October 11, 2024

- Canada Labor Force Survey surprises to the upside.

- US and Canadian markets closed on Monday.

- US dollar opens steady but firm.

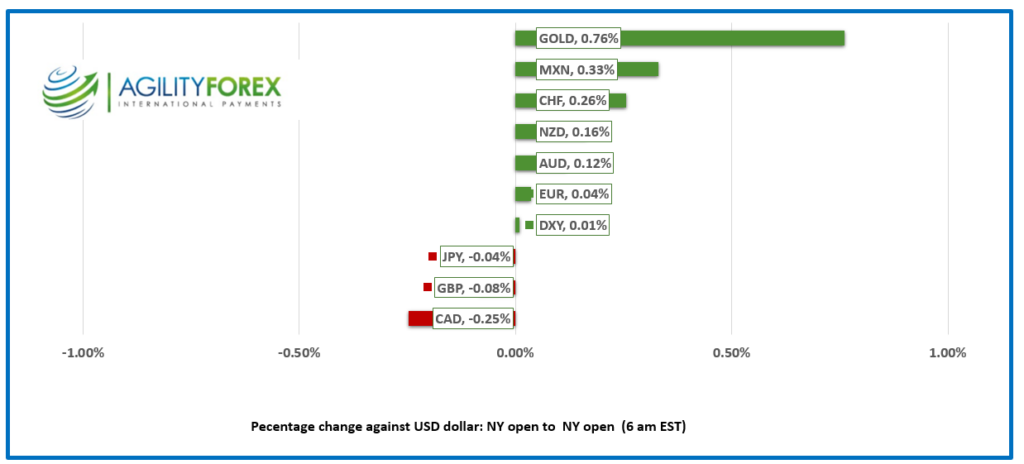

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3767, overnight range 1.3736-85, previous close 1.3740

USDCAD dropped on the heels of the September employment report, falling from 1.3777 to 1.3728. The move is not likely to be sustained because the headline numbers mask the true weakness of Canadian employment.

Today’s data showed that although employment is growing, (actual 47,000) it is not keeping pace with population growth, especially due to the influx of immigrants and non permanent residents (NPR). This population increase is diluting employment gains, as seen in the declining employment rate (actual 60.7% from 60.8%). The labor market may have expanded but there are significant challenges in absorbing the rapidly growing population into meaningful employment.

The Bank of Canada’s Business Outlook Survey is due at 10:30 am. If inflation expectations fall below the 2.0% threshold, policymakers could be alarmed by deflation risks. In that case, a 50 bp rate cut at the October 23 meeting would become almost certain.

If USDCAD is hovering around the 1.3690-1.3705 range near the 10:00 am option expiry window, volatility may spike as $2.7 billion worth of option strikes mature.

WTI oil prices remain steady, trading between 74.53-75.85, supported by fears of potential Israeli retaliation against Iran over the weekend. President Biden hinted that Israel might target Iranian oil facilities, which could tighten global supply.

With both Canadian and US markets closed for holidays on Monday, expect very light trading after lunch today.

USDCAD technicals

The intraday USDCAD are bullish and unchanged from yesterday The steep, but steady channel that started October 2 is intact and targeting 1.3800 The break above1.3750 followed by a move above1.3800 would extend gains to 1.3850. A move below 1.3750 suggests a drop to 1.3705 and perhaps 1.3660.

Longer term Fibonacci studies suggest that the convincing move above the 61.8% Fibonacci retracement level of 1.3400 (the April 2001-October 2007-monthly chart, suggests further gains to 1.4550 are in the cards.

For today, USDCAD support is at 1.3730 and 1.3710. Resistance is at 1.3790 and 1.3840

Today’s Range 1.3690-1.3790.

Chart: USDCAD monthly

Source: Investing.com

The Tortoise Laps the Hare

Fed Chair Jerome Powell’s remarks labeling September’s 50 bp rate cut as a “recalibration” hinted that another cut of the same magnitude was unlikely. Yesterday’s US inflation data has made Powell seem prophetic. The second consecutive upside surprise in Core inflation suggests that a maximum 25 bp rate cut may be on the table for November. Atlanta Fed President Raphael Bostic even mentioned that he was open to skipping a rate move altogether next month. The prospect of a Fed pause drove the US 10-year Treasury yield to 4.12% yesterday, though it eased slightly to 4.10% in NY trading today. US PPI and Consumer Sentiment data are on tap.

US Core PPI rose 2.8% y/y in September (forecast 2.7%, August 2.6%) and those results support a slower pace of Fed rate cuts.

EURUSD

EURUSD remains in the middle of its 1.0900-1.0955 range, with no significant reaction to German inflation data meeting expectations. Traders remain focused on US data and rate outlooks, with the policy divergence between the ECB and the Fed capping any substantial EURUSD gains.

GBPUSD

GBPUSD traded erratically within a 1.3022-1.3094 range. Mixed UK GDP, trade, manufacturing production, and industrial production data failed to ignite much market interest. Dovish expectations for the Bank of England contrast with more neutral expectations for the Fed, keeping GBPUSD movement limited.

USDJPY

USDJPY traded within a 148.31-149.57 range, currently sitting at 149.07. The pair is buoyed by this week’s rise in the US 10-year Treasury yield, which climbed from 4.01% to 4.12%.

AUDUSD & NZDUSD

AUDUSD traded with a slight positive bias within a 0.6701-0.6750 range. Traders are eyeing the possibility of a positive stimulus announcement from Chinese officials over the weekend. NZDUSD mirrored the Aussie, trading between 0.6057-0.6106, as it attempts to recover from losses triggered by the RBNZ’s 50 bp rate cut earlier this week.

USDMXN

USDMXN traded lower within a 19.4151-19.6210 range, with gains building after the release of Banxico’s monetary policy meeting minutes yesterday. Policymakers expect rates to fall further if inflation continues to ease, though concerns remain as inflationary pressures still pose challenges.

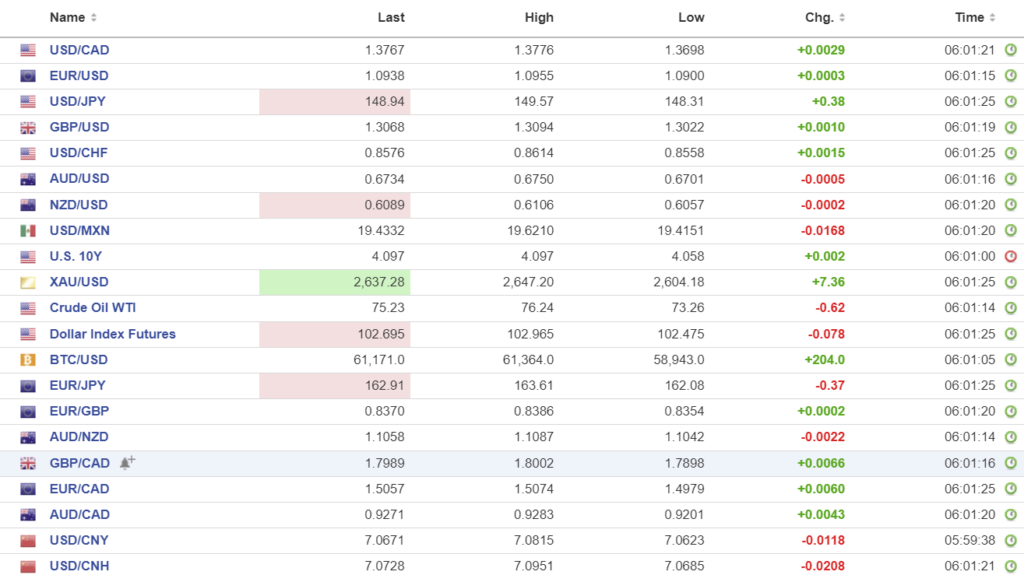

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0731 (prev. 7.0702)

Shanghai Shenzhen CSI 300 fell 2.77% to 3887.17

Xi Jinping is threatening Taiwan after President William Lai reminded Beijing that the two countries “are not subordinated to each other.” Jinping, overseeing a floundering economy, a property market crisis, and fearing social unrest may be planning on using a war to raise his fortunes. Dictators throughout history have used the same tactic. Taiwan reported that in the past 24 hours (until 6am Friday) the PLA sent 20 aircraft and 10 ships on a “patrol” around the island. US Secretary of State Antony Blinken described China’s actions as “increasingly dangerous and unlawful.”

Investors have been unimpressed with the amount of fiscal investment announced to date and are hoping that Saturday’s Finance Minister’s briefing will result in a massive stimulus announcement. However, other analysts are suggesting Beijing mya add stimulus in increments to avoid over stimulating the economy.

Chart: USDCNY and USDCNH

Source: Investing.com