By Michael O’Neill

There has never been a president quite like the fellow occupying the White House, today. Many pray that there never will be again. But that is a moot point. Donald Trump is the 45th President of the United States and will be until he is impeached, resigns, or loses the November 2020 election.

To the American military, he is the Commander-in-Chief, the man in charge of the armed forces and the massive military arsenal. Even scarier, his ego is a big as the military arsenal he commands. And he has the nuclear codes.

None of the above will come as a surprise to anyone with a pulse which explains why FX markets and markets, in general, react to his “tweets’, his speeches, press conferences or interviews.

President Trump and Kim Jong-un of North Korea have been loggerheads for the past month. North Korea keeps launching missiles and threatening the United States (as well as Guam and Japan) while the US and South Korea antagonize North Korea by holding massive war games on their border.

Three weeks ago, President Trump responded to a North Korea threat to Guam, promising “fire and fury” like the world has never seen.” On August 28, Kim Jong-un launched a ballistic missile that flew over Northern Japan.

FX traders shifted into risk aversion mode and bought Japanese yen and Swiss francs as they are the “safe-haven currencies.

President Trump’s first reaction was to act “presidential.” He told Japan that America was behind them 100% and warned Pyongyang that “all options were on the table.”

Trump’s reaction caught FX traders (and probably everyone else) by surprise. In response, the safe-haven trades were unwound.

It was too good to last. On August 30, Mr. Trump sounded threatening, again. He tweeted “the U.S. has been talking to North Korea, and paying them extortion money, for 25 years. Talking is not the answer!”

This time, FX markets yawned. President Trump became the “boy who cried wolf”

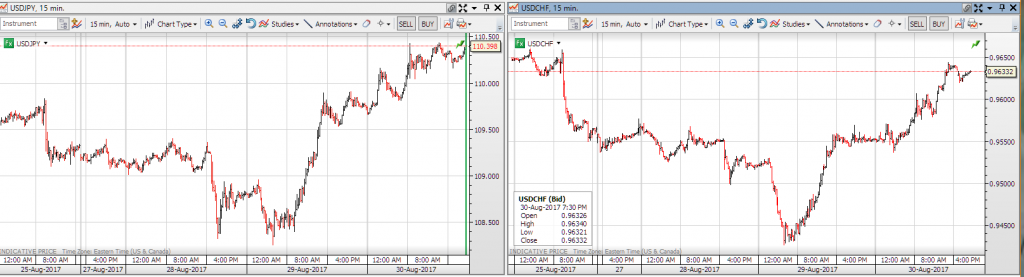

The following chart shows the fifteen-minute ebb and flow of risk aversion for the two most popular safe-haven currencies. These wide price swings were not just because of Trump’s comments, but he was a large part of them.

Chart: USDJPY and USDCHF-15 minute price moves August 25-August 30

Mr. Trump and his comments had destabilized FX markets even before he took the oath of office. He might be the biggest culprit sparking safe-haven trades, but he is far from being the only destabilizing influence.

Fed Chair Janet Yellen and European Central Bank President Mario Draghi have taken turns roiling FX and other markets.

The Kansas City Federal Reserve’s Annual Jackson Hole Symposium is a closely watched gathering because central bankers have used the venue to announce major policy shifts. Some traders worked themselves into a lather ahead of the August 24-26, 2017 meeting because of scheduled speeches by Fed chair Janet Yellen and European Central Bank (ECB) President Mario Draghi.

Markets were looking to Janet Yellen to provide a little clarity on US monetary policy, something that had been lacking since the June 14 meeting, press conference and updated projections. They didn’t get anything. Ms. Yellen did not talk about monetary policy in her speech.

A similar let-down occurred with Mario Draghi’s speech. Many were expecting him to talk about tapering the quantitative easing program. He didn’t.

Traders expected too much from Yellen and Draghi’s Jackson Hole speeches. Source: Google images

Traders were annoyed and expressed their annoyance by selling US dollars. The move worsened due to a bout of risk aversion, and concerns about the impact of Hurricane Harvey on the US economy.

But that was then; this is now.

A common theme, evident this week, is the transient nature of FX moves due to risk. These risks include; fears and concerns associated with inflammatory rhetoric in Trump tweets, terrorist attacks, geopolitical sabre-rattling and natural disasters. The reactions can be exaggerated when those events occur during liquidity-challenged, summer markets.

Although the impact of top-tier economic data reports can be diminished in the summer, data released near the end of August should not be ignored. This information will be fresh in the minds of policy makers when their monetary policy meetings occur.

Recent US data including the 3.7% jump in Q2 GDP, reaffirmed the strength of the economy. Fed officials have said time and time again, that interest rate decisions are data dependent. Still, markets do not expect a rate increase until December, and even then the odds are just 30.9%, as per the CME Fedwatch tool.

Major economic data still trumps Trump. On August 31, Canada posted a rip-roaring 4.5% rise in Q2 GDP. That data led to a steep drop in USDCAD and refocused attention on the prospect of another Bank of Canadian rate increase, which could occur as soon as September 6.

Central bank policies are the most important drivers of a currencies direction. The bankers get their guidance from economic data, and develop very long term outlooks.

In contrast, FX traders have much shorter horizons. The forward-looking nature of the job means that they have to react to headlines, tweets, or any event that they believe could impact how a central banker perceives the direction of monetary policy.

Arguably, traders are getting wise to President Trump as nothing seems to come from his inflammatory comments or tweets. He is all bark and no bite.

In the Royal Court of Foreign Exchange, the central bankers are the Kings and Queens, and President Trump is the Joker. And like all jokers, he shouldn’t be taken seriously.