Photo: Amazon.com

- Risk sentiment sours on aggressive Fed rate hike fears

- European commission slashes growth and boosts inflation forecasts.

- US dollar opens strong, JPY underperforms.

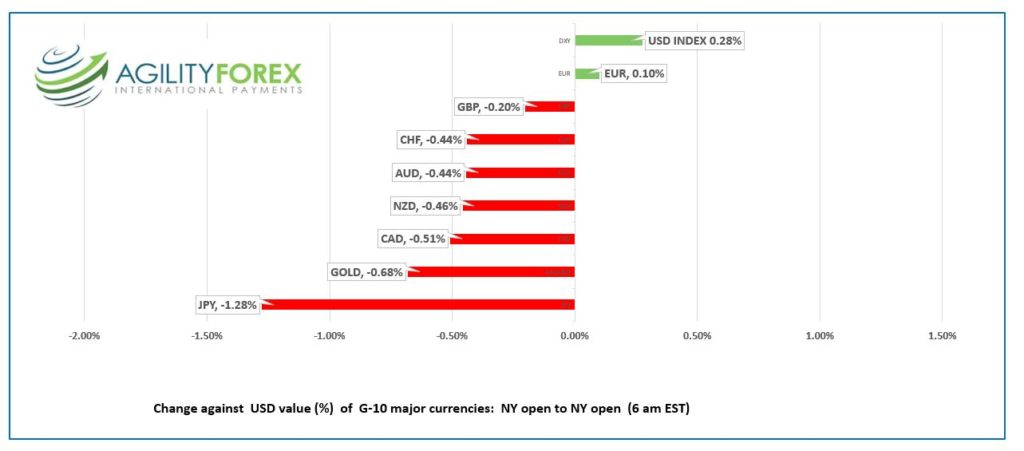

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3078-82, overnight range 1.1.2974-1.3156, close 1.2979

FX traders proved beyond any shred of doubt that USDCAD direction is dictated by the Fed and not the Bank of Canada (BoC). The evidence is incontrovertible.

The BoC surprised markets and jacked-up the overnight rate by 100 bps or 1.00% even though economists were positive rates would only increase by 0.75%.

USDCAD jumped from 1.2975 to 1.3060, prior to the BoC announcement after US inflation surged to a higher than expected 9.1% compared to 8.6% in May. The BoC announcement knocked USDCAD down to 1.2936 by noon.

That was it. The hotter than expected US inflation data followed by the BoC “jumbo” rate hike had traders speculating the Fed would follow the BoC lead and raise rates 1.00% on July 27. The bought US dollars across the board.

The US dollar rally accelerated in Europe after the European Commission released new forecasts of sharply higher inflation and lower growth.

USDCAD crushed resistance in the 1.3080 area, with prices touching 1.3156 in NY trading, setting the stage for further gains to 1.3500.

Even so, USDCAD gains will face tough sledding. WTI oil prices remain at lofty levels compared to this time last year. The war in Ukraine doesn’t have an end date and even when it does, sanctions on Russian oil won’t go away. China still needs oil and despite stupidly high prices, people will still drive.

Canada Manufacturing Sales fell 2% as expected but the May results were revised higher to 2.6% from 1.7%.

USDCAD technical outlook

The intraday USDCAD technicals are bullish following the breach of double top resistance in the 1.3070-80 area. Fibonacci retracement analysis projects further gains to 1.3340 which is the 50% retracement level of the March 2020 to June 2021 range, if prices remain above 1.3030.

For Today, USDCAD support is at 1.3070 and 1.3030. Resistance is at 1.3170 and 1.3210. Today’s Range 1.3110-1.3170

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

OMG! The Fed may raise rates by 1.00% at the July 27 meeting, and global markets are in a tizzy. Even if it happens, it is only 0.25% more than was almost universally expected, and just one hike with another three more to follow.

No big deal, but traders are skittish, and markets are thin.

Asian equity indexes closed with small gains except for Hong Kong’s Hang Seng index, which lost 0.22%. European bourses are in negative territory, with the UK FTSE 100 and German Dax index down 0.56%. S&P 500 futures are down 1.35%, WTI oil lost 2.63%, and Gold fell 1.46%. The 1US 0-year Treasury yield is 2.968%

The US weekly jobless claims report was a tad weaker than expected as the number of claims increased by 9,000 last week. June PPI index rose 1.1% m/m higher than expected.

EURUSD touched 1.0120 yesterday post-CPI, then retreated to spend the overnight session in a 1.0006-1.0059 range. The currency is weighed down by the latest European Commission forecasts that slashed 2023 GDP growth to 1.4% from 2.3% and predict inflation to average 7.6% in 2022 and 4% in 2023. The Russian invasion of Ukraine is blamed for the outlook, which said “uncertainty tips the balance of risks to adverse outcomes.” The EURUSD technicals are bearish and expect a breach of 1.0000 to extend losses to 0.9875.

GBPUSD mirrored EURUSD moves and traded with a bearish bias in a 1.1817-1.1891 range. Prices are undermined by expectations that the Bank of England will lag Fed hikes, UK recession risks, and ongoing political uncertainty.

USDJPY soared from 137.34 to 139.38 due to the outlook for sharply higher US rates in the face of stagnant Japanese rates. Traders do not fear BoJ intervention in FX as long as the Yield Curve Control policy caps JGB’s at 0.25%.

AUDUSD whipped about in a 0.6732-0.6787 range and is just above the bottom of that range in NY. Bullish sentiment from blow-out employment data and reports China may end its ban on Australia coal imports, was swamped by broad US dollar demand on speculation of a more aggressive Fed rate hike posture. Australia added 88,400 jobs (forecast 25,000) and the unemployment rate fell to 3.5% from 3.8%.

NZDUSD underperformed against its Australian cousin and traded in a 0.6094-0.6131 band.

Chart of the Day: USDJPY quarterly

Source: Saxo Bank

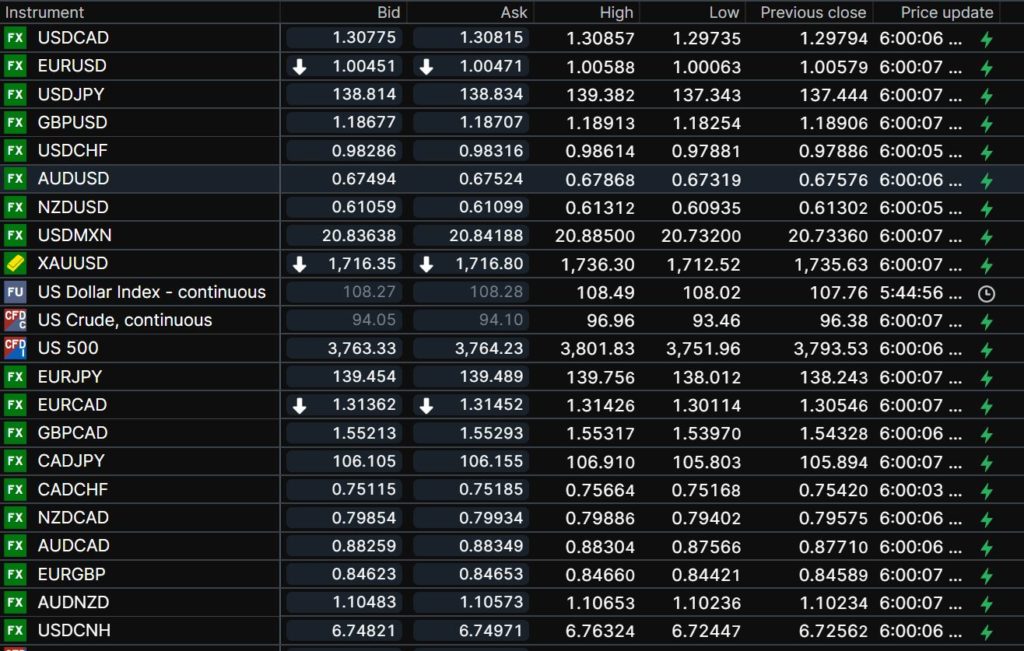

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.7265, previous 6.7282

Shanghai Shenzhen CSI 300 rose 0.01% to 4,322.07

China pondering end of its Australia coal ban in face of uncertainty over Russian supply.

.Chart: USDCNY 1 month

Source: CNBC