January 17, 2020

USDCAD open (1.3040-44) 6:00 am EST) Overnight Range (1.3036-1.3056)

Fed Chair Jerome Powell has repeatedly described the US economy as being in a “good place.” It still is according to today’s December Housing Starts report and yesterday’s Retail Sales data.

There was a risk-on party in global equity markets overnight, but FX markets couldn’t get past the bouncer at the door. The Wall Street rally yesterday continued into Asia and European markets overnight. Gold and oil prices inched higher as did the US dollar, albeit marginally.

The US dollar opened in New York with small gains against the major G-10 currencies but essentially unchanged against the commodity bloc.

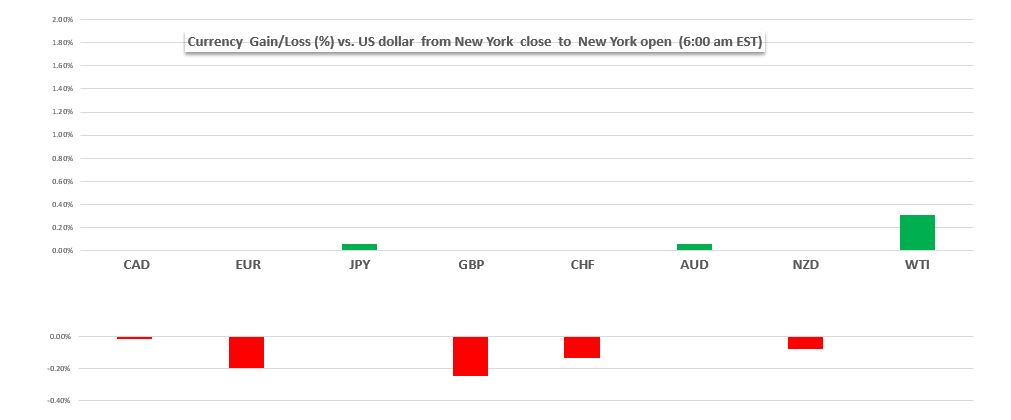

FX overnight snapshot

Source: Saxo Bank/IFXA Ltd

This week’s rally in GBPUSD ended abruptly just before New York opened. GBPUSD plunged from 1.3118, just before Europe opened to 1.3032 in early New York trading after an ugly retail sales report. December retail sales fell 0.6% m/m rather than rise 0.7% m/m as forecast. That news, combined with dovish comments from many Bank of England officials raised the odds for a January 30 rate cut. The intraday technicals are bearish with the break below 1.3040 suggesting further losses to 1.2950.

EURUSD followed Sterling lower. The single currency dropped from an overnight peak of 1.1141 to 1.1110 in New York. Eurozone inflation at 1.3% y/y for headline and core, underscored the ECB’s dovish outlook.

USDJPY traded in a 110.12-110.28 range overnight, seemingly reluctant to stray far from the 110.00 area. Prices are supported by a tick higher in US Treasury yields, news of a new US 20-year bond, and the unwinding of pre-trade deal safe-haven trades.

AUDUSD and NZDUSD dipsy-doodled alongside the release of China GDP data which was as expected at 6.0%. China Retail Sales beat expectations which led to USDNY closing well below the official fixing rate. The theory seems to be that the Antipodean currencies are not getting much support from the Phase 1 Trade deal because the tariffs are still in place. Also, AUDUSD gains are limited by speculation of Reserve Bank of Australia rate cuts and economic damage from the wildfires.

WTI oil prices are consolidating gains that took prices from $57.60/barrel to $58.89/b overnight. Prices are supported by the ongoing Opec/Russia crude production cuts and Iran/US tensions. However, forecasts suggesting oil supply will exceed demand in H1 2020, and concerns that existing US/China tariffs will impede global growth are limiting gains.

USDCAD is stuck in a 1.3030-50 range. Broad US dollar demand is being offset, to a degree by a rebound in oil prices. Traders do not seem to want to get too involved ahead of the US long weekend and the Bank of Canada monetary policy meeting on Wednesday.

Today’s US data includes December Building Permits, Housing Starts, Michigan consumer Sentiment, Industrial Production and Capacity Utilization. The results should confirm that the American economy is chugging along nicely which will support Wall Street and the greenback. There are three Fed speakers on tap today, who will likely parrot the “economy is in a good place” mantra.

The US market is closed on Monday for Martin Luther King Day. Since the dollar is down across the board compared to Monday and today’s New York open, (except against JPY and AUD) it suggests the dollar could see a position-squaring, profit-taking rally today.

USDCAD Technical Outlook

The USDCAD technicals are bearish. The downtrend line from December 2, at 1.3315 is intact while prices are below the 1.3070 area, suggesting further losses to 1.2950. If 1.2950 breaks, losses could extend to 1.2810. A decisive break above 1.3070, targets 1.3190. For today, USDCAD support is at 1.3030 and 1.2990. Resistance is at 1.3070 and 1.3110. Today’s Range 1.3020-70

Chart: USDCAD daily

Source: Saxo Bank