Source: Wikimedia commons

- Most major markets are closed tomorrow

- No surprise from Canada November GDP

- US dollar retreats, opens at or near, session lows

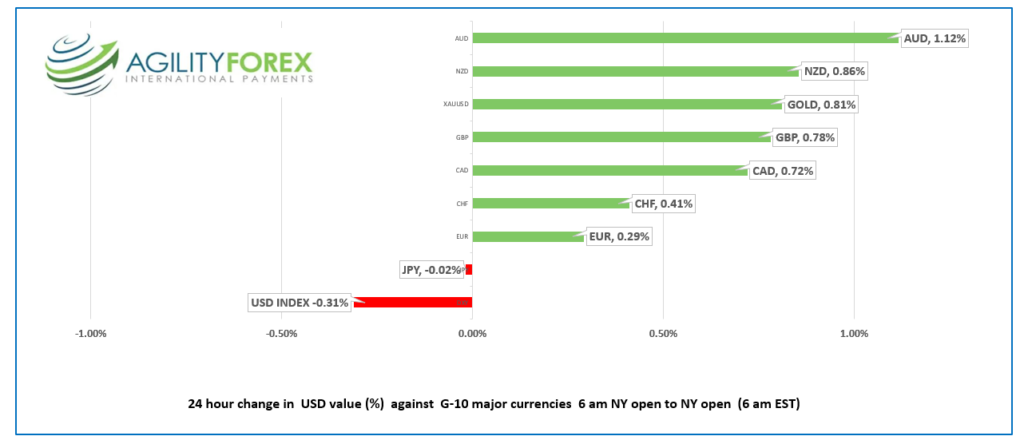

FX at a Glance

Source: IFXA Ltd/RP

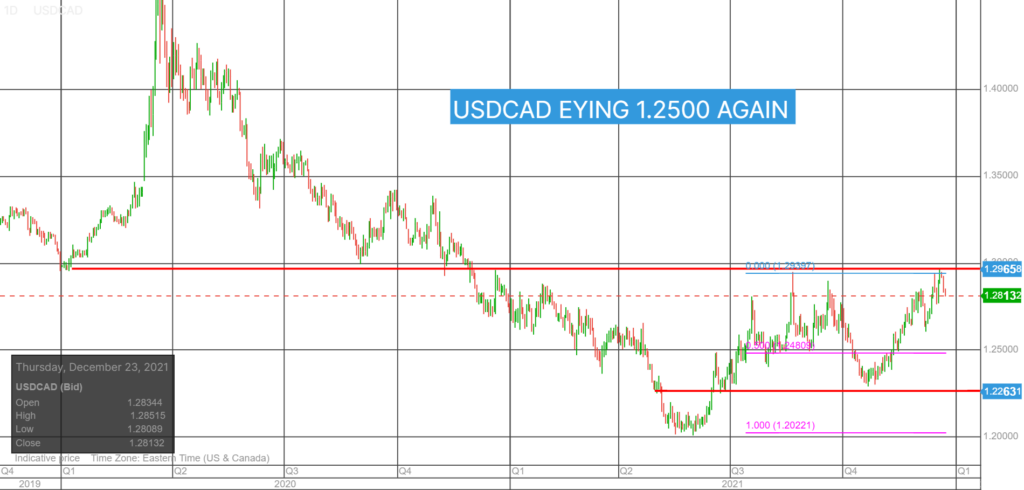

USDCAD Snapshot Open 1.2812-16, Overnight Range 1.2813-1.2852, Previous close 1.2852

USDCAD bulls may be on the menu for Christmas dinner. Broad-based US dollar selling followed economic reports suggesting good economic growth amid robust consumer confidence.

Risk sentiment improved further after early studies of the Omicron variant from the UK and Denmark said hospitalizations are 40-45% lower than for Delta.

WTI oil prices rallied on improved global growth prospects and after the Energy Information Administration (EIA) crude inventory data. US crude inventories fell 4.7 million barrels in the week ending December 17.

Canada October GDP rose 0.8% m/m as expected. The results did not have any impact on USDCAD trading.

Technical view: The intraday USDCAD technicals are bearish while trading below 1.2920. The decisive breach of the December uptrend line at 1.2860 shifts the focus to the November uptrend line which comes into play at 1.2730 (4 hour chart).

Fibonacci retracement of the October 27-December 20 range suggests a break below 1.2803 targets the 1.2703, the 38.2% retracement level, which if broken puts 1.2630 in play.

For today, USDCAD support is at 1.2810 and 1.2770. Resistance is at 1.2870 and 1.2910. Today’s Range 1.2810-1.2870.

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Merry Christmas. Markets are closed tomorrow in New Zealand, Australia, Europe, and the UK. US bond markets close at 2:00 pm today and are closed Friday. The New York Stock Exchange and CME are closed Friday. FX desks are open but will be very lightly staffed

The next Agility Forex daily will be December 29.

The US dollar is under pressure in thin holiday trading. Market risk sentiment is positive following reports that Omicron is less severe than the Delta variant and upbeat US economic reports yesterday.

Equity traders liked what they saw and bought stocks. S&P 500 and DJIA futures extended yesterday’s gains overnight, as the major Asia and European equity indexes posted gains. Gold and oil prices are firmer, while the US 10-year Treasury yield is steady at 1.473%.

US Durable Goods Orders rose 2.5% in November, well-above the 1.6% expected, while weekly jobless claims, and personal income and expenditures data were as forecast. The results were good enough to give the greenback a modest bid.

EURUSD tested downtrend resistance at 1.1341, then retreated to 1.1300, following the US data. ECB President Christine Lagarde reiterated her belief that inflation would drop to the bank’s target of 2.0% in 2022 which helped to cap earlier gains. European markets are closed Friday.

GBPUSD gave back some of today’s gains after the US economic data. GBPUSD rallied from 1.3344 to 1.3435 then fell to 1.3410 in NY. Prices are supported by diminished concerns about the Omicron variant and renewed speculation of additional BoE rate hikes.

USDJPY rallied with the improved tone to risk sentiment, with prices supported by steady US Treasury yields.

AUDUSD and NZDUSD joined the risk-on rally party, supported by higher commodity prices.

Chart of the Day: GBPUSD

Source: Yahoo Finance

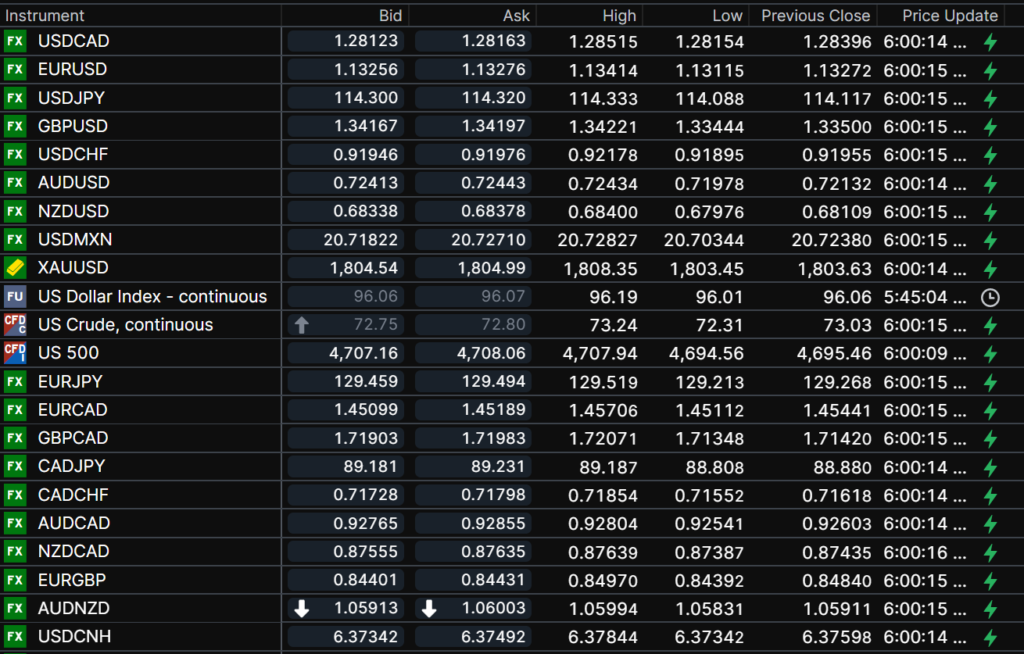

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

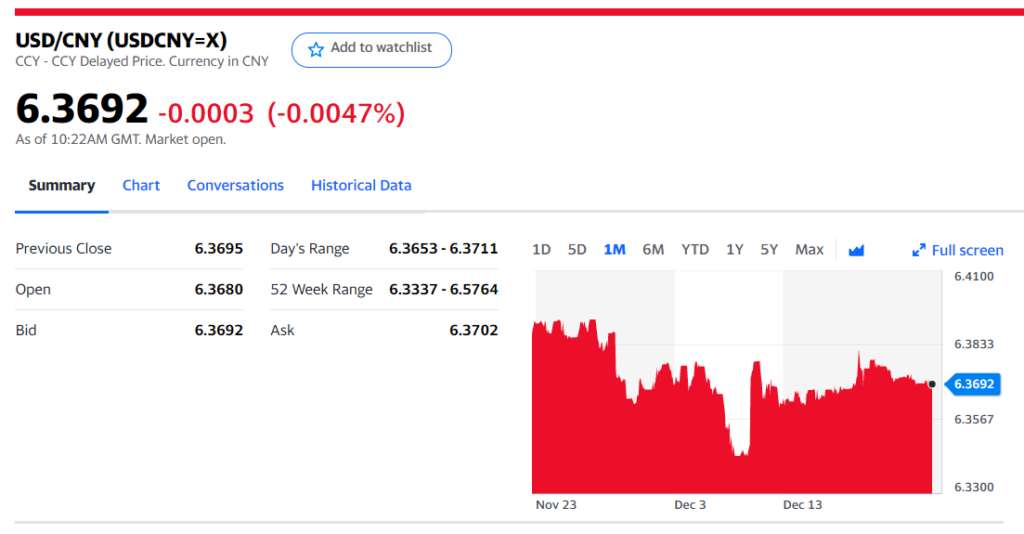

China Snapshot

Today’s Bank of China Fix 6.3651, Previous 6.3703

Shanghai Shenzhen CSI 300 rose 0.70% to 4,948.74

Chart: USDCNY 1 month

Source: Yahoo Finance