August 22, 2024

- FOMC minutes reveal policymakers on board for September rate cut.

- 818,000 US jobs vanish with NFP Benchmark revision

- US dollar trades defensively

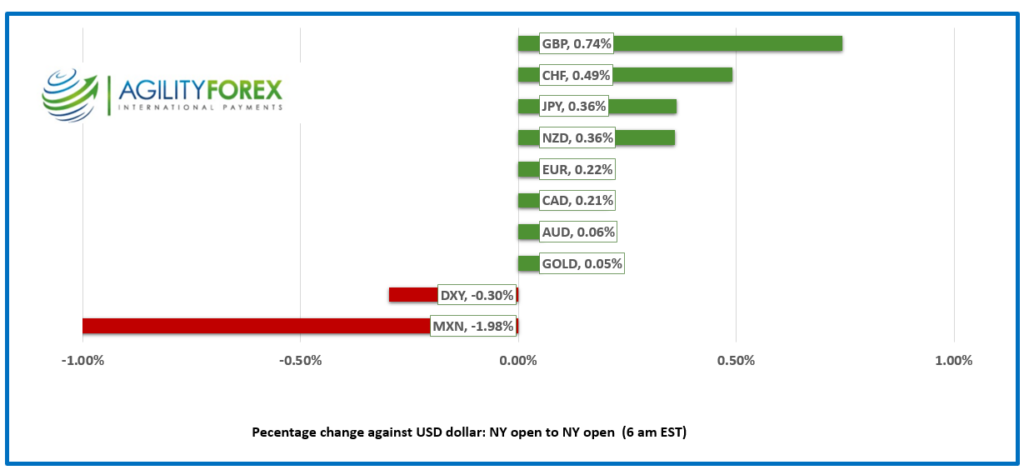

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3580, overnight range 1.3571-1.3597, previous close 1.3594

USDCAD traded defensively yesterday and slid from a peak of 1.3679 to 1.3577 then extended the losses in a 1.3571-1.3597 range overnight. The gains occurred in tandem with falling CAD/US interest rate spreads thanks to forecasts from JPMorgan and Citibank economists predicting a 50 bp Fed rate cut on September 18.

Labour woes may limit further losses. CN Rail and CPKC Rail locked out railway workers claiming that contract negotiations have broken down. A CN statement read “Without an agreement or binding arbitration, CN had no choice but to finalize a safe and orderly shutdown and proceed with a lockout.” Apparently $150,000/year is not enough for a train engineer to make ends meet. The move wreaks havoc throughout the Canadian supply chain as no goods are coming or leaving from ports. It also creates problems for the US supply chain.

The Trudeau government will order binding arbitration to end the work stoppage, but they will wait about a week to pretend they are letting both sides resolve issues at the bargaining table. Then, when they finally act, they can portray themselves as supporters of workers and the economy.

WTI oil traded in a 71.58-72.23 range, garnering a bit of support after the EIA announced crude inventories fell by 4.649 million barrels last week.

US weekly jobless claims are expected at 230,000.

USDCAD technicals

The intraday USDCAD technicals are bearish. USDCAD is in a gently sloping downtrend channel since break below support at 1.3690 last week. The top of the channel is at 1.3590 and the base is 1.3540. A topside break suggests further gains to 1.3660, then back to 1.3690.

Longer term, USDCAD is bearish following the move below the 38.2% Fibonacci retracement level ( 1.3655) which targets the 50% level at 1.3560. Failure to breech the bottom suggests further 1.3560-1.3655 consolidation. However, a decisive break below targets 1.3470 then 1.3350.

For today, USDCAD support is at 1.3590 and 1.3560. Resistance is at 1.3660 and 1.3690. Today’s Range 1.3560-1.3620

Chart: USDCAD daily

Source: DailyFX

“Now You See Them, Now You Don’t”

The US job market is about 72% weaker than the Bureau of Labor Statistics (BLS) and FOMC members believed. Oops. Instead of the anticipated 2.9 million jobs being created in the 12 months leading up to March 2024, the economy only added 2.088 million workers. Or did it? Most bank economists expected a downward revision, but yesterday’s results came uncomfortably close to the “worst case” forecasts. Traders, however, seemed unbothered. Wall Street closed with modest gains, and the 10-year Treasury yield inched up from 3.765% to 3.804% by the end of the day. Meanwhile, the US Dollar Index bounced back to 100.05 from 100.779.

FOMC Scissors: Sharp and Ready

“Snip, snip.” That’s the sound echoing through financial markets on September 18 when the FOMC is expected to announce its first interest rate cut since March 15, 2020. A rate cut is all but certain, with only the size of the cut up for debate. Yesterday’s BLS NFP revision underscores a much weaker labor market than previously thought, which could prompt a 50 bp cut, according to economists at Citibank and JPMorgan. Today’s initial jobless claims are now under the microscope. A higher-than-expected figure (forecast at 230,000) could lead Fed Chair Powell to hint at a larger cut during his Jackson Hole speech tomorrow.

Global Equity Indexes: Modest Gains Across the Board

Wall Street’s positive close translated into modest gains in Asian markets. Australia’s ASX 200 climbed 0.21%, and Japan’s Topix gained 0.25%. European bourses followed suit, led by a 0.38% rally in France’s CAC-40 and a 0.31% gain in Germany’s DAX. S&P 500 futures are flat. The US 10-year yield edged up from 3.78% to 3.82%.

EURUSD:

EURUSD traded sideways within a 1.1128-1.1166 range. Prices peaked briefly after French Services PMI jumped to 55 from 50.3, but the rally fizzled out as the gain was attributed to Olympic-related activity. The rest of the Eurozone’s PMI data was a mixed bag. Eurozone Manufacturing PMI dipped to 45.6 from 45.8, and German Manufacturing PMI dropped to 42.1 from 43.2. Traders are now holding their breath for Fed Chair Powell’s speech tomorrow.

GBPUSD:

GBPUSD rallied, climbing from 1.3081 to 1.3129, with bullish technicals pointing towards a possible test of 1.3180. Higher-than-expected UK August PMI data (Composite PMI 53.4 vs forecast 52.9, Manufacturing PMI 52.5 vs forecast 52.1, Services PMI 53.3 vs forecast 52.8) fueled the rally, which got an extra boost from EURGBP selling. GBPUSD continues to be supported by steady Bank of England interest rates, especially with the Fed likely to cut rates.

USDJPY:

USDJPY traded in a 144.85-145.76 range, with gains limited by general US dollar weakness and caution ahead of BoJ Governor Ueda’s parliamentary appearance on Friday. Prices are being weighed down by the possibility of a 50 bp Fed rate cut in September.

AUDUSD and NZDUSD:

AUDUSD traded in a 0.6727-0.6754 range overnight, retreating from its peak in early NY trading due to lower commodity prices but remains underpinned by a somewhat hawkish RBA interest rate outlook. NZDUSD mirrored AUDUSD’s movements, trading within a 0.6144-0.6170 range.

USDMXN:

USDMXN rallied yesterday following the FOMC minutes and then consolidated its gains in a 19.2713-19.3515 range ahead of today’s inflation and Q2 GDP data. The Mexican economy is expected to have grown by 2.2% y/y, unchanged from the previous month.

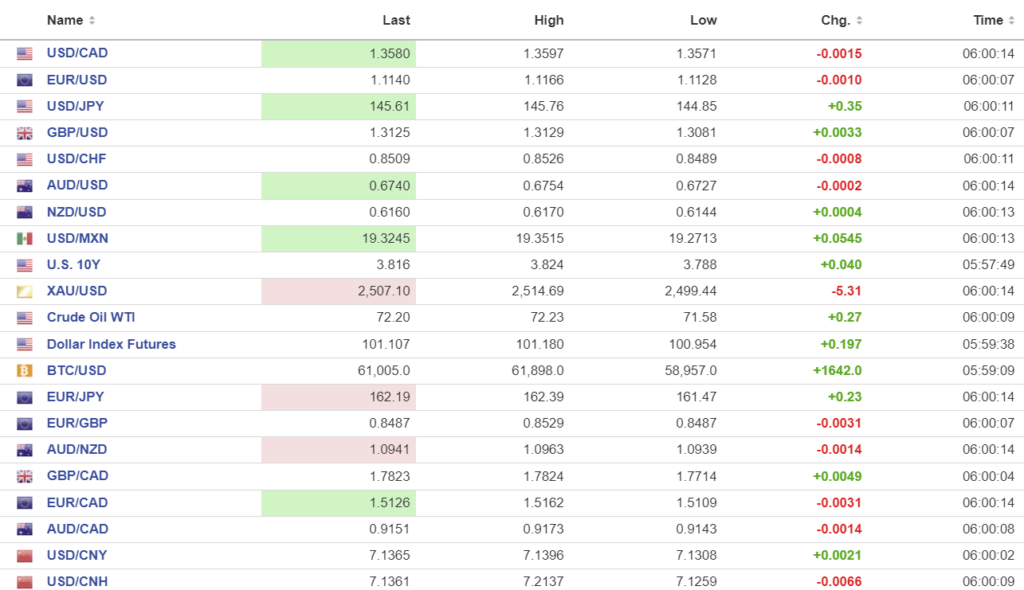

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1228 vs (prev. 7.1307).

Shanghai Shenzhen CSI 300 fell 0.26% to 3313.14

Chart: USDCNY and USDCNH

Source: Investing.com