April 23, 2024

- Wall Street price action will drive FX direction today.

- US threatening sanctions on some Chinese banks

- US dollar opens little changed after quiet overnight session.

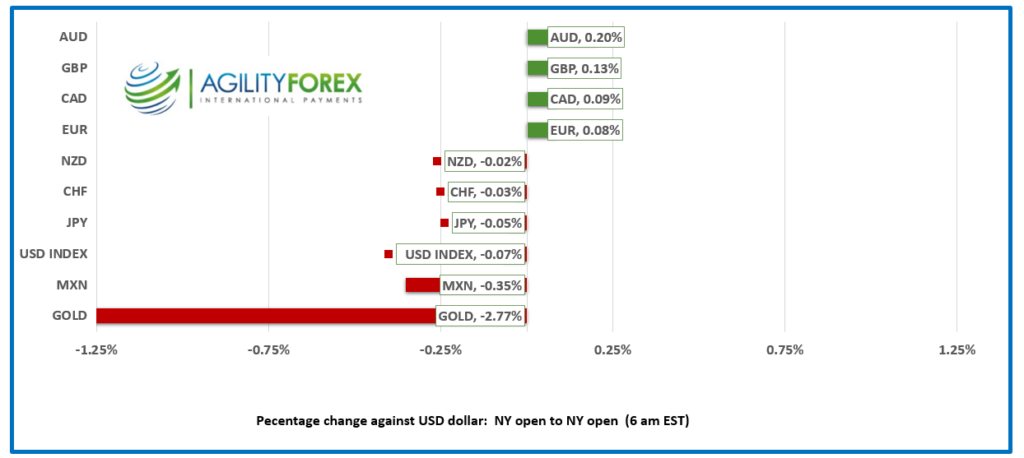

FX at a Glance

Source: IFXA/RP

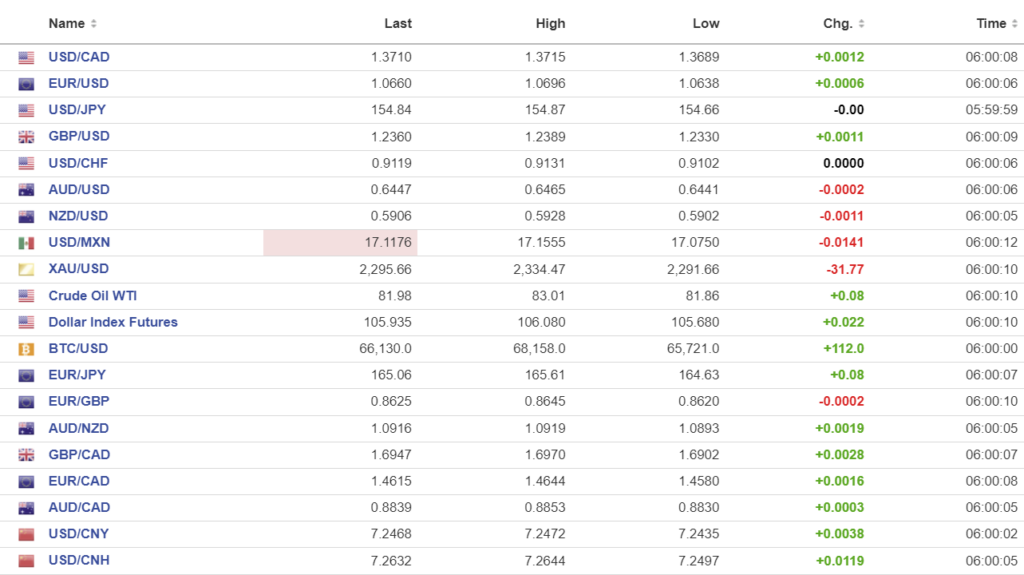

USDCAD Snapshot: open 1.3710, overnight range 1.3689-1.3715, close 1.3701

USDCAD drifted lower along with the improvement in risk sentiment yesterday, but the downtrend stalled overnight. Once again, USDCAD direction is dictated by US data and the Fed. The BoC still seems to be on track to cut rates in June while a slate of robust US data keeps the Fed firmly on hold. The prospect of a strong US GDP reading on Thursday and higher then expected PCE -price index data on Friday will limit USDCAD downside.

WTI oil traded in a 81.67-83.01 range overnight and is sitting at its session low in NY. The lack of further escalation in the Iran/Israel conflict has eased concerns of supply disruptions.

The Canadian data calendar is empty.

USDCAD Technicals

The intraday USDCAD technicals are bearish with prices in a downtrend channel between 1.3660- and 1.3670, on an hourly and 4 hour chart. A break above 1.3720 negates the downtrend and targets further gains to 1.3760.

The uptrend line from April 4 is intact above 1.3680 with further support in the 1.3660-80 area suggesting limited downside.

For today, USDCAD support is at 1.3680 and 1.3660. Resistance is at 1.3730 and 1.3750. Today’s range is 1.3680-1.3740.

Chart: USDCAD 4 hour

Source: DailyFX

Awaiting a catalyst

Traders are biding their time today. The European PMI data didn’t do the trick and the US dollar remained mired in narrow ranges overnight. There isn’t anything on the US or Canadian economic agenda that will generate interest today. But anticipation is building. Things will start to change tomorrow starting with Australian CPI, German IFO, Canadian Retail Sales and US Durable Goods orders, followed by US GDP on Thursday. The BoJ monetary policy meeting is Friday, but it is the US PCE-price index report that is key. A higher than expected result will suggest US rates could go higher, while a lower reading will raise hopes of an earlier than expected rate cut.

Equities and earnings

The S&P 500 closed at 5010.60 yesterday and that helped lift Asian equity indexes higher. The Nikkei 225 index gained 0.30% while Australia’s ASX 200 rose 0.45%. European bourses are in the green led by a 0.84% rise in the German Dax. S&P 500 futures are pointing to a positive open on Wall Street. Tesla’s quarterly earnings are due after the close.

EURUSD

EURUSD traded in a 1.0638-1.0696 range and is in the middle of that band in NY. Prices got a boost from improved risk sentiment as well as improving PMI data. German Composite PMI rose to 50.5 from 48.3 which raised hopes that the recession was over. Eurozone Composite PMI saw a similar improvement rising to 51.4 from 50.3. EURUSD needs to break above 1.0740 or risk further downside.

GBPUSD

GBPUSD chopped about in a 1.2330-1.2407 range. S&P Global economist wrote “PMI survey data for April indicate that the UK economy’s recovery from recession last year continued to gain momentum.” Services PMI Business Activity Index 54.9 (Mar: 53.1). 11-month high, Manufacturing PMI at 48.7 (Mar: 50.3) 2-month low. Even so, it is the US and UK interest rate outlook that is driving GBPUSD lower. Traders believe the BoE will cut rates by 150 bps more than the Fed.

USDJPY

USDJPY ticked higher in a 154.66-154.87 range. Japanese PMI data was a tad better than expected but it was ignored. Japan’s Finance Minister Shunichi Suzuki warned speculators that his meeting with his counterparts from Korea and the US set the stage for joint intervention. “I won’t deny that these developments have laid the groundwork for Japan to take appropriate action (in the currency market), though I won’t say what that action could be.”

AUDUSD and NZDUSD

AUDUSD traded in a 0.6441-0.6465 range and is at session lows in early NY partly due to China/US trade concerns. April PMI data delivered a mixed bag of results. Manufacturing PMI rose to 49.9 from 47.3 and Services PMI ticked down to 54.2 from 54.4. Traders are awaiting tomorrow’s CPI data. AUDUSD will continue to trade with a negative bias below 0.6500.

NZDUSD drifted in a 0.5903-0.5926 range with prices tracking broad US dollar sentiment. Gains may have been limited due to caution fresh trade drama between the US and China.

USDMXN

USDMXN traded with a modest negative bias falling from 17.1555 to 17.0750 due to broad US dollar selling pressures. The Mexican economy is expected to grow at 2.2% in 2024 due to the strong US economy which will drive higher exports and increased remittances.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

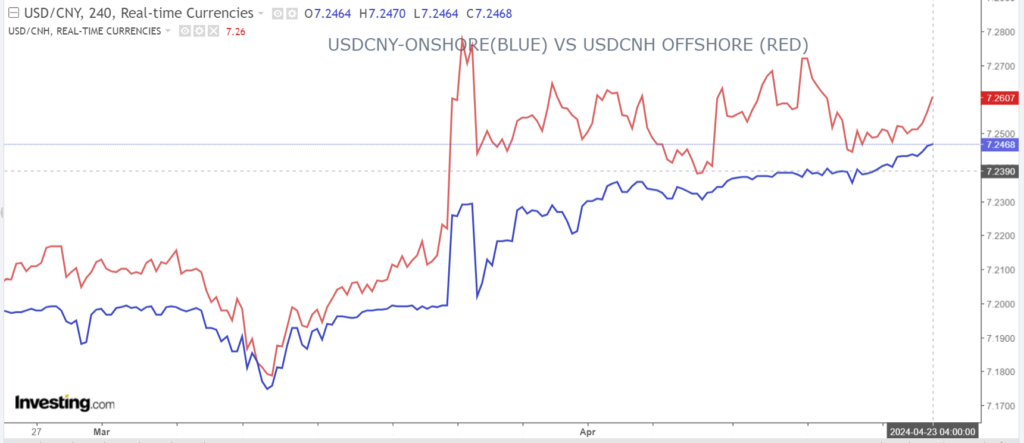

China Snapshot

PBoC fix: 7.1059 forecast 7.2437, (prev. 7.1043).

Shanghai Shenzhen CSI 300 fell 0.70% to 3506.22.

Chinese equity markets lag global markets due to fears that new US sanctions will block access to some Chinese banks to the global financial system, because they helped Russia. China’s exports of goods to Russia that can have a military purpose have surged. US Secretary of State Antony Blinken said is off to China today and he said, “China can’t have it both ways.It can’t purport to want to have positive friendly relations with countries in Europe, and at the same time be fueling the biggest threat to European security since the end of the Cold War.”

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com