Photo: Bing AI

September 29, 2023

- Falling Treasury yields lift equities.

- US Core PCE falls to 3.9% as expected.

- US dollar giving back some of Septembers gains.

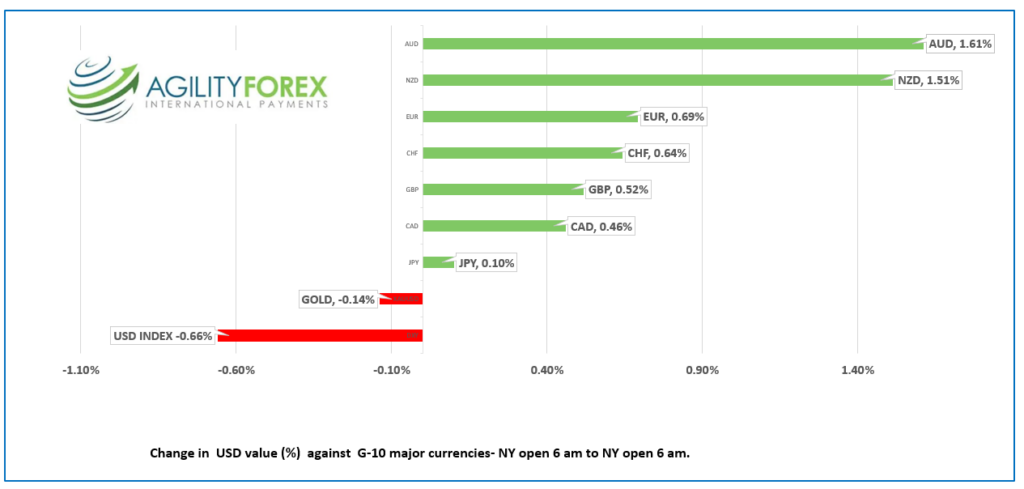

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3423-27, overnight range: 1.3417-1.3507, close 1.3487

USDCAD retreated from resistance yesterday and extended its fall overnight due to widespread US dollar selling on the back of falling Treasury yields. There wasn’t any specific catalyst for the move which suggests it is due to month and quarter end flows and if so, likely to be short-lived.

Canada’s economy was flat in July, a tick below the 0.1% expected and further evidence that rate hikes are taking a toll on economic growth. Statistics Canada said, “The manufacturing sector (-1.5%) had the largest negative contribution in July, its largest since April 2021. This was the second consecutive monthly contraction for the sector.”

WTI oil prices retreated from Thursday’s $95.03/b peak to $91.53/b overnight. They have recovered to $92.84/ bin NY trading and ongoing supply/demand imbalances suggest limited downside.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3460, looking for a move below 1.3410 to extend losses to 1.3360. A break above 1.3460 shifts the focus to 1.3600 again.

Longer term the uptrend line on a weekly chart from April 2022, is intact while prices are above 1.3210.

For today, USDCAD support is at 1.3410 and 1.3380. Resistance is at 1.3460 and 1.3510. Todays Range 1.3410-1.3510.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

September is scurrying into the annals of history, and Wall Street bulls couldn’t be happier. The S&P 500, a favorite risk barometer, dropped 5.19% from the start of the month until Tuesday when it began clawing back some losses. It is down 4.61% as of yesterday’s close.

PCE-excluding food and energy fell to 3.9% from 4.3% in July. It certainly didn’t fall enough to suggest the Fed will deviate from its higher for longer policy at its next meeting.

Risk sentiment improved dramatically as US Treasury yields retreated yesterday and overnight. The 10-year Treasury yield fell to 4.542% in NY today, from 4.64% yesterday, which fueled a 0.49% rally in S&P 500 futures. Traders should not party too hardy.

September has lived up to its advanced billing for being a weak month for stocks, and October may follow suit. The Great Crash of 1929 (Black Tuesday) occurred in October. So did Black Monday, which happened on October 19. On that day, the DJIA plunged 22.6%, and the S&P 500 dropped 20.5% due to program trading, stock overvaluation, rising interest rates, and trade deficits. Sounds a lot like September 2023.

The US government is on the cusp of another shutdown. It comes as no surprise. Republicans and Democrats can’t even agree on the day of the week.

EURUSD rallied to 1.0617 from 1.0558 due to broad US dollar weakness and lower-than-expected Eurozone inflation. HICP dropped to 4.3% y/y in September (forecast 4.5%) compared to 5.2% in August, which offset negative sentiment from weaker-than-forecast German retail sales (actual -1.2% m/m vs. forecast 0.5%). Today’s rally may be short-lived as the EURUSD downtrend is intact while prices are below 1.0660.

GBPUSD is at the top of its 1.2197-1.2272 range, with prices getting a lift from upwardly revised Q2 GDP to 0.6% y/y from 0.4% previously. GBPUSD also benefited from widespread US dollar selling pressures. Brexit supporters may be astonished to discover that the UK is still under the heel of the European Court of Justice. The Financial Times reported that the court fined the UK because it allowed pleasure boats to use lower-taxed red diesel. The UK government is likely to pay the fine as they said it was a historical case that began when the UK was in the EU.

USDJPY dropped to 148.53 from 149.51 due to falling US Treasury yields. The BoJ bought bonds to halt the rise in JGB yields, which climbed to 1.73% yesterday, the highest level since 2013. Japanese data was mixed. August Retail Trade rose 7.0% y/y (forecast 6.6%), while Industrial production fell 3.8% from -2.3% previously.

AUDUSD traded bullishly in a 0.6420-0.6502 range supported by rebounding commodity prices and broad US dollar weakness. Australia is on holiday Monday, and the RBA meeting is Tuesday. They are expected to leave rates unchanged.

US Purchasing Managers Survey, and the Michigan Consumer Sentiment and Consumer Inflation Expectations reports are still ahead..

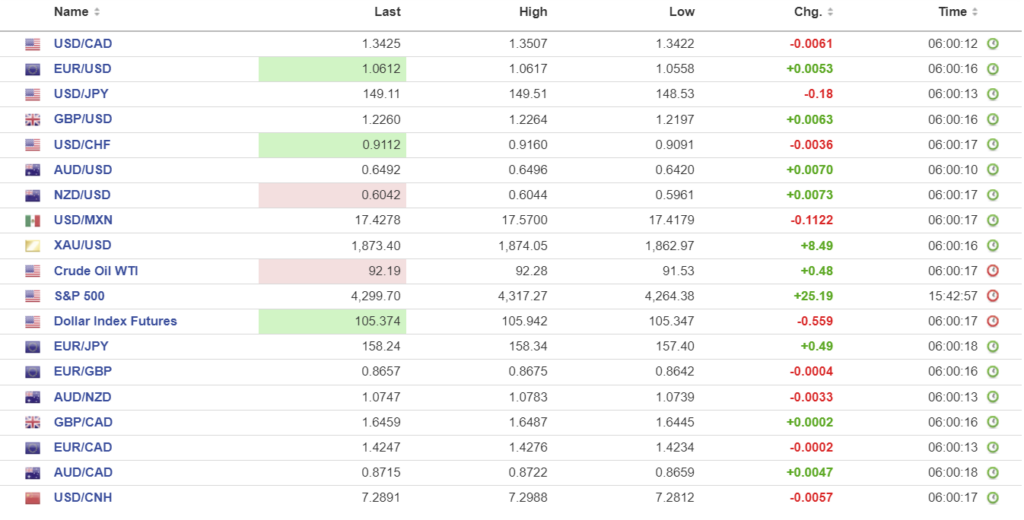

FX high, low, open

China Snapshot

Chinese markets are closed for Golden Week holidays.

Bank of China Fix: closed. previous 7.1798.

Shanghai Shenzhen CSI 300 closed for Golden Week.

Chart: USDCNH (offshore)

Source: Bloomberg