanghai Shenzhen CSI 300 rose 0.30% to 4162.03.

UBS raises 2023 growth forecast to 5.7% from 5.4% due to expectations of a stronger than anticipated recovery.

Q1 GDP 4.5% y/y (forecast 4%)

March Industrial Production 3.9% y/y, February 2.4%)

March Retail Sales 10.6% y/y (forecast 7.4%).

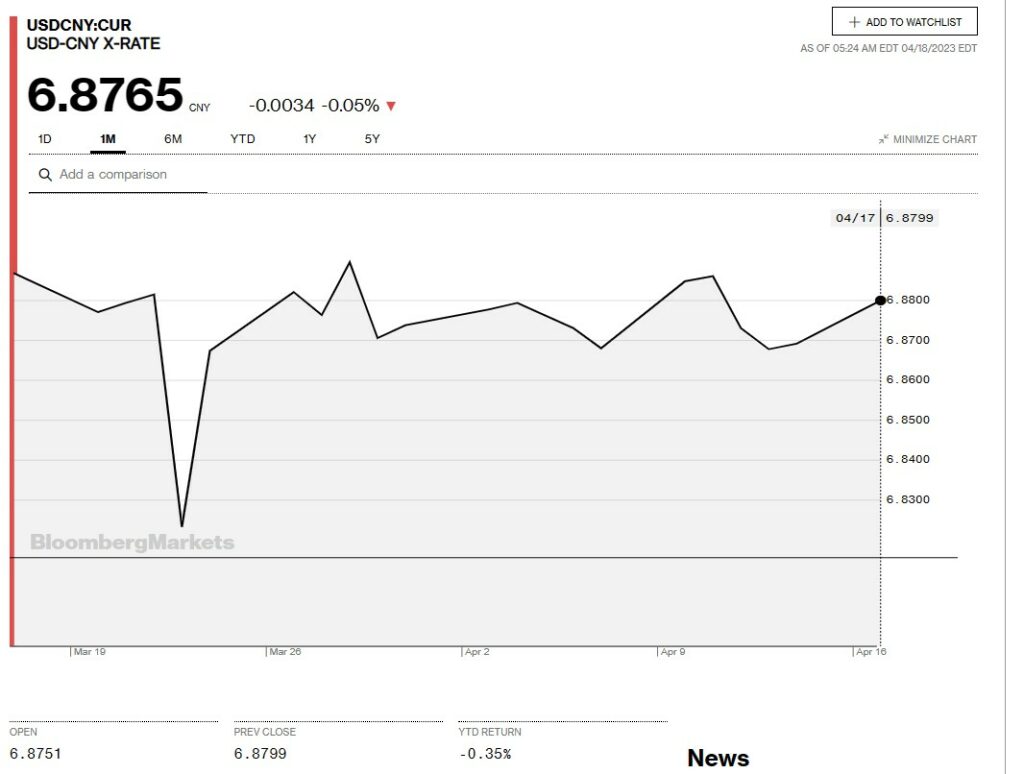

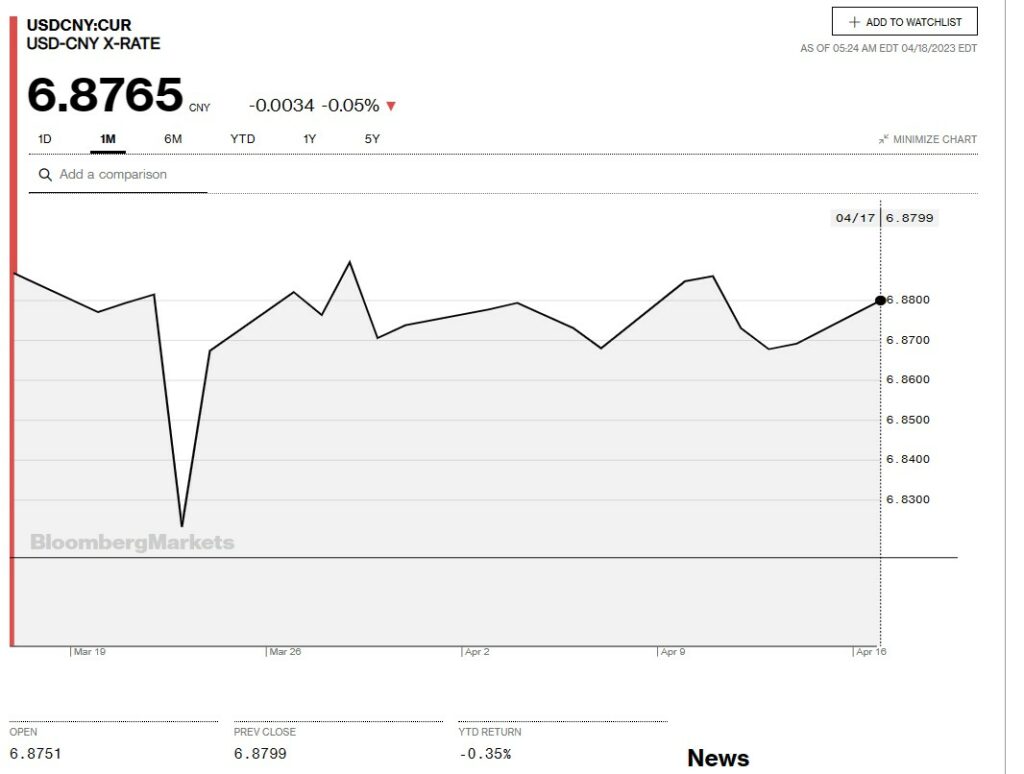

Chart: USDCNY 1 month

Source: Bloomberg