September 4, 2024

- Bank of Canada expected to announce a dovish 25 bp rate cut.

- Negative risk sentiment weighing on stocks.

- US dollar opens mixed compared to Tuesday.

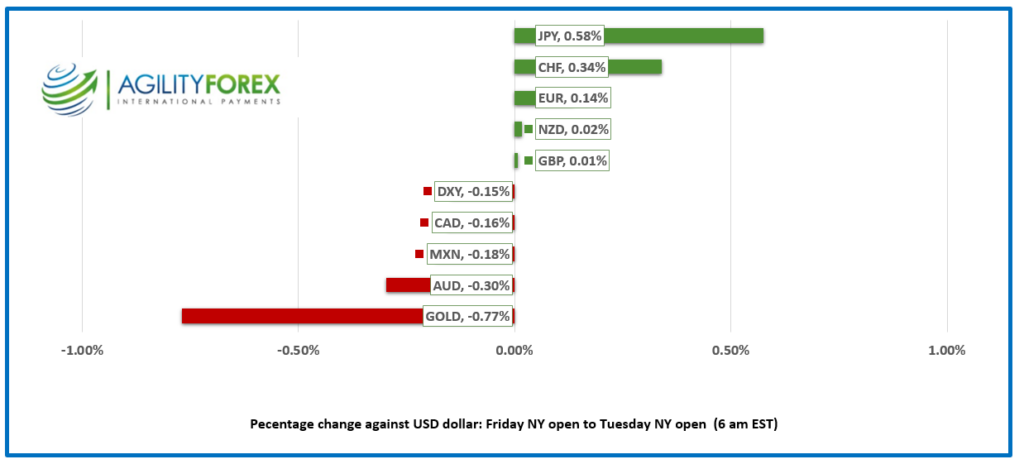

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3556, overnight range 1.3533-1.3563, previous close 1.3552

USDCAD rallied on the back of broad-based US dollar demand triggered by the stock market melt-down on Wall Street yesterday and managed to hang on to the gains overnight. A litany of woes combined to spook traders and the disappointing ISM Manufacturing result (47.2, forecast 47.5, July 46.8) led the way as it caused chatter about a US hard landing. That worry has elevated the importance of today’s JOLTS survey.

The Bank of Canada will cut rates by 25 bps today which is already priced in. The tone of the statement will be key and if it alludes to faster and deeper rate cuts, USDCAD downside will be limited.

WTI oil traded in a 69.19-71.45 range overnight due to the combination of weak Chinese economic data and Opec’s plans to start increasing production beginning October 1. A sustained move below $70.00 would provide some support to USDCAD.

USDCAD technicals

The intraday USDCAD technicals are bullish while trading above 1.3520 and looking for a decisive break above 1.3580 to extend gains to 1.3630 where the downtrend line from August 6 comes into play. Failure to break above that line argues for a revisit to support at 1.3440.

For today, USDCAD support is at 1.3520 and 1.3490. Resistance is at 1.3580 and 1.3630. Today’s Range 1.3520-1.3620.

Chart: USDCAD 4 hour

Source: Investing.com

“They’re Coming to Take You Away, Ha-haa”

The novelty song of the same title was released in 1966 and reached number 3 on the Billboard Hot 100 chart. It is considered non-pc today despite the lyrics being about a dog. Nevertheless, Nvidia CEO Jensen Huang is singing those lyrics as Justice Department officials issued subpoenas for an antitrust investigation. Mr Huang wasn’t the only person unimpressed. Nvidia investors knocked $280 billion off its market cap and helped fuel the Tuesday market meltdown on Wall Street.

JOLTS May Jolt Hard Landing Fears

The labour market is now the Fed’s top concern, putting today’s Job Openings and Labour Turnover Survey (JOLTS) in the limelight. Expectations are for a decline in job openings to 8.1 million from the prior 8.1874 million, continuing the uneven downtrend since January’s peak of 8.748 million.

Global Equities Follow Wall Street’s Lead

Wall Street had a rough day, with the Nasdaq plunging 3.26%. Asian markets wasted no time following suit; Japan’s Nikkei 225 plummeted 4.24%, and the Topix slid 3.65%. Australia’s ASX 200 dropped 1.86%. Europe joined the risk-off mood, with the French CAC leading the charge down, plunging 0.90%. S&P 500 futures are off by 0.37%, while the US 10-year Treasury yield holds steady at 3.815%.

EURUSD

EURUSD remained range-bound between 1.1039 and 1.1063, modestly supported by bullish technicals and growing concerns of a hard US landing, stoking hopes for faster and deeper Fed rate cuts. The Euro also got a boost from upbeat Eurozone composite PMI data, signaling the economy’s fastest growth in three months, helped along by Paris Olympic buzz.

GBPUSD

GBPUSD traded with a slight bid in the 1.3101-1.3128 range after dipping to 1.3087, following the release of US ISM Manufacturing PMI data and negative risk sentiment from Wall Street. Prices were supported by a stronger-than-expected UK Services PMI reading (actual 53.7 vs. forecast 53.3), with S&P Global noting a recovery in UK service sector performance amid improving economic conditions and domestic political stability.

USDJPY

USDJPY drifted lower within a 144.75–145.56 range, touching a low in early European trading before rebounding to 145.10 in New York. Selling pressure on USDJPY was driven by safe-haven yen demand after the US stock market turmoil rattled investors. The pair also tracked US 10-year Treasury yields, which remained steady at 3.815%.

AUDUSD and NZDUSD

AUDUSD was on the defensive in early Asia, falling from 0.6710 to 0.6685 after mixed Manufacturing and Services PMI readings. However, it rebounded to 0.6716 by the New York open. Australia’s Q2 GDP disappointed, rising just 0.2% q/q and 1.0% y/y, a figure slightly better than the RBA’s forecast but still the weakest annual growth since the 1990s.

NZDUSD mirrored AUDUSD moves, trading within a narrow 0.6169–0.6195 range.

USDMXN

USDMXN traded in a tight 19.7462–19.8540 range after spiking to 19.9844 following the release of disappointing US services PMI data. Analysts at JP Morgan see USDMXN as vulnerable to downside risks, citing Mexico’s trade balance, rising remittances, and its independent central bank. High Mexican interest rates compared to the US are also keeping the carry trade alive.

Bitcoin (BTCUSD)

Bitcoin took a hit, along with other fiat currencies, dropping from 59,481 to 56,010 before grinding higher to 56,924 in New York. The decline mirrored the slump in US and Asian stock markets.

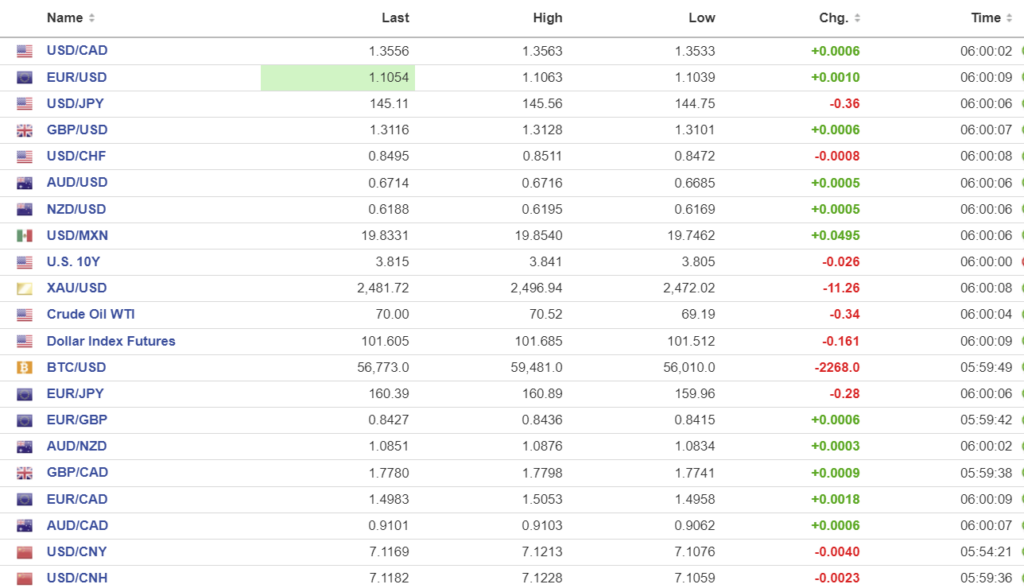

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1148 vs exp. 7.1167 (prev. 7.1112).

Shanghai Shenzhen CSI 300 fell 0.65% to 3252.16

Caixin August Services PMI51.6, (forecast 52.2, July 52.1) Bank of America cuts its China GDP forecast to 4.8% from 5.0%

Chart: USDCNY and USDCNH

Source: Investing.com