May 21, 2024

- Canada CPI falls-improves odds for June rate cut.

- No US data but plenty of Fed speakers today.

- US dollar opens lower from Friday, but little changed since Monday’s close.

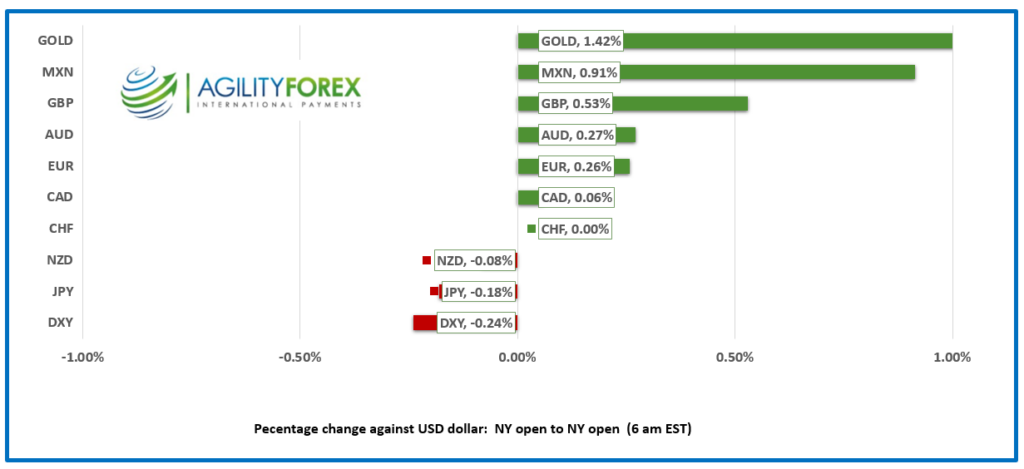

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3630, Friday-Tuesday NY open range 1.3580-1.3659, Friday close 1.3635, Monday close 1.3619

USDCAD opened little changed from where it closed on Friday then inched higher following the April inflation report. Canada CPI rose to 2.7% y/y as expected but below the 2.9% seen in March. The BoC Core CPI index rose just 1.6% compared to 2.0% in March and that sets the stage for a June rate cut. Two weeks ago, BoC Governor Tiff Macklem said. “We do see renewed downward momentum in underlying inflation. The message to Canadians is, we are getting closer. We are seeing what we need to see and we just need to be confident that it will be sustained.” Today’s results should make them confident. USDCAD climbed from 1.3622 to 1.3659 following the data.

WTI oil prices are trading at the bottom of is 78.00-79.30 range due to downgraded risks of Middle East oil supply being disrupted and news that rain helped to contain the wildfires threatening crude production in Fort MacMurray.

USDCAD Technicals

The intraday USDCAD technicals are modestly bearish below 1.3650 looking for a move below 1.3600 to extend losses to 1.3550. A move above 1.3650 targets a retest of 1.3690.

The daily chart tells a different story. The short term downtrend channel from April 16 is intact although prices are just above the pivot line of 1.3618. The channel suggests further losses to 1.3330. However, the January 1 2024 uptrend line is intact above 1.3550 and while prices are above this level, a retest of 1.3850 is still likely.

For today, USDCAD support is at 1.3610 and 1.3570. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3610-1.3690.

Chart: USDCAD daily

Source: DailyFX

Hard-liner, Harder landing

Hardline Iran President Ebrahim Raisi hardlined into some mountains yesterday. By all accounts, he was not a nice man, but his demise may weaken Iran’s support for Hamas, at least temporarily.

FOMC in no hurry to cut rates.

Fed officials continue to express a lack of confidence that inflation is falling in a sustainable manner. Cleveland Fed President Loretta Mester said three rate cuts in 2024 is no longer appropriate. Bond traders are slowly getting the message. The US 10-year Treasury yield is trading sideways around 4.43%. The S&P 500 closed with a tiny gain yesterday, Asian equity indexes closed with losses, and European bourses are in the red. S&P 500 futures are flat.

EURUSD

EURUSD traded indecisively in a 1.0836-1.0897 range since Friday and is sitting at 1.0870 in NY. There are no top-tier US economic reports on the slate this week, and the FOMC minutes from the May 1 meeting are stale, leaving tomorrow’s speech by ECB President Christine Lagarde and Thursday’s Eurozone PPI data to provide direction. German and Eurozone data were ignored.

GBPUSD

GBPUSD consolidated Friday’s gains in a 1.2688-1.2726 range since Monday, supported by broad US dollar weakness. Traders are cautious ahead of tomorrow’s PPI and CPI data, which will determine whether the Bank of England cuts rates at the June 20 meeting.

USDJPY

USDJPY drifted higher, rising from Friday’s low of 155.25 to 156.65 overnight, mainly because the US 10-year Treasury yield climbed to 4.42% from 4.37% on Friday. Prices dipped in Europe and are trading at 156.15 in NY. Japanese Finance Minister Shunichi Suzuki repeated his usual blather about dealing appropriately if FX moves become unstable.

AUDUSD AND NZDUSD

AUDUSD traded defensively after peaking at 0.6710 yesterday and dropping to 0.6646 overnight, before inching higher to 0.6670 in early NY trading. The RBA minutes from May 7 showed that policymakers discussed raising rates before leaving them unchanged, but that is old news. Consumer Confidence fell (actual -3, previous -2.4).

NZDUSD closed at 0.6131 on Friday and then traded sideways in a 0.6089-0.6139 range since. Traders are content to sit on the sidelines until Wednesday’s RBNZ monetary policy meeting.

USDMXN

USDMXN drifted lower, falling from Friday’s peak of 16.7182 to 16.5830 today. Traders ignored the surprise drop in Mexican March retail sales yesterday (actual -1.7% y/y, February 3.0%) but remained under pressure after Banxico Deputy Governor Irene Espinosa complained that the March rate cut was premature. She said, “The monetary restriction that was needed to maintain convergence (of inflation to the target) within the horizon that we had planned was reduced.” Her comments suggest further Banxico rate cuts may be delayed.

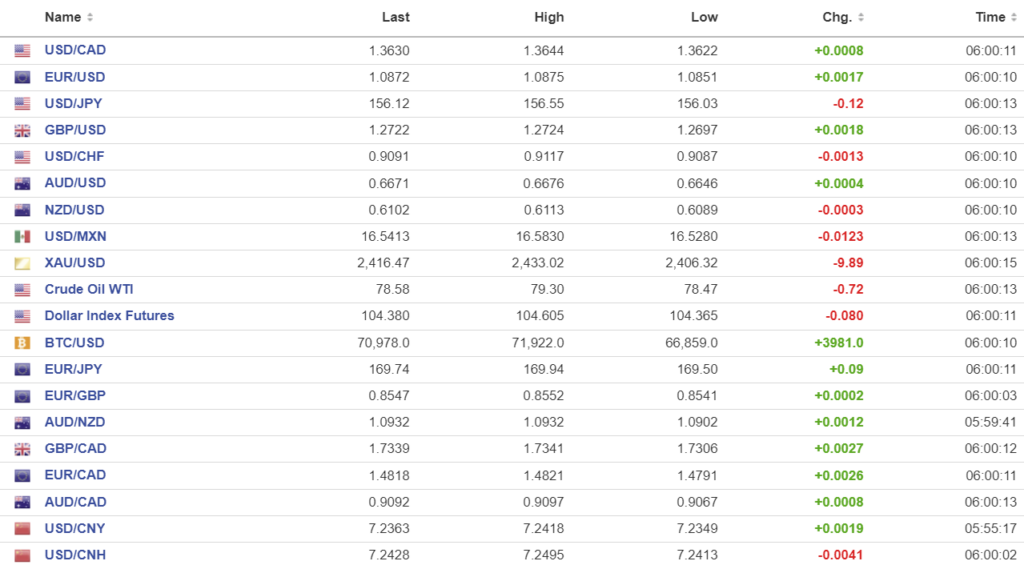

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1069 vs exp. 7.2366 (prev. 7.1042).

Monday: PBoC fix: 7.1042 vs exp. 7.2162 (prev. 7.1045)

Shanghai Shenzhen CSI 300 fell 0.40% to 3676.16

Monday-PBoC left 1-year and 5-year Loan Prime Rate unchanged at 3.45% and 3.95% respectively.

Chart: USDCNY and USDCNH

Source: Investing.com