Source: Rachel Mans McKenny/Penguin Random HOuse

- Risk sentiment improves as the US 10-year Treasury yield retreats

- BoC Business Outlook Survey fuels forecast for 75 bp hike next week

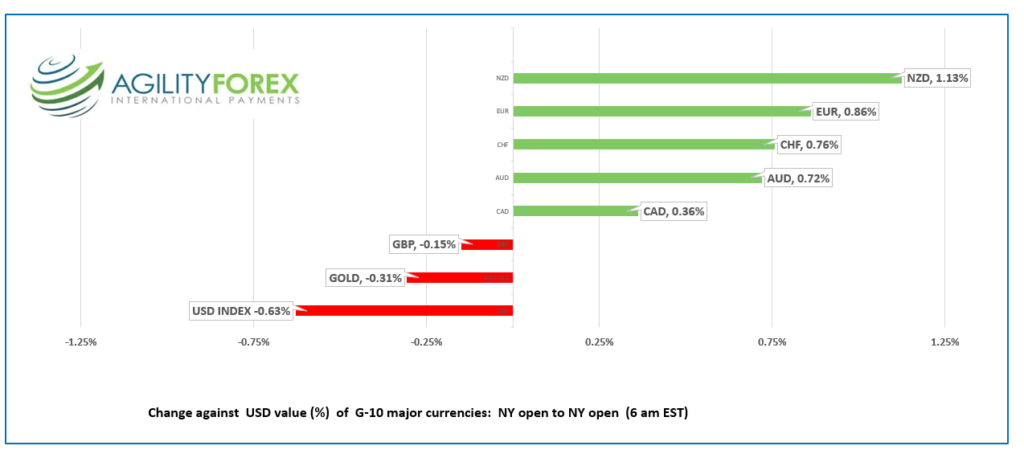

- US dollar retreats, NZD outperforms

FX at a glance:

Source: IFXA Ltd/RP

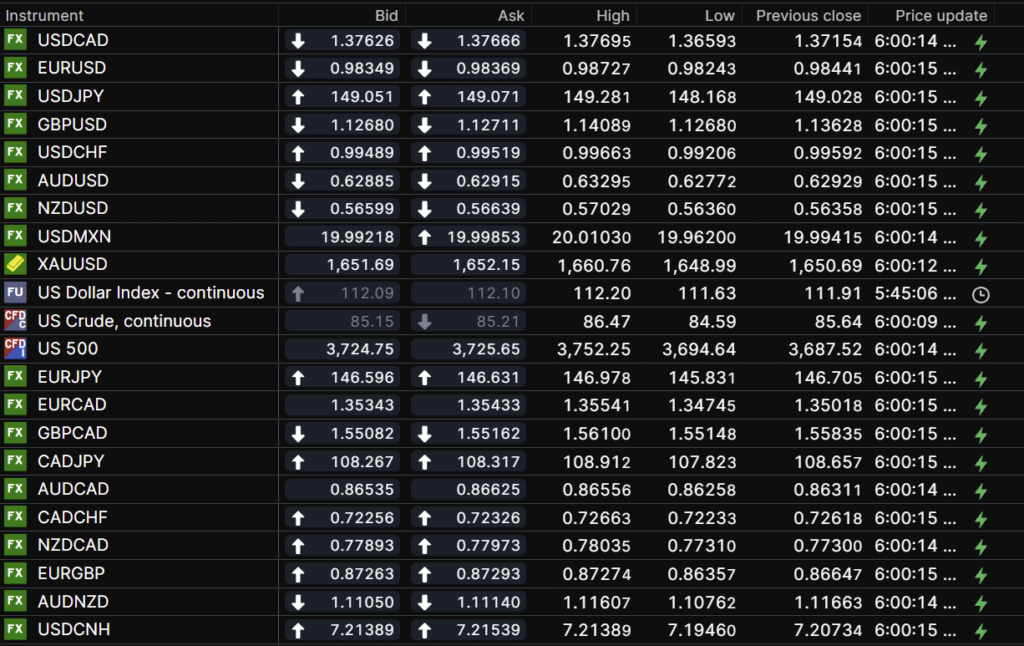

USDCAD Snapshot: open 1.3762-66, overnight range 1.3659-1.3770, close 1.3715

USDCAD dropped from 1.3815 at Monday’s NY open to 1.3700 in the wake of the Bank of Canada (BoC) Business Outlook Survey (BOS). The survey did not paint a pretty picture.

The survey noted “Business confidence has softened. Many firms expect slower sales growth as interest rates rise and demand growth shifts closer to pre-pandemic levels. Early signs suggest that pressures on prices and wages have started to ease, but firms’ inflation expectations remain high.

The results led JPMorgan to raise its October 26 rate hike forecast to 75 bps from 50 bps.

Source: Bank of Canada BOS

Yesterday’s USDCAD price action is a “chicken or an egg” dilemma as it occurred as the S&P 500 index propelled itself to a 2.65% gain. However, it is more than likely that the USDCAD losses were due to the S&P 500’s rally.

WTI oil chopped about in a $84.59-$86.47 range. The Biden Administration is planning to release another 10-15 million/barrels from the Strategic Petroleum Reserves this week, to help counter the Opec production cut that takes effect November 1. WTI gains are hampered by slowing global growth concerns.

Canada housing starts were better than expected rising 299,600 (forecast 263,000)

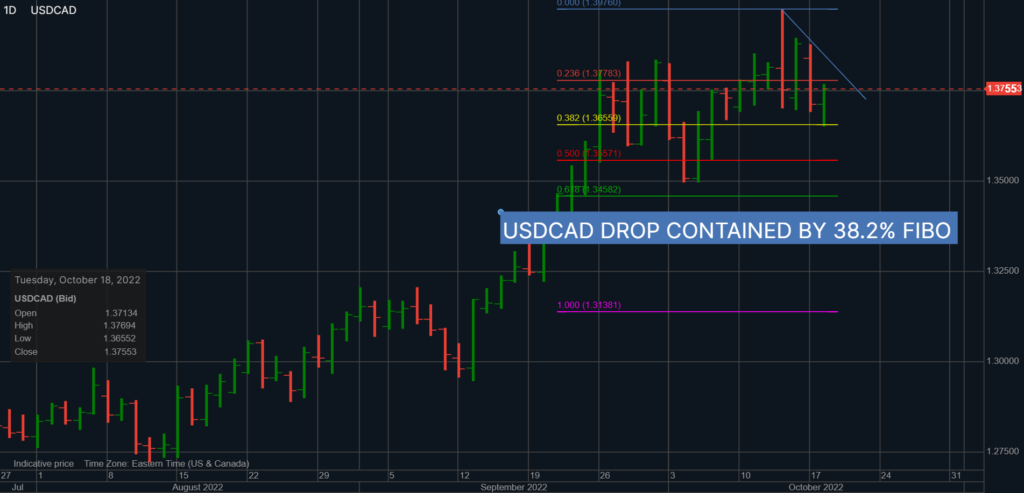

USDCAD Technical outlook

The intraday technicals are bearish below 1.3770, with the move below 1.3730 snapping the uptrend line from the middle of September. The follow-through decline halted at 1.3659 overnight, just above the 38.2% Fibonacci retracement level (1.3655) of the Sept.13 rally. The subsequent rally stalled at the 23.6% level and just below the intraday downtrend from October 14. A decisive break above 1.3780 would negate the downside pressure and target 1.3900. A decisive break below 1.3650 suggests further losses to the 61.8% Fibo level of 1.3440.

For today, USDCAD support is at 1.3690 and 1.3650. Resistance is at 1.3780 and 1.3830. Today’s range: 1.3690-1.3770

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The Butterfly effect is a phenomenon whereby a minute change in a complex system can have large effects elsewhere. The Kwasi Kwarteng effect has similar traits. The Kwarteng/Truss budget wreaked havoc across UK financial markets and contagion fears spread to global bonds, equities, and the US dollar.

The new Chancellor of the Exchequer Jeremy Hunt scrapped the Kwarteng budget, and the universe was back in balance.

Wall Street closed with impressive gains and S&P 500 futures which have gained 2.0% in early NY trading, powered by the 10-year Treasury yield sliding from 4.04% overnight to 3.97% in NY.

EURUSD consolidated yesterday’s gains in a 0.9814-0.9873 range. Prices may have received a bit of support after the German ZEW Economic Sentiment rose by 2.7 points to 59.2. However, the assessment of the economic situation deteriorated.

GBPUSD traded in a 1.1257-1.1409 range. Prices peaked in Asia then plunged in Europe and found a bottom in NY. Prices have rebounded to 1.1342 in the wake of sharply higher US equity futures. The gains were due to a FT report citing “officials” that claimed the BoE would delay its Quantitative Tightening program until the end of October. Price dropped after the BoE said the story contained inaccuracies.

USDJPY traders continue to thumb their noses at the Bank of Japan and the Ministry of Finance. USDJPY climbed to 149.29 from 148.16 on the heels of higher US 10-year bond yields then eased in NY as risk sentiment improved.

AUDUSD traded in a 0.6277-0.6330 range with prices tracking US dollar sentiment. Comments from RBA Deputy Governor Michele Bullock said policymakers can keep pace with global tightening as it meets more frequently than global peers.

NZDUSD rallied from 0.5636 to 0.5703 with the peak seen after NZ inflation was a hot 7.2% y/y, easily beating the 6.6% y/y expected. Some bank analysts raised their forecasts for a November rate hike from 50 bps to 75 bps.

The US calendar includes Industrial Production, Capacity Utilization and NAHB Housing Market.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

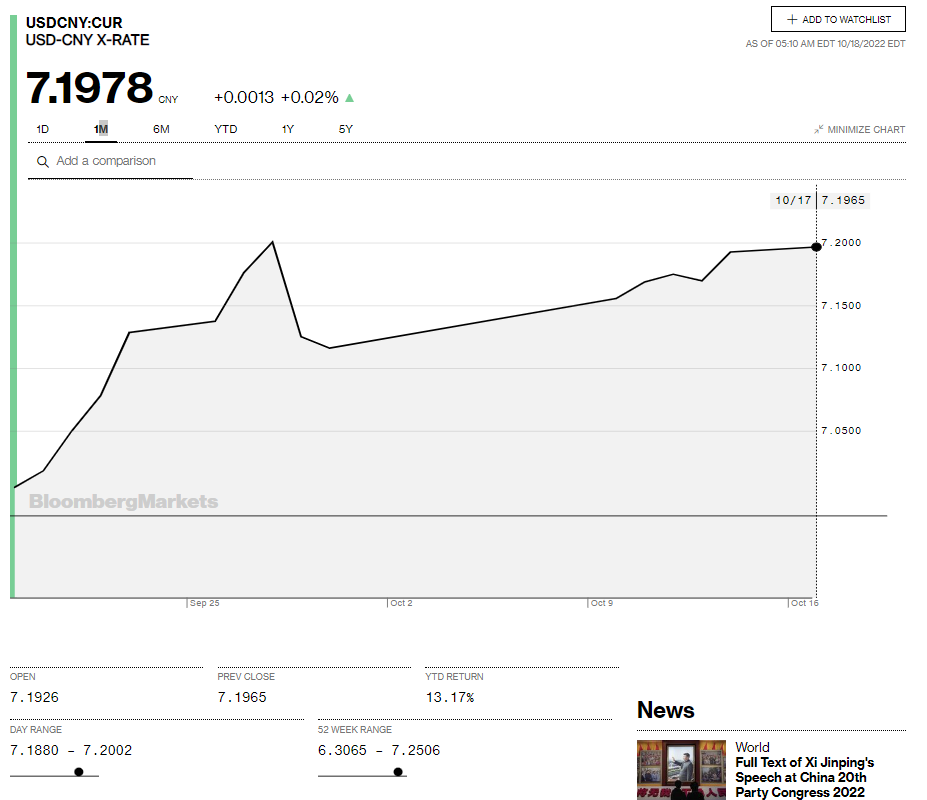

Today’s Bank of China Fix: 7.1086, previous 7.1095

Shanghai Shenzhen CSI 300 fell 0.21% to 3838.27

China delays release of GDP data during Communist Party Congress perhaps so Xi Jinping’s COVID policy doesn’t look so damaging.

Chart: USDCNY 1 month

Source: Saxo Bank