August 5, 2024

- Equity markets have stopped the bleeding-for now.

- RBA delivers a “hawkish” hold.

- US dollar is trading mixed-JPY outperforms while MXN lags.

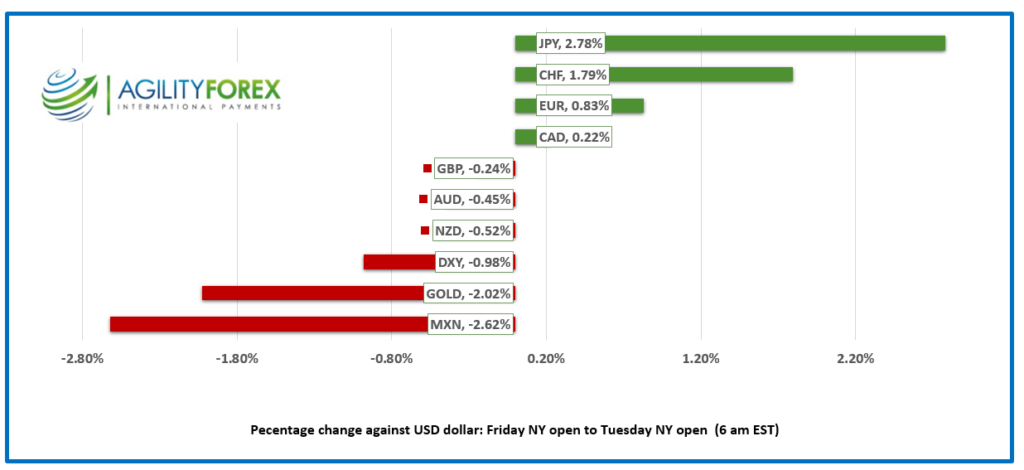

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3845, overnight and Monday range 1.3793-1.3947, Aug. 2 close 1.3874

USDCAD dipsy-doodled along with the rest of the G-10 currencies and started today’s session and is trading a tad weaker than where it closed Friday and yesterday. That is not because the loonie is anything special but because traders are seeing a glimmer of optimism in the cloud of negativity. The speculation of an inter-meeting Fed rate cut or the possibility of a 50 bp rate cut at the September meeting have sparked a narrowing of CAD/US 10-year interest rate differentials.

WTI oil prices traded in a 72.86-74.56 range overnight and are sitting at 73.41 in NY. Prices have dropped steadily since the beginning of June and even rising Middle East tensions failed to stem the slide. Traders fear oil markets will be oversupplied when Opec increases production in October even as the Chinese economy struggles to grow.

US and Canada trade reports are due today, but it is equity market performance that will determine USDCAD direction.

USDCAD Technicals

USDCAD tested intraday support in the 1.3790 area, and it held. Prices then rallied and are looking to break above minor resistance in the 1.3850 are to retest yesterday’s peak. The hourly RSI’s suggest gains may be difficult as USDCAD is still overbought.

The daily chart is bullish with RSI’s in neutral territory. The break above resistance in the 1.3780-90 zone and the USDCAD retreat from 1.3950 suggests a period of 1.3780-1.395 consolidation is likely, inside the broader 1.3590-1.3950 range.

For today, USDCAD support is at 1.3810 and 1.3780. Resistance is at 1.3850 and 1.3900. Today’s Range 1.3810-1.3890

Chart: USDCAD daily

Source: DailyFX

Meltdown

Summer markets have a nasty reputation for outsized moves sparked by dubious catalysts and exaggerated by poor liquidity due to holidays. Friday was a textbook example. The US nonfarm payrolls headline number rose far less than expected, wreaking havoc across all asset classes after Wall Street indexes fell through the floor. Any near-term hope that calm would return to markets vanished on Monday with the weekend news that Warren Buffett bailed on a huge chunk of his Apple holdings. The Nasdaq closed with a 3.47% loss, still leaving the tech index up 9.6% YTD, as of yesterday’s close. The stampede into safe-haven assets was evident, with the 10-year Treasury yield dropping from 3.97% to 3.65% before a bounce to 3.84%. The US dollar index (DXY) dropped from 103.85 pre-NFP to 101.97 yesterday before rebounding to 102.91 overnight.

Autopsy

The Friday-Monday market meltdown was due to a combination of factors but exacerbated by the poor liquidity environment typical of summer markets. This year, the markets may have been thinner than usual due to the Paris Olympics, the Northern Hemisphere heatwave, and the US presidential race sidelining traders.

Markets started to bounce back in Asia overnight, but it is yet to be determined if the bounce is of the dead cat variety. Traders may be reassessing the doom and gloom scenarios and concluding the sell-off was overdone. Scotiabank Capital Markets Economics Chief Derek Holt argues the market wildly over-reacted to the NFP data. He pointed out that the results are still being distorted by the pandemic fallout. Furthermore, he says that Friday’s NFP result was a tad better than the pre-pandemic norm.

Rebound

Tuesday’s Asia session saw Japan’s Topix soar 9.30% to 2,434.21 after closing at 2,215.15 the day before. Analysts suggest the panic selling has run out of steam. European bourses are still bleeding red ink. The French CAC is down 0.55%, while the UK FTSE 100 index is close to unchanged at -0.6%. S&P 500 futures have rallied 0.53% this morning but still have a long way to go to recuperate Monday’s 3.00% loss.

Risk sentiment started improving as traders digested numerous commentaries suggesting that the equity sell-off was overdone. Jefferies and Company predicted that the weak US labor market would spur the Fed to cut rates before the scheduled September meeting. Perhaps, but by doing so, the FOMC would be admitting they were wrong—again. The Wall Street Journal’s Nick Timiraos writes that if the Fed sees further evidence that the labor market is slowing, they may cut rates by 50 bps in September.

EURUSD

EURUSD is trading just above the low of its overnight 1.0907-1.0963 range and continues to consolidate Friday’s gains, where it surged from a pre-FOMC level of 1.0822 to 1.1008 yesterday. Equity market volatility overshadowed mixed to better-than-expected German and Eurozone Composite PMI data and a weaker-than-expected Eurozone Retail Sales report today (actual -0.3% m/m vs forecast -0.1% and May 0.1%). Narrowing ECB/US interest rate differentials and bullish EURUSD technicals following the break above 1.0870 are supporting prices.

GBPUSD

GBPUSD mirrored EURUSD moves and traded in a 1.2700-1.2817 range since Monday. Slightly better-than-expected services PMI yesterday (actual 52.5 vs forecast 52.4) and a forecast-topping Construction PMI report today (actual 55.3 vs forecast 52.7) only managed to slow the downward slide from EURGBP buying to unwind carry trades. A move below 1.2690 targets 1.2480.

USDJPY

USDJPY is trading at 144.85 in early NY after a wild couple of days. It was trounced in the wake of the disappointing NFP report then plummeted from 146.67 to 141.69 yesterday and 143.62-146.37 overnight. Ongoing carry trade unwinding and the global risk aversion from the equity market meltdown are driving price action.

AUDUSD and NZDUSD

AUDUSD plunged to 0.6351 yesterday before rallying to 0.6541 after the Reserve Bank of Australia (RBA) left rates unchanged at 4.35% but issued a hawkish message. Policymakers are concerned about inflation, which they claim is not only too high but also not showing any signs of improvement in the near term. Governor Michele Bullock said that traders betting on a near-term rate cut “were getting a little bit ahead of themselves.”

NZDUSD traded choppily in a 0.5850-0.5980 range and is sitting at 0.5920 in NY.

USDMXN

USDMXN soared, swooned, then inched higher inside a 19.1388-19.8400 range. The peso is battered by fears that a US soft landing may not be as soft as originally expected in addition to carry trade unwinding.

Bitcoin (BTCUSD)

BTCUSD was not immune to fiat currency volatility or a jump in global risk aversion. BTCUSD plunged from Friday’s peak of 63,341 to 49,684 overnight before bouncing to 54,960 in NY

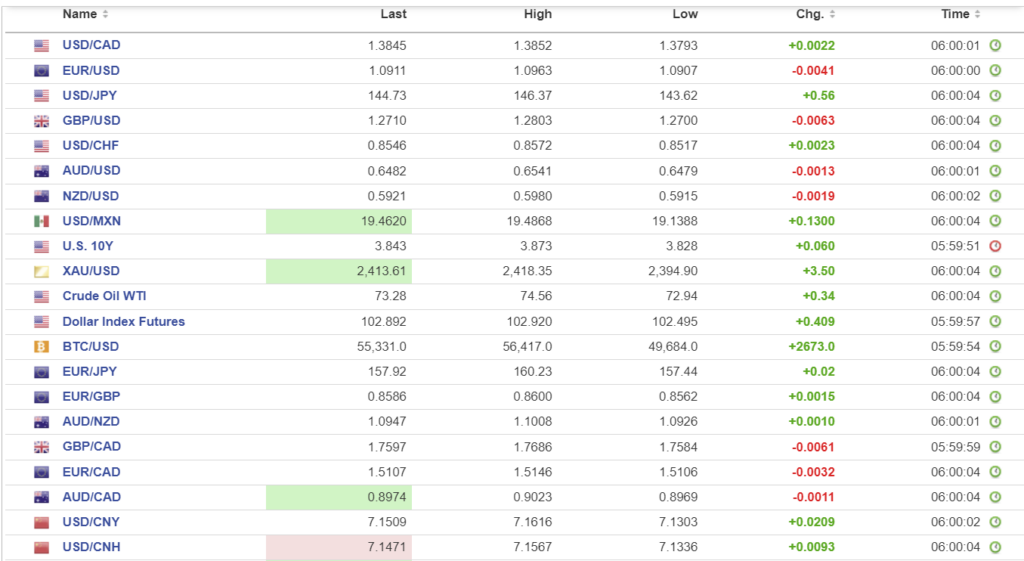

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

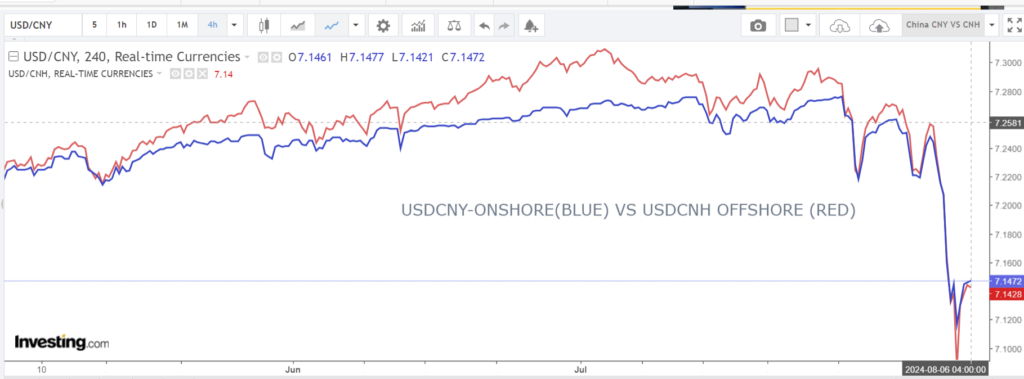

China Snapshot

PBoC fix: 7.1318 vs exp. 7.1454 (prev. 7.1345).

Shanghai Shenzhen CSI 300 fell 0.34% to 3342.98

July Caixin Serves PMI 52.1 (forecast 51.4, June, 51.2)

Chart: USDCNY and USDCNH

Source: Investing.com