May 30, 2024

- Treasury yields retreating from recent peak.

- GDP and jobless claims data as expected and a non-event.

- US dollar is drifting lower in tandem with lower Treasury yields.

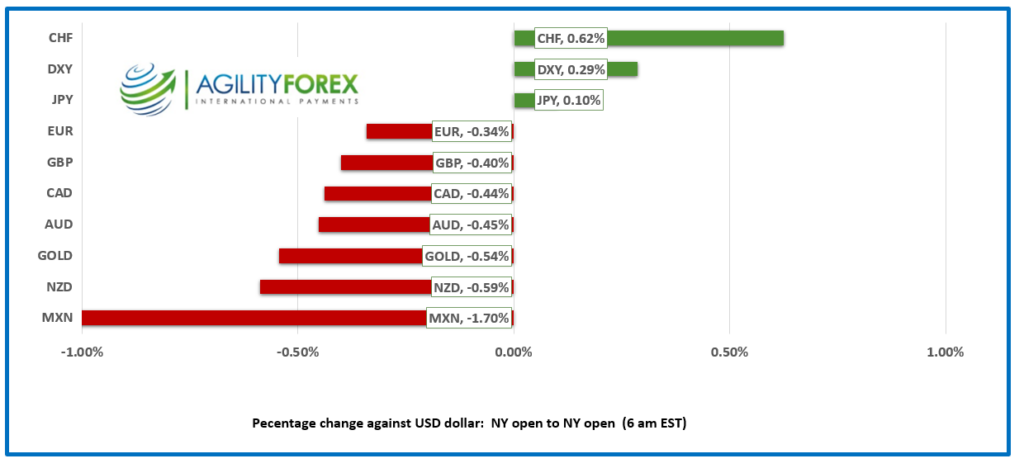

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3721, overnight range 1.3693-1.3736, close 1.3718

USDCAD rallied sharply yesterday after bond traders downgraded their expectations for earlier-than-expected Fed rate cuts and drove the US 10-year Treasury yield to 4.62%. The rally was exacerbated by earlier comments from Minneapolis Fed President pointing out that rate hikes were still a possibility.

WTI oil prices dropped on increased fears that a period of prolonged elevated US rates will suffocate global demand. WTI dropped from 80.60 yesterday to 78.59 today. News that the API reported a 6.4 million barrel decline in crude inventories was ignored.

Today, Statistics Canada reported that “Canada’s current account balance (on a seasonal adjusted basis) posted a $5.4 billion deficit in the first quarter, widening $0.9 billion from the previous quarter.”

USDCAD Technicals

The intraday USDCAD are bullish following the decisive break above 1.3690 yesterday. USDCAD is in a steep hourly uptrend channel between 1.3680 and 1.3750 which should contain price action today.

The longer term technicals are unchanged with the uptrend from January 2024 intact while prices are above 1.3570. That trendline is supported by the 100 and 200 day moving averages at 1.3571 area.

For today, USDCAD support is at 1.3680 and 1.3650. Resistance is at 1.3750 and 1.3790. Today’s range is 1.3680-1.3760

Chart: USDCAD daily

Source: DailyFX

“No sign of Intelligent Life Anywhere”

Those are Buzz Lightyear’s words, but Fed Chair Jerome Powell might be thinking the same about the bond market. That’s because the Fed boss has been telling all who would listen that US interest rates need to remain in restrictive territory until inflation is on a sustainable downward trend to 2.0%. For a while, bond traders figured that they were the masters of the universe, and rates would go lower because they wanted them to. That lasted until a series of stronger-than-expected economic reports and a chorus of Fed officials chirping about the need for unchanged or even higher rates made them rethink their view. The surge in Treasury yields, with the 10-year yield at 4.594% today, is a sign of capitulation, and a key reason why the US dollar is bid.

No Joy from Today’s Data

US Weekly jobless rose by 3,000 to 219,000 in the week ending May 24 which was close enough to the forecast (218,000) to be a non-event. The second estimate of real GDP was 1.3% y/y, as expected

EURUSD.

EURUSD is at the top of its 1.0788-1.0820 overnight range as it attempts to recoup some of yesterday’s losses. The single currency got a bit of support after Eurozone Economic Sentiment increased, albeit slightly, rising to 96 from 95.6. However, enthusiasm was tempered by the Employment Expectations indicator continuing to decline. The EURUSD uptrend from the end of April is intact while prices are above 1.0770.

GBPUSD

GBPUSD broke its May uptrend line yesterday and fell from 1.2778 to close at 1.2701. The losses were fueled by fears that US rates will remain unchanged for longer than expected even though the BoE may delay easing due to sticky inflation. The UK election campaign is in full swing, but UBS analysts suggest that a Labour party win is fully priced into the currency. The GBPUSD uptrend from April is intact above 1.2630.

USDJPY

USDJPY retreated from its 157.71 peak yesterday and dropped to 156.54 overnight despite the US 10-year Treasury yield climbing from 4.41% last Friday to 4.624%. Gains may have been capped because the 157.70 area is where the BoJ supposedly intervened at the beginning of May. USDJPY downside is limited while Treasury yields remain at current levels.

AUD/USD and NZD/USD

AUDUSD dropped from 0.6660 to close in NY at 0.6610 yesterday, then traded in a 0.6591-0.6621 band overnight. The increase in negative risk sentiment from higher US interest rates is weighing on the currency while expectations that the RBA will leave rates unchanged until November are providing some support.

NZDUSD dropped from 0.6146 yesterday to 0.6089 overnight and is sitting on support at 0.6100. The spike in US Treasury yields drove NZDUSD lower. The government delivered its first budget and introduced a tax cut package, as expected. Analysts suggest that implementing tax cuts before spending cuts will make the RBNZ’s job of lowering inflation much more difficult. They now expect the first rate cut will occur much later in 2025.

USD/MXN

USD/MXN rallied from 16.9665 to 17.1395 overnight and is near the top of that band in early NY trading, boosted by higher US Treasury yields. The prospect that the Fed leaves rates unchanged for the rest of the year while Banxico cuts rates by 25 bps on June 27 has put a floor under USDMXN.

BTC/USD

BTC/USD (Bitcoin) traded quietly in a 67,180-68,467 band as the mantra of Fed rates being “higher for longer” limits gains

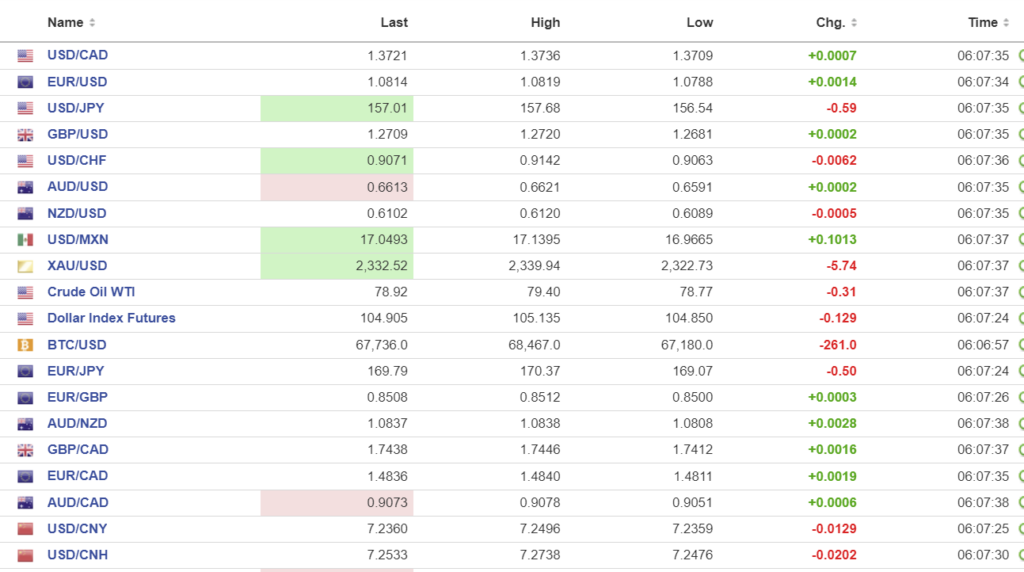

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

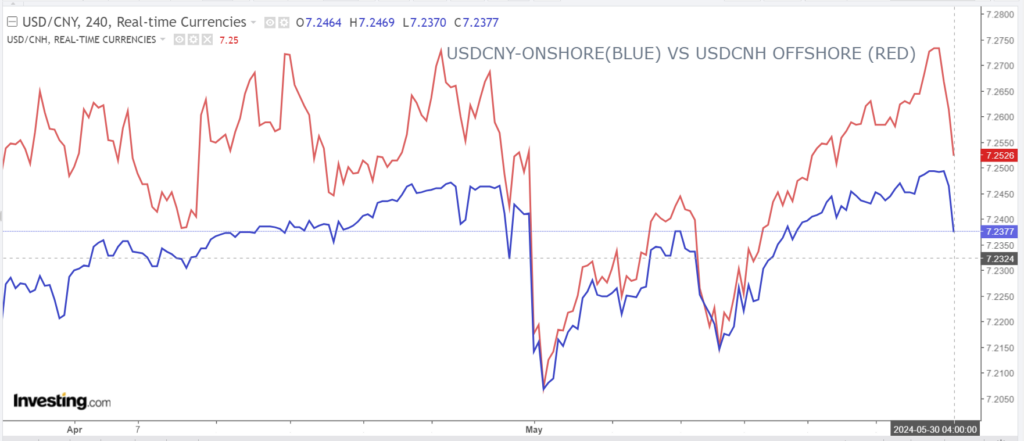

China Snapshot

PBoC fix: 7.1111 vs expected 7.2623 (prev. 7.1106)

Shanghai Shenzhen CSI 300 fell 053% to 3594.31.

Chart: USDCNY and USDCNH

Source: Investing.com