Photo: Globalnews

- Risk sentiment turns from mildly positive to mildly negative after US data

- US November PPI rose 0.3% m/m (forecast 0.1%)

- US dollar traded defensively, rallied post-PPI

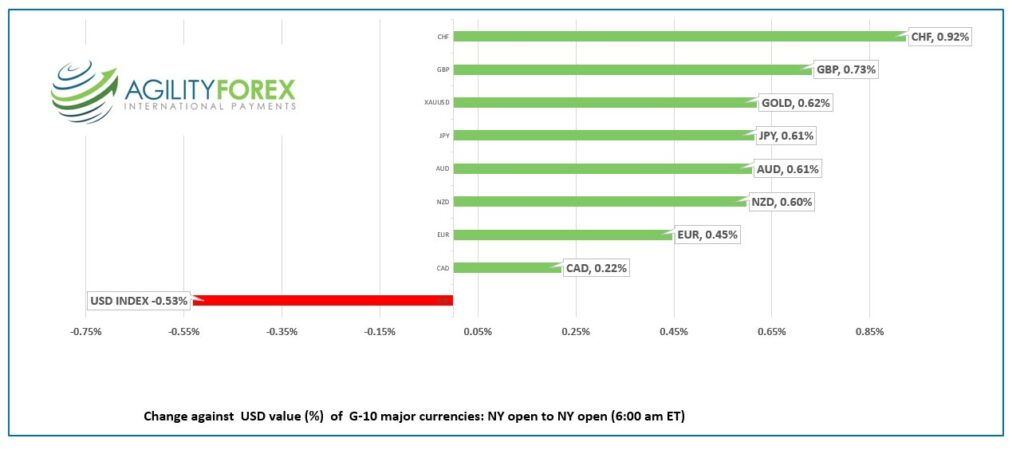

FX at a glance:

Source: IFXA Ltd/RP

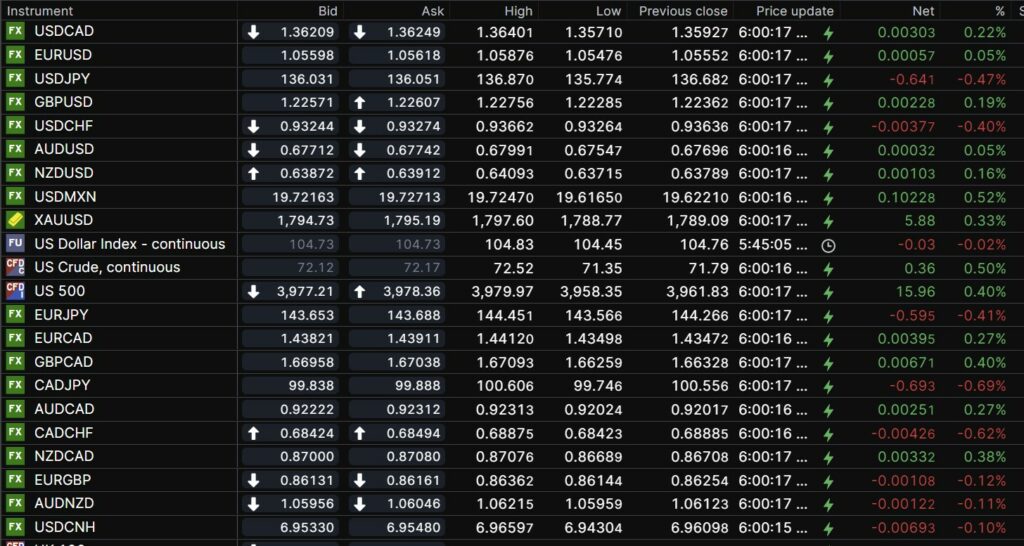

USDCAD Snapshot: open 1.3621-25, overnight range 1.3571-1.3690, close 1.3593

USDCAD dropped from 1.3690 In European trading yesterday to 1.3561 by mid-morning on the back of modestly improved risks sentiment spurred by the rising stocks on Wall Street. Markets were also perky due to increased popularity of the theme that the Fed is very close to its terminal rate, which if true makes stocks attractive and undermines the US dollar.

The magnitude of the USDCAD decline was exacerbated by stop loss selling in thin markets.

Evidence of thin markets was on full display immediately following the US November PPI data, whine USDCAD spiked to 1.3690 from 1.3610.

Yesterday, BoC Deputy Governor Sharon Kozicki explained the decision to raise rates by 50 bps saying, “the economy remains in excess demand, inflation is still too high and broadly based, and short-term inflation expectations remain elevated.”

Looking forward, Ms Kozicki said the BoC will be considering whether to raise rates further, but decisions will be more data-dependent.” That implies Wednesday’s decision wasn’t determined by economic data but by something else. Hmm, coin toss, drinking game?

USDCAD technical outlook.

The USDCAD intraday technicals are bullish while trading above 1.3430, the uptrend line from November 15, which is guarded by minor support in the 1.3550-60 area. A move below 1.3550 suggests further losses to 1.3430, while a decisive move above 1.3690 targets 1.3750

For today, USDCAD support is at 1.3620 and 1.3570. Resistance is at 1.3690 and 1.3750

Today’s range 1.3620-1.3690

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Financial markets are in the eye of the storm. Many traders are in pubs, Christmas shopping, or otherwise occupied, either awaiting next week’s US inflation data and the sermons from the mount-Mount Fed, Mount ECB, and Mount BoE.

That changed in the wake of the hotter-than-expected US November PPI data, which threw a wet blanket on speculation that the Fed will pivot after fed funds reach the terminal level.

The US Bureau of Labor wrote, “The Producer Price Index for final demand advanced 0.3 percent in November, seasonally adjusted. Final demand prices also rose 0.3 percent in both October and September.

S&P 500 futures plummeted to 3928.60 from 3986.97 before scratching back to 3945. The US 10-year yield jumped to 3.51% from 3.469% and the US dollar rose against the G-10 majors. Those moves are already retracing.

WTI oil prices got a minor boost yesterday following news that a TC pipeline heading for Cushing Oklahoma sprung a leak. The gains were temporary and WTI dropped from $75.37/b yesterday to $71.35/b just before NY opened. Prices bounced to $72.80/b after the PPI data.

EURUSD traded in a 1.0504-1.0588 band and is in the middle of that range. (6:00 am PT). Prices continue to be supported by expectations for a hawkish ECB meeting result next week, and optimism surrounding China covid-zero policy relaxation. The intraday EURUSD technicals are bullish above 1.0500 but face strong resistance at 1.0600. A move below 1.0540 will target 1.0480.

GBPUSD traded in a 1.2206-1.2276 range supported by a minor uptrend at 1.2190, with the low achieved post-PPI. Traders are awaiting the release of the quarterly Inflation Report which is expected to show inflation expectations have risen. The BoE is expected to hike rates by 50 bps at next Thursday’s meeting.

USDJPY traded defensively in a 135.69- 136.87 range overnight before spiking to 136.60 after the US data. Prices have since retreated to 136.05 and are weighed down by speculation the BoJ may end its yield curve control (YCC) policy in 2023.

AUDUSD climbed from 0.6745 to 0.6799 due to the weak US dollar and optimism around China’s relaxation of covid-zero protocols.

Michigan Consumer Sentiment (forecast 53.3) is ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

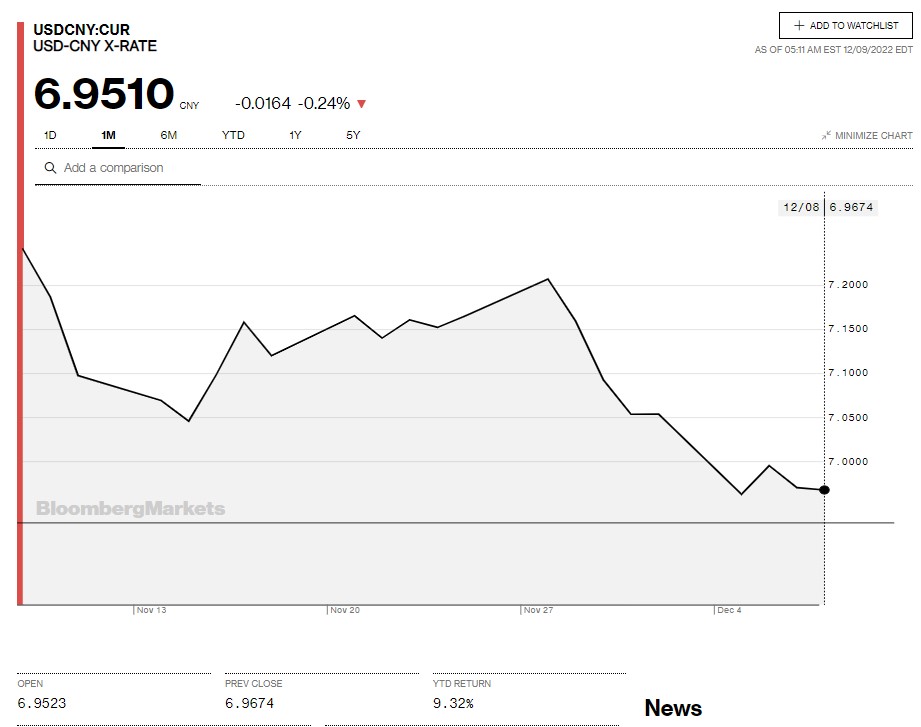

Today’s Bank of China Fix: 6.9588, previous 6.9606

Shanghai Shenzhen CSI 300 rose 0.99% to 3998.24

November CPI 1.6% y/y (forecast 1.0%, October 2.1% y/y)

November PPI -1.3% y/y (forecast -1.5%, October -1.3% y/y)

Chart: USDCNY 1 month

Source: Bloomberg