January 19, 2024

- Canada Retail Sales were weaker than expected in November.

- Robust data pushing Fed rate cuts back.

- US dollar consolidating this week’s gains.

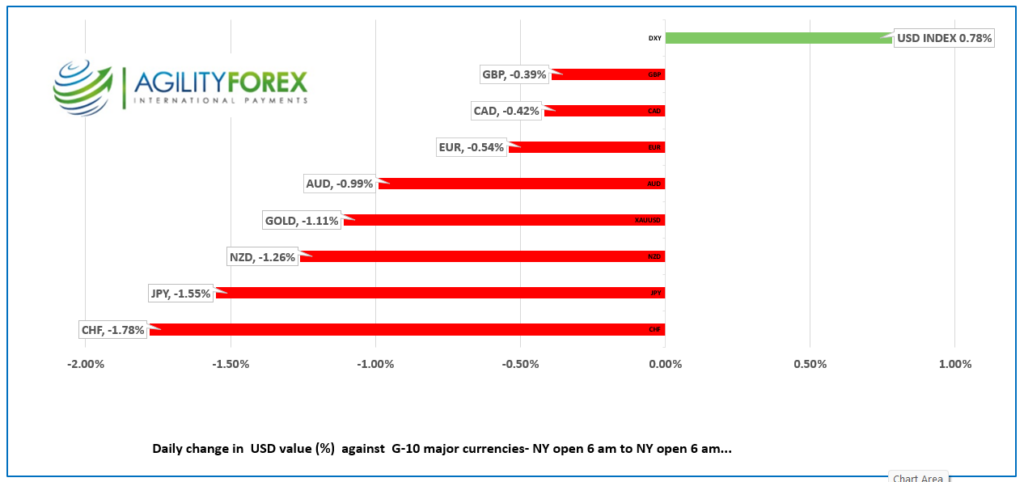

Weekly FX at a glance-Monday-Friday NY open

Source: IFXA

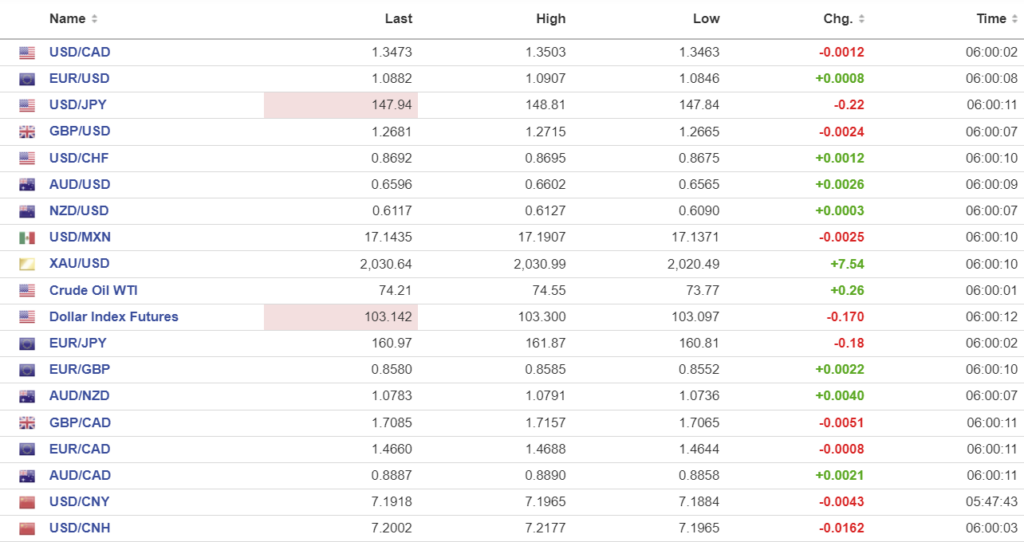

USDCAD Snapshot: open 1.3471-75, overnight range 1.3455-1.3503, close 1.3489.

USDCAD is looking like it will finish the week as the second best performing G-10 currency against the US dollar. Today’s November retail sales report isn’t likely to have a lasting impact because not only is the data stale, but traders are also focused on the US interest rate outlook and that is what is driving USDCAD moves.

Canada retail sales fell 0.2% m/m in November compared to the downwardly revised 0.% m/m in October. Excluding auto’s the November decline was 0.5% m/m. October’s number was downgraded to 0.4% from 0.6%. The results are further evidence that consumers are feeling the pinch from high interest rates.

The result should limit USDCAD downside as it could encourage the BoC to lower rates but realistically, it is the outlook for Fed rates that is driving the currency pair.

WTI oil prices retreated to $73.72 to $74.55 due to the overnight US dollar selling pressure. Concerns about supply disruptions are offset by slow Chinese economic growth.

USDCAD Technicals:

The USDCAD technicals are bearish. The downtrend from November is guiding prices lower while 1.3540 caps the topside. A daily close below the 100 day moving average (1.3480) suggests further downside towards the 200 day moving average at 1.3378. It won’t be a one-way street as USDCAD has support at 1.3450 which is the 38% Fibonacci retracement level of the November-January range.

For today, USDCAD support is at 1.3450 and 1.3420. Resistance is at 1.3510 and 1.3540. Todays range 1.3460-1.3520

Chart: USDCAD daily

Source: DailyFX

G-10 FX recap

“The best-laid plans go awry.” Renowned Scottish poet Robbie Burns wrote those words in 1785, but traders positioned for a Fed rate cut on March 20 have been muttering them since the beginning of the year. Why wait for Robbie Burns Day on January 25?

The odds for the FOMC to cut rates to 5.25% dropped from 77% on January 12 to 53.8% today, following a series of robust US economic reports, including yesterday’s weekly jobless claims data. The US dollar has had a good week and is poised to finish with gains across the board, led by a 1.8% drop in the Swiss franc.

FX markets were somewhat subdued, but that could change this morning with the release of the US Michigan Consumer Sentiment Index and the Consumer Inflation Expectations report.

Asian equity markets closed higher, led by a 1.40% gain in Japan’s Nikkei 225 index and a 1.02% rise in Australia’s ASX 200. China and Hong Kong markets lost ground. European bourses opened in positive territory and extended gains with the UK FTSE 100 index gaining 0.42%. Wall Street is looking perky, with S&P 500 futures up 0.44%. The 10-year US Treasury yield is steady at 4.15%.

EURUSD drifted in 1.0868-1.0895 range Softer than forecast German Producer Prices data in December (actual -1.2% m/m vs forecast -0.5%) drove the single currency to its low before profit taking helped recoup the losses. ECB President is concerned about a Trump victory and said the best defence is having a strong deep domestic market. The ECB monetary policy meeting is next Thursday.

GBPUSD bounced in a 1.2665-1.2715 band and appears to have shrugged off a weak December retail sales report which was the worse since Covid in January 2021. (-3.2% m/m vs November 1.4%).

USDJPY weakened to 148.84 from 148.81 after Japanese inflation data for December remained low which eased pressure for the Bank of Japan to tighten policy. Prices have since moved higher to 148.16 on the back of the US 10-year Treasury yield rising to 4.15%.

AUDUSD drifted higher in a 0.6565 to 0.6602 range thanks to higher commodity prices and modestly improved risk sentiment.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1167, expected 7.1972, previous 7.1174.

Shanghai Shenzhen CSI 300 fell 0.15% to 3269.78.

Chart: USDCNY and USDCNH daily

Source: Investing.com