Source: HDclipart

- Russia/Ukraine exchange shells, and rhetoric

- FOMC minutes were stale

- US dollar rangebound and choppy

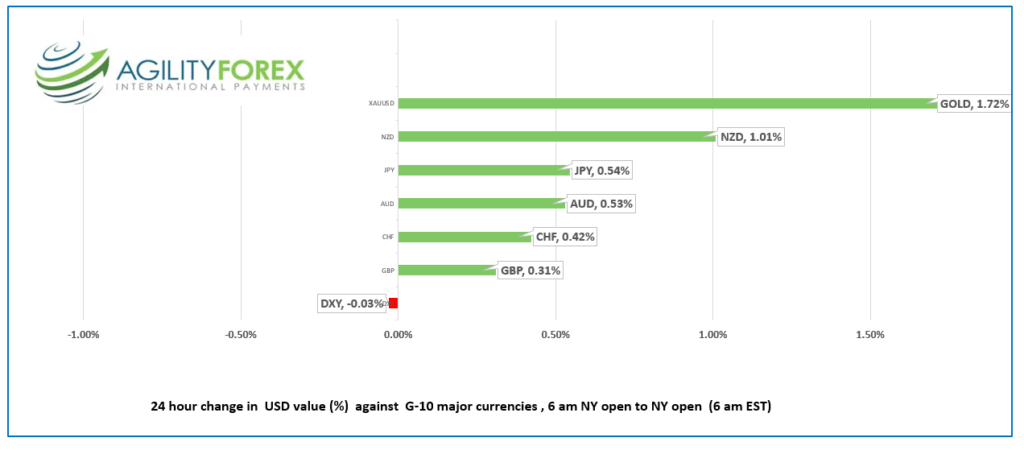

FX at a Glance

Source: IFXA Ltd/RP

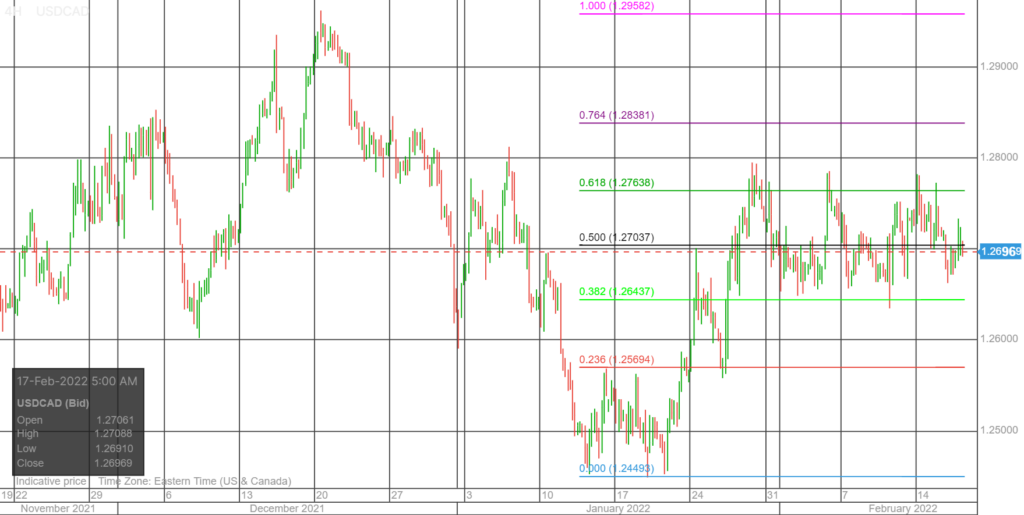

USDCAD Snapshot: Open 1.2700-04 Overnight Range-1.2682-1.2733, previous close 1.2691

USDCAD bobbed and weaved in a choppy, headline-driven overnight session. News of progress in the Iran nuclear talks weighed on oil as did the EIA report that US crude inventories rose by 1.21 million barrels in the week ending February 11.

Even so, oil price news was quickly forgotten as Russian and Ukraine headlines hogged the spotlight. US officials accuse Russia of “fake news” after the Kremlin reported troops were pulled back from the Ukraine border. The New York Times claims a “senior official” said Russia added 7,00 more troops.

USDCAD traders quickly forgot about the inflation report. January CPI was a hotter than expected 5.1% y/y, which suggests the Bank of Canada may need to be aggressive in raising interest rates. However, that seems unlikely. Yesterday, Deputy Governor Timothy Lane repeated the bank’s belief that “inflation will come down quickly in the second half of the year. What he didn’t say was the level inflation would fall from; 10%? -15%?.

Technical view: The intraday are unchanged from yesterday. USDCAD is rangebound in a 1.2650-1.2770 band. A topside break would extend gains to 1.2840 while a downside drop targets 1.2574. The uptrend line from June 2021 is intact above 1.2500.

For today, USDCAD support is at 1.2670 and 1.2640. Resistance is at 1.2730 and 1.2770. Today’s Range 1.2640-1.2730

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

S&P 500 DJIA futures traded firmly in early NY trading but gave back all those gains after US weekly jobless claims rose 23,000 to 248.000 last week. Analyst expected an increase of 219,000. Traders ignored the Building Permits and Housing Starts reports.

The FOMC minutes were anticlimactic. There were no surprises or fresh insight, which leaves the size of the March rate hike question unanswered.

European bourses have been choppy and have given up earlier gains in NY trading. Soil bounced in a $90.65-(3.27/b range and is at $91.65 in NY. Gold climbed to $1893.20 from $1868.08. the US 10-year Treasury yield sits at 2.011%.

EURUSD was steady in 1.1324-1.1385 band. ECB policymaker Pablo de Cos said, “the direction in which we need to head is clear, but we should not draw premature conclusions as to the time frame. The process will be both gradual and data-dependent.” The ongoing Russia/Ukraine tensions are also limiting EURUSD gains.

Chart: EURUSD 4 hour

Source: Saxo Bank

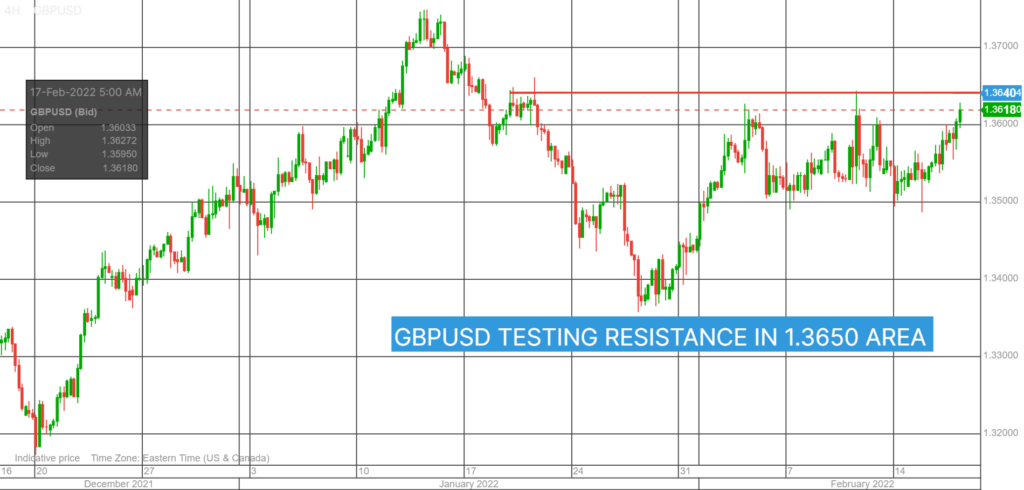

GBPUSD rallied to 1.3627 from 1.3557 on anticipation of a more aggressive Bank of England interest rate outlook following yesterdays inflation report. The intraday technicals are bullish above 1.3570 looking for a test of 1.3750.

Chart GBPUSD 4 hour

Source: Saxo Bank

USDJPY suffered from geopolitical tensions sparking safe-haven demand for yen which drove prices from 115.52 to 114.96.

AUDUSD and NZDUSD rallied alongside the improved risk tone. AUDUSD got a bit of a boost from more “wishy-washy” comments from RBA officials. Deputy Governor Guy Debelle said a rate hike could happen or then again, maybe not.

AUDUSD rallied to 0.7214 from 0.7151 supported by a better than expected employment report. Australia added 12,900 jobs compared to the forecast of 0. The participation rate ticked up to 66.2 from 66.1

NZDUSD climbed from 0.6661 to 0.6711 in NY supported by speculation the RBNZ may hike rates 0.50% at next week’s meeting.

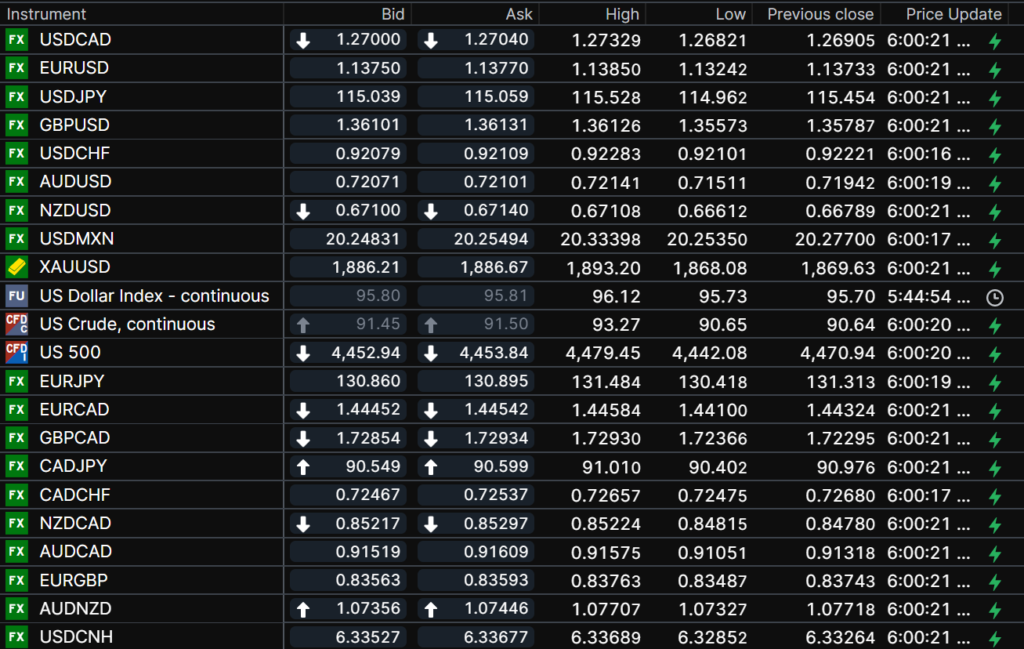

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

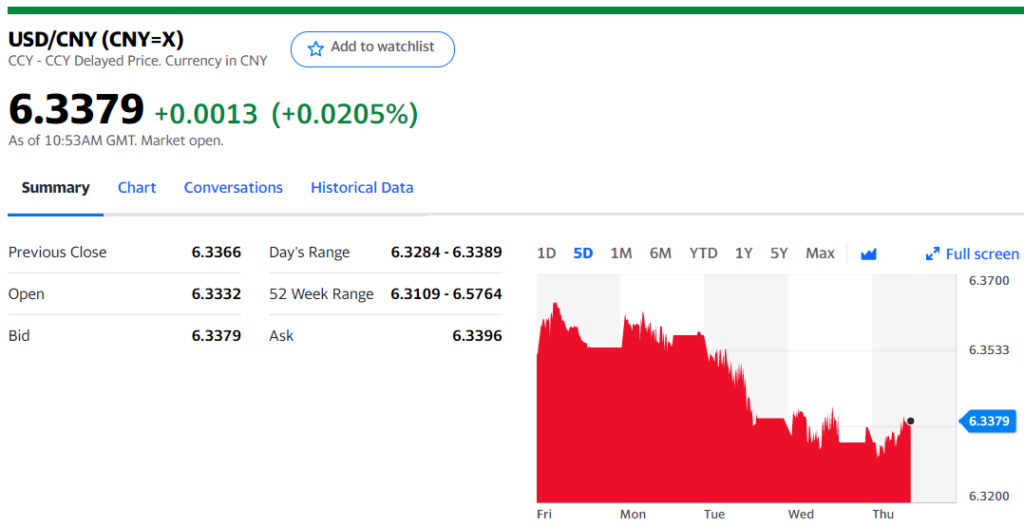

China Snapshot

Today’s Bank of China Fix 6.3321, previous 6.3463

Shanghai Shenzhen CSI 300 rose 0.24% to 4629.16

Chart: China 1 month

Source: Saxo Bank