Photo: Freepik

March 24, 2023

- EURUSD collapsing from Thursday peak but still above Monday open.

- European PMI data overshadowed by Deutsche Bank stock plunge.

- US dollar rallies overnight but opens mixed for the week.

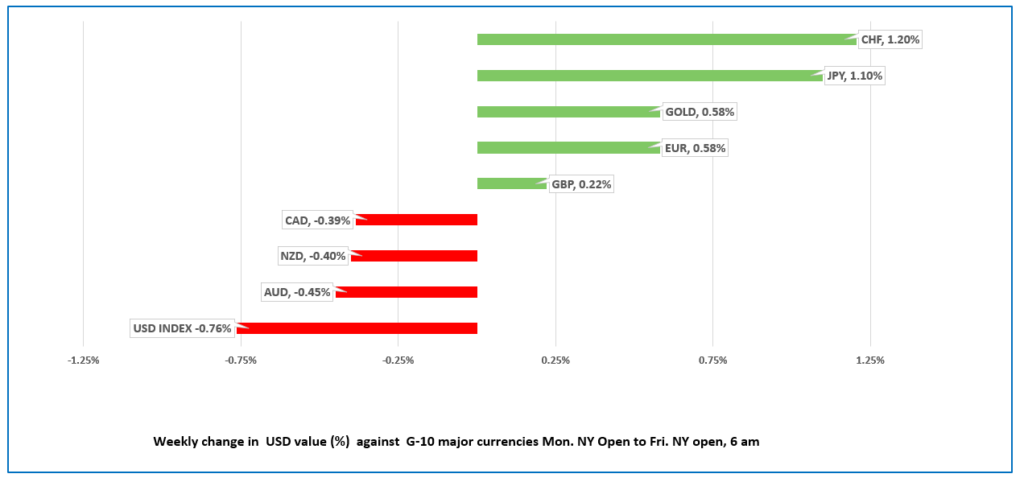

Weekly FX at a glance

Source: IFXA Ltd/RP

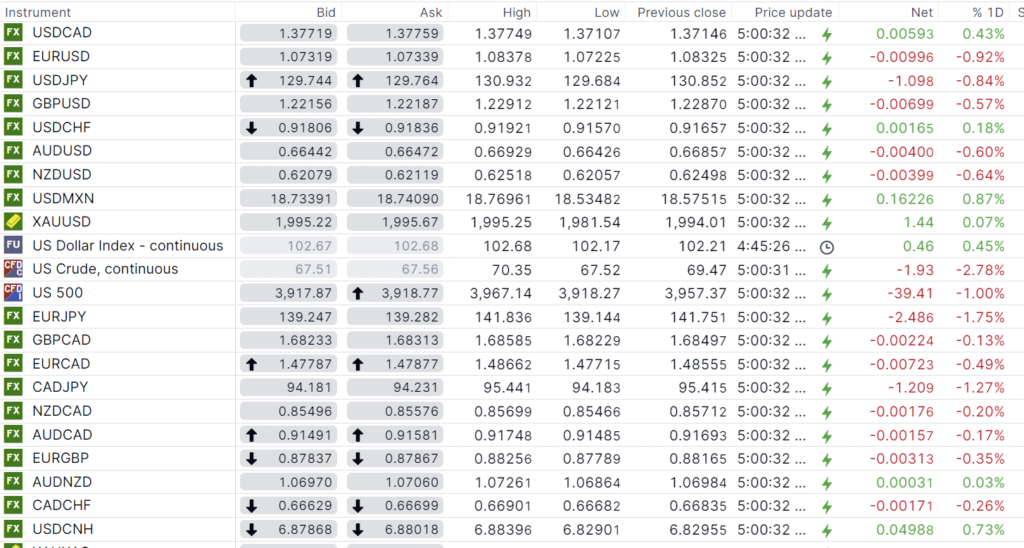

USDCAD Snapshot: open 1.3772-76, overnight range 1.3711-89, close 1.3715

USDCAD continues to bounce between support and resistance and is currently attacking the top end of its range. USDCAD hit 1.3631 yesterday and 1.3789 was paid in early NY trading today with the gains fueled by risk aversion due to European banking jitters.

The drop in the US dollar knocked WTI oil from its overnight peak of $0.35/b down to $66.85/b. The drop is likely due to traders reducing positions ahead of the weekend. Expectations for renewed Chinese demand should limit the downside.

Canada Retail Sales are expected to have risen 0.7% m/m in January compared to 0.5% in December. The focus on global banking worries suggests today’s results will not have any impact on USDCAD trading.

Canada Retail Sales surprised to the upside, rising 1.4% m/m compared to forecasts for a 0.7% gain. Core retail sales, which exclude gasoline stations, fuel vendors and motor vehicle and parts dealers, increased 0.5% in January.

USDCAD Technical Outlook

The intraday USDCAD technicals turned bullish overnight with the break above the 1.3740-1.3760 resistance area, setting the stage for further gains to 1.3850. A break below 1.3700 would negate the upside pressure and shift the focus to the 1.3630 support area.

For today, USDCAD support is at 1.3720 and 1.3690. Resistance is at 1.3790 and 1.3850.

Today’s range 1.3720-1.3820

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Those that believe “there is never just one cockroach” are proving to be rather prescient this morning. It was just yesterday when Swiss National Bank President Thomas Jordan patted himself and his colleagues at FINMA for concocting a solution to the Credit Suisse debacle.

They decided to rank Credit Suisse shareholders above owners of AT-1 bonds, with the latter being wiped out with the UBS takeover.

The Swiss bankers decisions are having a negative impact throughout the European banking system.and investors are jittery.

Deutsche Bank AT-1 bond holders are soiling themselves after Deutsche’s credit default swap (insures against default) prices soared, and the stock price tanked.

EURUSD plunged on the news and safe-haven demand for bonds drove the US 10 year Treasury yield to 3.285%. It was 3.69% on Wednesday.

US Treasury Secretary Janet Yellen needs to put a sock in it. One day she implies that Treasury would guarantee all US bank deposits and the next day she reverses herself. Yesterday she said, “These are tools we could use again for an institution of any size if we judged its failure would pose a systemic risk.”

European equity indexes are in full retreat. The German Dax and French CAC 40 indexes have shed 2.02% while the UK FTSE 100 index dropped 1.90% (as of 6:45 am EDT). S&P 500 futures are down 0.80%.

EURUSD traded negatively falling from 1.0838 in Asia to 1.0722 in early NY due to rising fears around bank stability. Nevertheless, the single currency is still higher than where it opened in NY on Monday. Traders ignored Eurozone PMI data. S&P Global wrote that “Eurozone economic growth accelerated to a ten-month high in March. However, the overall rate of growth remains modest and driven solely by the service sector, with manufacturing suffering a further loss of new orders. EURUSD has minor support at 1.0690, which if broken, will extend losses to 1.0610.

GBPUSD fell to 1.2193 from 1.2291 due to the rising European banking concerns and the flight into safe-haven US dollars. UK Retail Sales ex fuel rose 1.5% m/m in February but were down 3.3% y/y. Both results were at tad better than expected but ignored by FX traders. Bank of England Governor Bailey warned that inflation risks becoming “imbedded” if businesses continue to raise prices.

USDJPY plunged to 129.65 from 130.93 due to the drop in US Treasury yields and safe-haven demand for yen. Japanese inflation data was mixed. Headline CPI rose 3.3% y/y lower than January’s 4.3% y/y result but Core CPI rose from 3.2% y/y in January to 3.5% y/y.

AUDUSD was weighed down by the negative risk sentiment and fell to 0.6627 from 0.6693. Weaker than expected Manufacturing and Services PMI added to the selling pressures.

US Durable Goods Orders fell 1.0% in February, compared with a 0.5% decline in January. Traders ignored the news.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

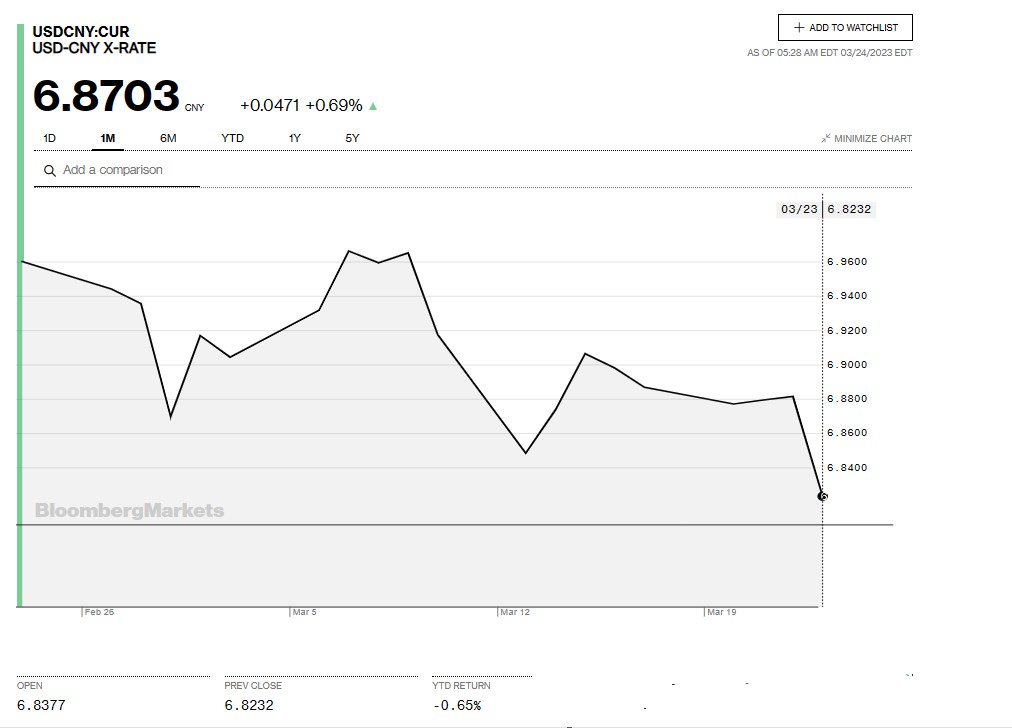

China Snapshot

Bank of China Fix: 6.8374, Previous: 6.8709

Shanghai Shenzhen CSI 300 fell 0.30% to 4027.05.

Chart: USDCNY 1 month

Source: Bloomberg