Photo: Bing Image Creator

September 6, 2023

- Rising oil prices stoke inflation fears.

- Bank of Canada expected to leave rates unchanged.

- USD opens mixed but keeps bullish bias.

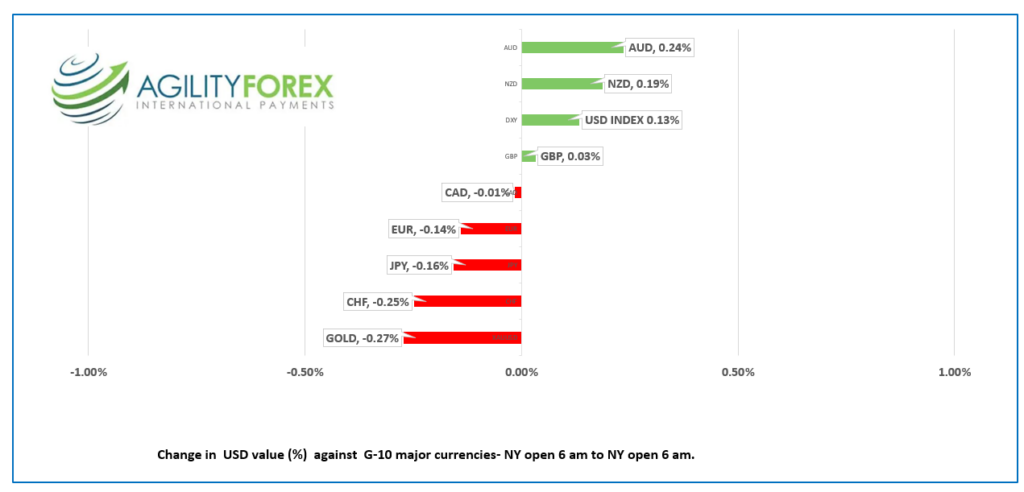

FX at a Glance

Source: IFXA/RP

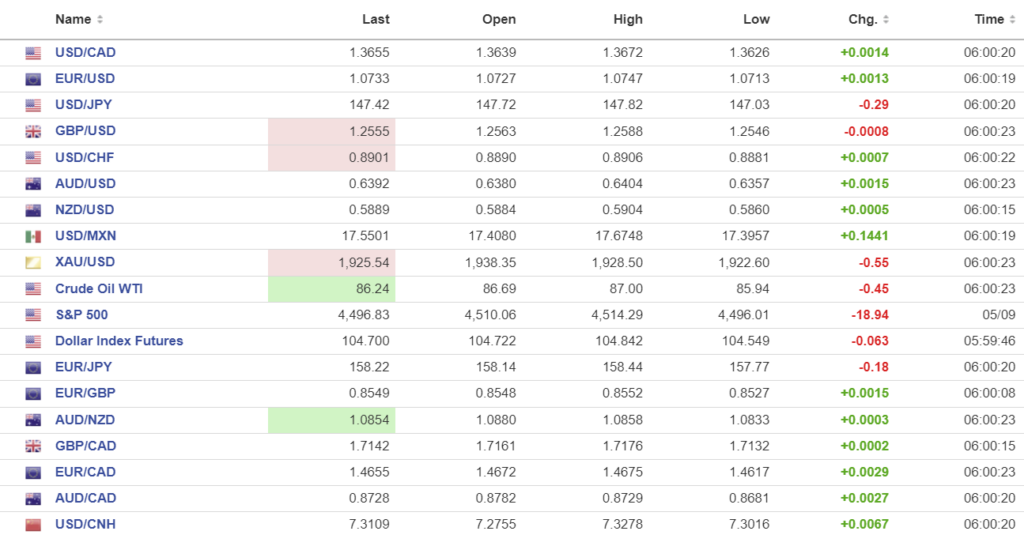

USDCAD Snapshot: open: 1.3653-56, range since Friday: 1.3626-1.3672, close 1.3641

USDCAD traded choppily yesterday, and that will be the case today.

Bank of Canada Governor “Hamlet” Macklem will answer the question “to hike or not to hike” today when he releases the monetary policy statement at 7:00 am PDT. Despite higher than expected inflation and a still tight labour market, most economists and analysts believe rates will be left unchanged at 5.0%. However, the statement will be somewhat hawkish due to inflation remaining stubbornly have the BoC’s 2.0% target.

There is a small risk that BoC Governor could surprise markets with a hike to demonstrate its independence from political influence. Ontario Premier Doug Ford, BC Premier David Eby, and Newfoundland and Labrador Premier Andrew Furey have written letters to Mr. Macklem urging him to refrain from further rate hikes, as they are exacerbating the housing affordability crisis. Mr. Ford wrote, “Your rate hikes have made it next to impossible for young people, newcomers, and first-time homebuyers to have any place to call home.”

USDCAD gains are being slowed by rising oil prices. WTI traded in a $85.94-$87.00/b range due to Saudi Arabia and Russia extending previously announced production cuts until year end.

USDCAD Technicals

The intraday USDCAD technicals are bullish while trading above 1.3605 which guards the 1.3540, August uptrend line. A break above the 1.3680-90 area suggests further gains to 1.4000. A break below 1.3605 then 1.3540 argues that a short term top is in place at 1.3670 and would target 1.3360.

For today, USDCAD support is at 1.3610 and 1.3570. Resistance is at 1.3680 and 1.3720. Today’s range 1.3590-1.3690.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Oil prices and Treasury yields are working in concert to fuel US dollar gains. Yesterday, Saudi Arabia announced it would extend its 1.3 million barrel-per-day production cut until the end of December, while Russia said it would follow suit with its 300,000 b/d cut. The news is underpinning the greenback as higher oil prices are a drag on global growth and increase inflation risks.

US Secretary of State Antony Blinken is in Kyiv (formerly Kiev) to announce another $1.0 billion in aid, although no one is sure of how much will go to the war effort and how much to secret Swiss bank accounts.

The major Asian equity indexes closed lower, except for Japan’s Nikkei 225 index, which rose 0.62% due to the weaker yen. European bourses opened in negative territory and are trading lower, with the UK FTSE 100 index and the French CAC 40 indexes down 0.63%. S&P 500 futures are down 0.19%.

The US data is just second-tier, but the ISM Services PMI (forecast 52.5 vs July 52.7) could spark a further US dollar rally if it is higher than expected.

EURUSD traded with a negative bias in a 1.0713-1.0747 range. The single currency is suffering from fears of another energy crisis after Saudi Arabia extended its voluntary production cuts to the end of the year. German factory orders fell -11.7% in August (forecast of -0.4%) compared to an increase of 7.6% in July. EURUSD is also suffering due to uncertainty around next week’s ECB meeting. The market is pricing in just a 25% chance for a rate hike due to the weak economy and lower inflation.

GBPUSD traded sideways in a 1.2544-1.2588 range as it consolidated Tuesday’s losses. Economic data underscored the weakness of the UK economy. August Construction PMI was 50.8 compared to 51.7 in July. The survey noted that “House building remained the weakest-performing part of the construction sector (40.7), with the downturn the second-fastest since May 2020.”

USDJPY traded with a bid, rising from 147.03 to 147.72 due to firm US Treasury yields. The 10-year yield closed at 4.272% yesterday and is at 4.254% in NY. Officials are not impressed. Vice Minister of Finance Masato Kanda verbally intervened, again. He said, “Looking at underlying moves, speculative action or activity that cannot be explained by fundamentals can be observed.” Then he warned that the government would take appropriate steps.

AUDUSD traded in a 0.6357-0.6404 range overnight, with prices getting a bit of a boost from better-than-expected economic growth data. Q2 GDP rose 0.4% q/q (forecast 0.3%) and 2.1% y/y (forecast 1.7%). The data was revised higher by 0.1% in the previous three quarters, which some analysts believe keeps the rate hike door ajar.

Top of Form

FX high, low, open

Source: Investing.com

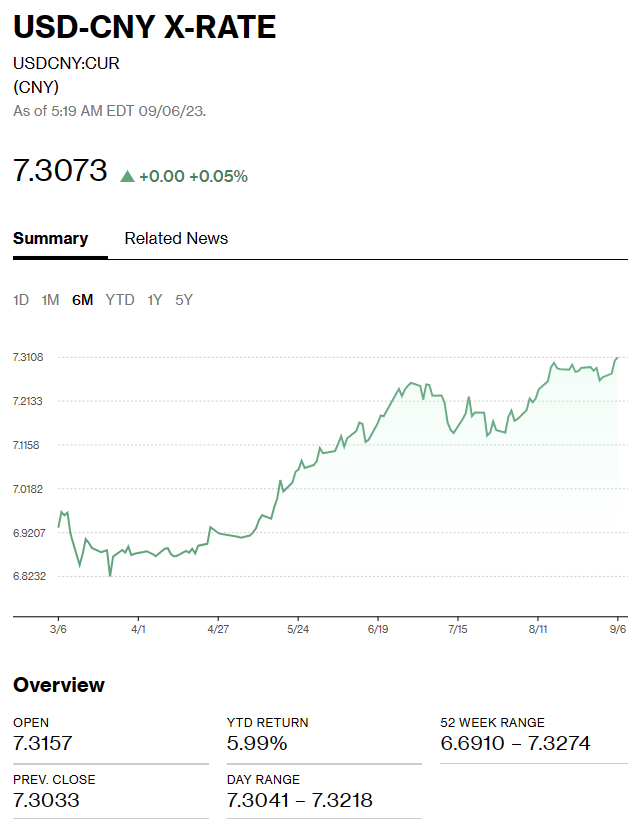

China Snapshot

Bank of China Fix: today 7.1969, expected 7.3097, previous 7.1783.

Shanghai Shenzhen CSI 300 fell 0.22% to 3812.03

There are reports that Chinese state owned banks were selling dollars in the onshore market.

Chart: USDCNY 1 month

Source: Bloomberg