Photo: BingAI

July 17, 2023

- Sluggish Chinese data sours risk sentiment.

- Oil prices slip as Libyan supply resumes.

- USD opens mixed from Friday-AUD and CAD underperform.

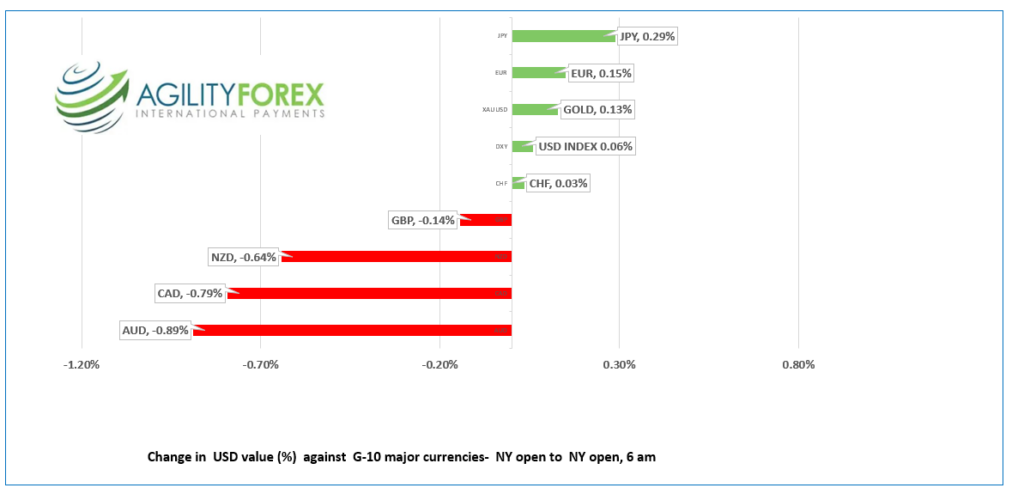

FX at a glance:

Source: IFXA Ltd

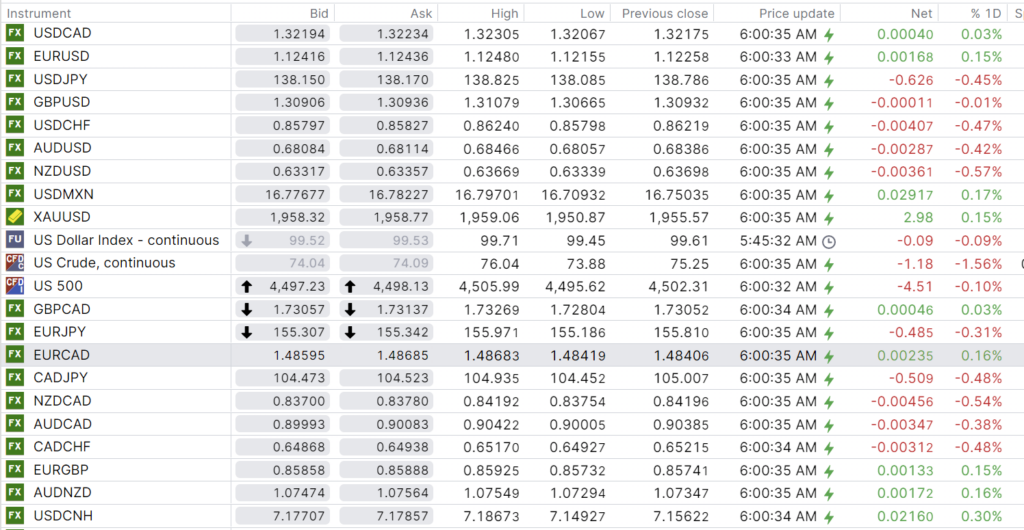

USDCAD Snapshot: open 1.3219-23, overnight range 1.3207-1.3231, close 1.3218

USDCAD is consolidating Friday’s gains after US data and oil prices sparked a sharp rally. USDCAD was in a downtrend after it peaked at 1.3385 on July 7. Prices traded with a negative bias until finding a floor in the 1.3090-1.3100 in Asia on Friday. Stronger than expected University of Michigan Consumer Sentiment index on Friday, and a drop in oil prices fueled the gains.

News that Libya restarted one of its oil fields knocked WTI from Friday’s peak of $77.26/b $73.88/b in early NY trading today.

USDCAD direction continues to be determined by the outlook for US interest rates. Friday’s Michigan supported expectations for another 25 bp rate hike on September 20, then a rate cut in March.

Canada Wholes Inventories rose 3.5% m/m in May, as expected and a non-event for FX.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while above 1.3170, supported by the break above 1.3150, which was the top of the downtrend channel from July. The rally is just a correction if prices stay below 1.3240 and a move below 1.3170 would ship the focus to 1.3100.

Longer term, The USDCAD uptrend from May 2021 comes into play in the 1.3030-40 area.

For today, USDCAD support is at 1.3170 and 1.3100. Resistance is at 1.3240 and 1.3305. Today’s range 1.3150-1.3250.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

“Is it hot enough for you?” Severe weather conditions, including scorching heatwaves, thunderstorms, and typhoons, are wreaking havoc across Asia, Europe, and North America, leaving traders demotivated.

Asian equity markets closed slightly lower, with Japanese markets closed for a holiday and the Hong Kong Hang Seng index suspended due to a typhoon. European bourses are trading in negative territory, with the German Dax down by 0.31% and S&P 500 futures experiencing a modest decline of 0.12%. WTI oil prices have fallen by 1.68%, while gold remains stable.

EURUSD is approaching its peak after fluctuating between 1.1216 and 1.1248 since the Asian market opened today. The continued gains are driven by the expectation that the Federal Reserve has only one more rate hike in store, with the first rate cut anticipated in March. Meanwhile, the European Central Bank’s outlook remains hawkish, and ECB President Lagarde is expected to reinforce this stance in her upcoming speech.

GBPUSD is currently consolidating last week’s gains within the range of 1.3067-1.3108. Traders are eagerly awaiting Wednesday’s CPI data, which is forecasted to be 8.2% (compared to May’s 8.7%). If the result exceeds expectations, it would almost confirm the Bank of England’s plan to raise rates by 50 bps on August 3. Additionally, the UK Rightmove House Price Index showed a 0.2% month-on-month decline in July, following a previous reading of 0.0%.

USDJPY is near the lower end of its range, fluctuating between 138.17 and 138.83. The market is experiencing lighter-than-usual trading volumes due to a national holiday. Finance Minister Shunichi Suzuki confirmed that exchange rates were not discussed during the G7 Finance Minister meeting in India. Expectations that the Bank of Japan may make adjustments to tighten monetary policy continue to weigh on USDJPY.

AUDUSD is trading with a negative bias within the range of 0.6806-0.6847 due to broad US dollar strength and disappointment over weaker-than-expected China Q2 GDP data, The market has not shown significant reaction to the news of Michelle Bullock’s appointment as the replacement for outgoing RBA Governor Philip Lowe. Bullock, who has worked at the central bank for 38 years, is not expected to alter the RBA’s monetary policy outlook.

The US data calendar is empty.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

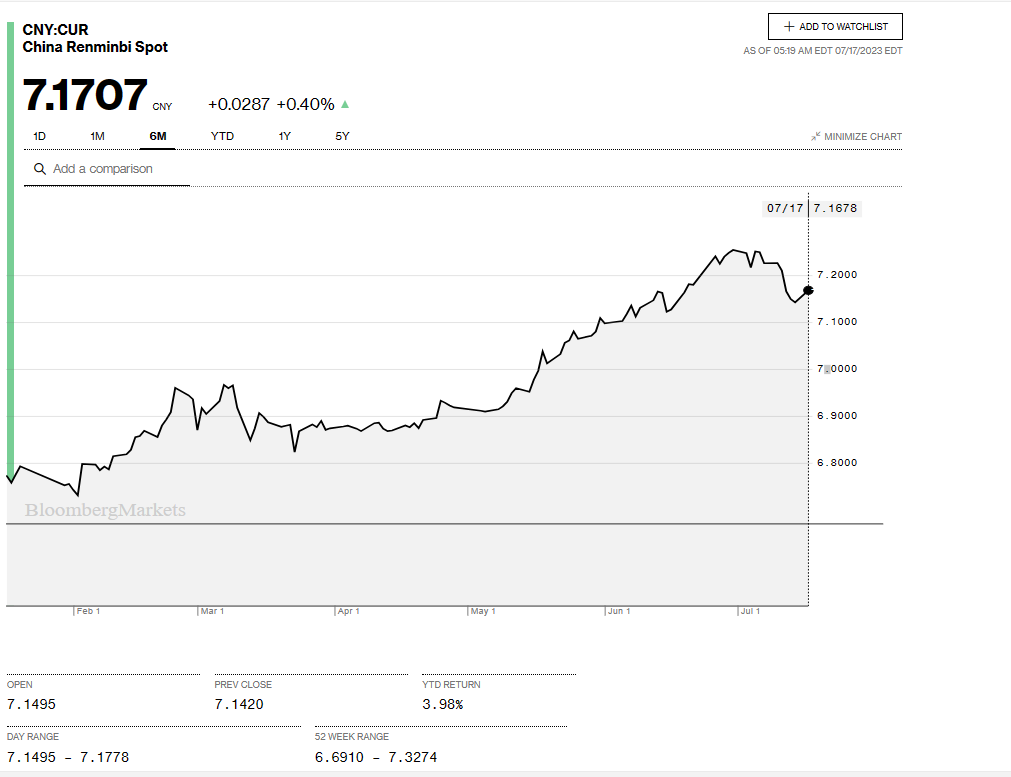

China Snapshot

Bank of China Fix: 7.1326 expected 7.1386, Previous 7.1318

Shanghai Shenzhen CSI 300 fell 0.82% % to 3867.17.

Q2 GDP actual 6.3% (forecast 7.3%, previous 4.5%). June Industrial Production actual 4.4% (forecast 2.7%, previous 3.5%). June Retail Sales actual 3.1% (forecast 3.2%, previous 12.7%).

The disappointing data raises questions about China achieves its 5.0% GDP growth target.

Chart: USDCNY 6 month

Source: Bloomberg