Photo:Pixabay

May 11, 2023

- Bank of England hikes rates by 25%-no surprise

- Weak Chinese inflation lifts US dollar.

- US dollar posts gains overnight, opens mixed from Wednesday.

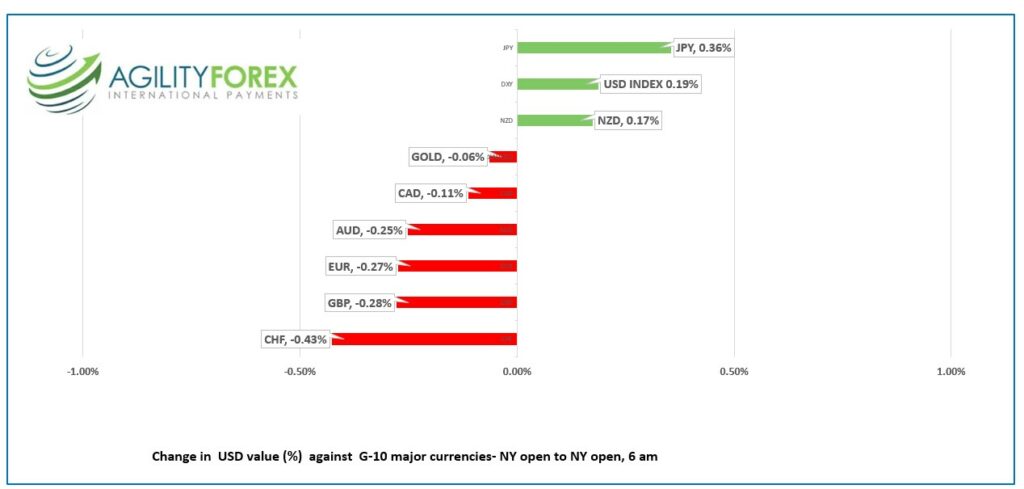

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3405-09, overnight range 1.3365-1.3427, close 1.3372

USDCAD came within spitting distance of support in the 1.3290-1.3410 area yesterday, then rallied to test the downtrend line from May 4.

An ambivalent April US inflation report, which provided fodder for hawks and doves, combined with soft Chinese inflation data, to reinvigorate the greenback.

Chinese April CPI rose a mere 0.1% y/y (forecast 0.3%, March 0.7%) while April PPI fell 3.6% y/y (forecast -3.2%, March -2.5%). The results raised fears that China’s post-covid zero economic rebound was fading which puts the global economic recovery in jeopardy.

WTI oil prices chopped about in a $72.71/b-$73.47 range supported by yesterday’s EIA report showing US crude inventories rose 2.95 m/b. Prices are also bolstered by supply Canadian supply disruptions due to wildfires in Alberta.

USDCAD Technical Outlook

The USDCAD technicals are bearish while prices are below 1.3420 (4-hour chart), looking for a break below 1.3290 to extend losses to the 1.3200-20 area. Yesterday’s rally from 1.3332 failed to break above the May 4 downtrend line suggesting the gains were just a correction, leaving USDCAD with a negative bias.

A move below 1.3290 suggests further losses to 1.3000, while a decisive break above 1.3420 targets 1.3520.

For today, USDCAD support is at 1.3360 and 1.3310. Resistance is at 1.3430 and 1.3460

Today’s range 1.3360-1.3440

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The highly anticipated US April inflation report proved disappointing. It supported arguments from both sides of the interest rate debate.

Traders are convinced that because the annual inflation rate dipped to 4.9% from 5.0%, it is all the evidence the Fed needs to pause rate hikes in June. Then, it can start cutting rates in September.

Fed officials are not on the same page. Chair Powell hinted at pausing rate hikes at the May 3 FOMC meeting. However, he stressed that if inflation proved stickier than expected they would hike rates again. Mr Powell said that inflation would decline slowly and if policymakers forecasts are correct, it would not be appropriate to cut rates.

Initial jobless claims rose 22,000 to 264,000 last week while PPI ex-food and energy dipped to 3.2% y/y from 3.4% in March. The results are encouraging for those expecting rate hikes; however they are also evidence that the US may fall into a recession.

Rising recession risks are lifting the US dollar while rate cut sentiment is underpinning equities.

Asia equity markets closed with small losses, while European bourses traded with small gains. S&P 500 futures have trimmed earlier gains and are just about unchanged as of 5:40 am PT.

EURUSD is trading choppily in a 1.0919-1.0997 band. ECB officials, Pablo Hernandez de Cos and Francois Villeroy are suggesting the tightening cycle is close to over which eroded some EURUSD support.

GBPUSD is churning in a 1.2567-1.2640 range with price action tracking Bank of England Governor Bailey’s monetary policy press conference. The BoE hike rates by 25 bps, lifting its benchmark rate to 4.50%. It was expected. Mr Baily was optimistic. He predicted inflation would be cut in half this year and that the country would avoid a recession.

USDJPY gave up European gains and dropped to 133.75 from 134.84 in tandem with the US 10-year Treasury yield falling to 3.55% from 3.4366 earlier today.

The Bank of Japan Summary of Opinions reiterated the dovish monetary policy outlook.

AUDUSD is trading at the bottom of its overnight 0.6723-0.6795 range due to broad US dollar strength after today’s PPI and jobless claims data.

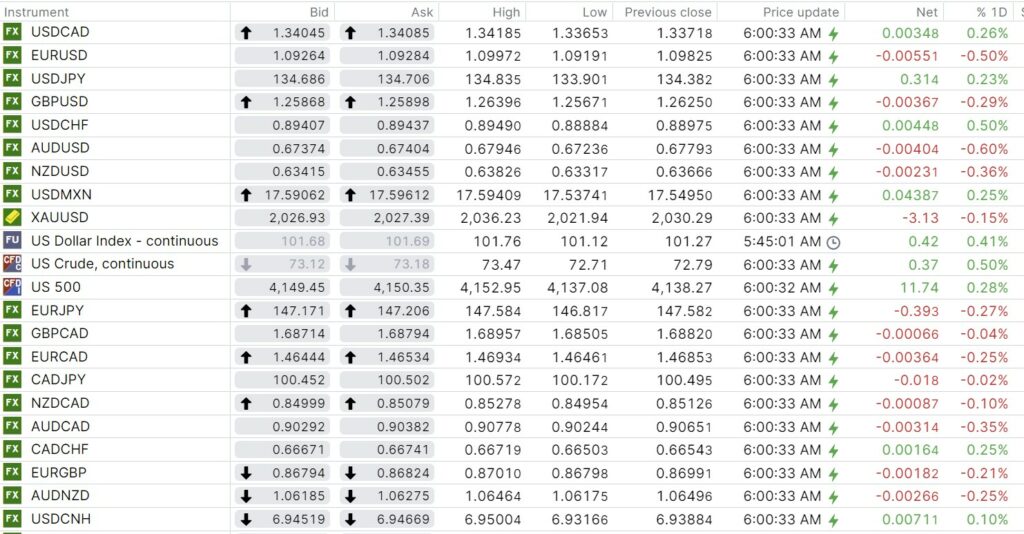

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

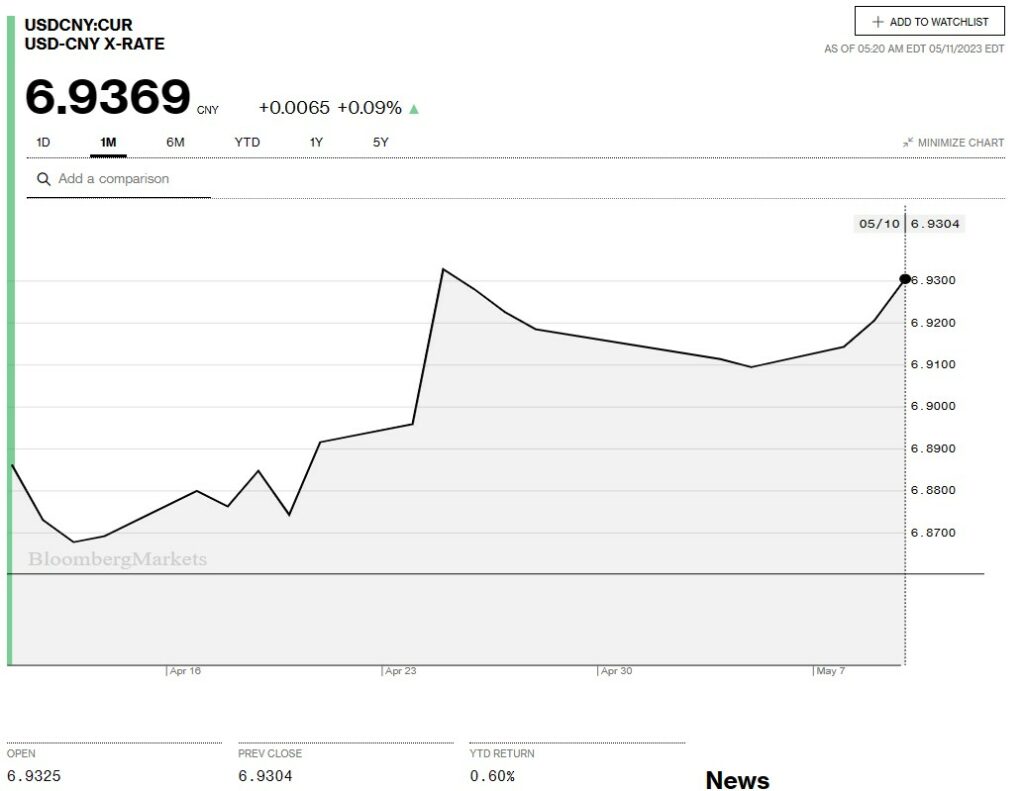

China Snapshot

Bank of China Fix: 6.9101 previous 6.9255.

Shanghai Shenzhen CSI 300 fell 0.16% to 3990.66.

April CPI 0.1% y/y (forecast 0.3%, March 0.7%)

April PPI -3.6% y/y (forecast -3.2%, March -2.5%)

The drop in CPI and PPI raises questions about the sustainability of the post-covid zero economic rebound.

Chart: USDCNY 1 month

Source: Bloomberg