February 1, 2024

- Fed caution lifts greenback and sinks stocks.

- Bank of England leaves rates unchanged at 5.25%-no surprise.

- US dollar finishes January with gains across the board.

January FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3456-60, overnight range 1.3420-1.3464, close 1.3436.

USDCAD dropped rapidly on the heels of better-than-expected November GDP growth (actual 0.3% m/m vs. forecast 0.1%). The news fueled talk that Canada would avoid a recession, which was encouraged by the 0.3% m/m flash estimate for December GDP. The news also meant that the BoC could be patient with expected rate cuts.

We will hear more about the BoC outlook today when Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers appear before the House Standing Committee. They will deliver the same message as they did at last week’s monetary policy meeting.

The gains evaporated with the cautious tone adopted by Fed Chair Powell and the FOMC. The outlook for US interest rates will continue to dictate USDCAD direction.

WTI oil prices traded in a $75.45-$76.70/b range. Broad US dollar demand helped cap gains, but supply disruption fears limited the downside.

USDCAD Technicals:

The intraday USDCAD technicals are neutral inside a 1.3370-1.3540 range. Yesterday’s failure to decisively breach support in the 1.3360-70 area combined with the subsequent rally above 1.3430 turned the intraday outlook to bullish. Traders are looking for a break above 1.3470 to extend gains to 1.3540. A break below 1.3370 or above 1.3540 risks a 0.0150 point move.

For today, USDCAD support is at 1.3420 and 1.3380. Resistance is at 1.3470 and 1.3510. Today’s range is 1.3390-1.3490.

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

Fed Chair Powell admitted that US rates were headed lower but, on his schedule, not the market’s. That’s not what traders wanted to hear, and they sold stocks and bought US dollars. The negative sentiment continued overnight, and the US dollar added to its post-FOMC gains against the majors. However, the safe-haven currencies, Swiss franc and Japanese yen, squeezed out small gains.

Risk sentiment soured slightly on news that the US launched an attack on Houthi targets in Yemen. In addition, the US is blaming Iran for the latest strife, which could lead to an escalation in Middle East tensions.

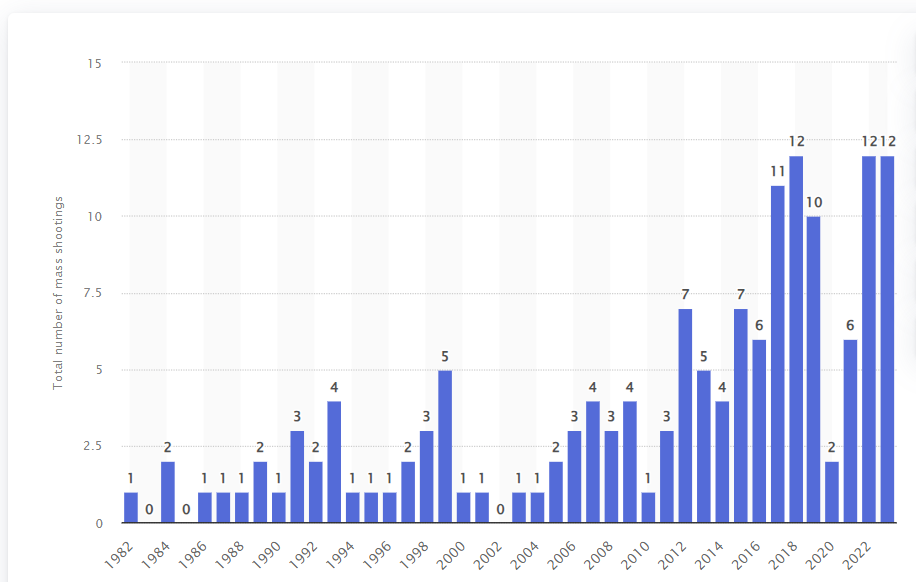

Meta’s Mark Zuckerberg faced a room of angry Senators who blamed Facebook for allowing kids to be sexually exploited online. Senator Lindsay Graham accused Zuckerberg of having blood on his hands, while Missouri Senator Josh Hawley demanded he apologize to families in the room. Both expressed their outrage as they cleaned their AR-15s and cashed NRA lobby checks while reviewing a chart of mass shootings in the US. It’s not Zuckerberg who should be apologizing

Number of mass shootings in US between 1982 and December 2023.

Source: Statista.com

Wall Street closed with losses and the major Asian equity indexes followed suit, except for Chinese ones. European bourses are trading mixed with the UK FTSE posting a 0.47% gain while the German Dax is down 0.20%. S&P 500 futures are up 0.33%.

Bond traders see the world differently. They are content just knowing that the Fed will be cutting rates and they appear less concerned about the timing. The US 10-year Treasury yield dropped from 4.10% on Tuesday to 3.94% today.

EURUSD traded negatively in a 1.0780-1.0822 range. The single currency is suffering from the idea that US interest rates may remain at elevated levels for longer than thought and because of weak Euro area PMI reports. HCOB Eurozone Manufacturing PMI was 46.6, Germany 45.5, and France 48.5. All are in contraction territory which compares poorly with the robust US economy. However, mixed Eurozone inflation data gave the single currency a little support. Eurozone Core CPI rose 3.3% y/y compared to the forecast of 3.2%. The EURUSD technicals are bearish below 1.0880 with a break below 1.0770 extending losses to 1.0705.

GBPUSD is chopping about in a 1.2626-1.2698 range as traders react to Bank of England Governor Bailey’s press conference. Mr Baily gave hopes to those looking for early rate cuts when he said “We don’t need to say inflation back at the 2% target before cutting interest rates, just more confidence that it is heading there sustainably.” The BoE left rates unchanged at 5.25%, as expected, but the Committee was far from united. Two members wanted to raise rates and one member wanted to cut them. The Governor and five others voted for unchanged.

USDJPY is consolidating yesterday’s losses in a 146.47-147.09 range. Prices are weighed down by the drop in the US 10-year Treasury yield and by expectations that US interest rates will be cut at some time in the near future.

AUDUSD traded lower in a 0.6508-0.6579 range. It is the worst-performing currency against the US dollar since yesterday’s open and the second-worst currency since the January 2 open. Weak Australian data including Building Permits, Business Confidence, and soft commodity prices didn’t help.

US ISM PMI data, Challenger Job cuts, and weekly jobless claims are ahead.

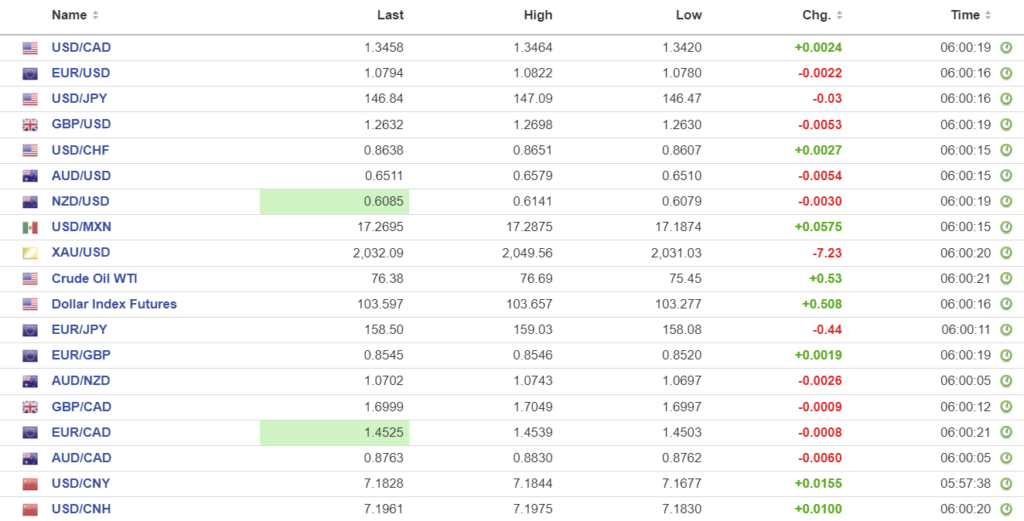

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1049, expected 7.1802, previous 7.1039.

Shanghai Shenzhen CSI 300 rose 0.07% to 3217.31.

Caixin January Manufacturing PMI-final, 50.8 (forecast 50.6)

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com